Loan refinancing can quietly reshape your finances—for better or worse. Many Americans refinance to lower monthly payments, reduce interest costs, or change loan terms. Others refinance at the wrong time and end up paying more over the life of the loan.

Refinancing isn’t just a quick rate swap. It’s a brand-new loan with new rules, new costs, and long-term effects on your cash flow and credit. Understanding how it works—and when it actually makes sense—is what separates smart refinancing from expensive mistakes.

Key Takeaways

In the U.S. financial system, refinancing is widely used—but often misunderstood. Before diving into the details, here are the key points every borrower should understand upfront.

- Loan refinancing replaces an existing loan with a new one, usually with a different interest rate, term, or lender.

- The main goals are lower interest, lower monthly payments, or better loan terms—not all refinances achieve all three.

- Upfront costs and timing determine whether refinancing actually saves money.

- Refinancing can help or hurt your credit depending on timing, application strategy, and repayment behavior.

- The best time to refinance depends on rates, your credit profile, loan balance, and how long you’ll keep the loan.

What Is Loan Refinancing?

Loan refinancing means taking out a new loan to pay off an existing one. After refinancing, you no longer owe the old loan—you now owe the new lender under new terms.

Those new terms may change:

- Interest rate (lower or higher)

- Monthly payment

- Loan length (term)

- Type of interest (fixed vs. variable)

- Lender

Refinancing does not erase debt. It restructures it.

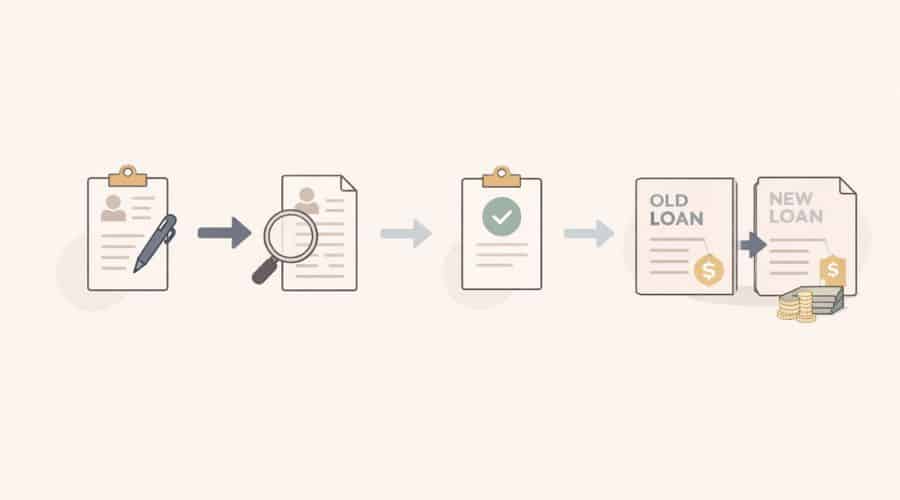

How Loan Refinancing Works in the United States

At a high level, refinancing follows a consistent process across most loan types in the U.S.:

1. You Apply for a New Loan

You submit a refinance application to a bank, credit union, or online lender. The lender reviews:

- Credit score and credit history

- Income and employment

- Debt-to-income (DTI) ratio

- Current loan details

- Collateral value (for secured loans like mortgages or auto loans)

2. The Lender Prices the New Loan

Based on risk, the lender offers:

- An interest rate

- A loan term

- Fees and closing costs

Rates and terms are influenced by broader market conditions and your personal credit profile, not just your existing loan. Federal interest rate policy and lender risk models also play a role in how refinance offers are priced.

3. Approval and Payoff of the Old Loan

If you accept the offer:

- The new lender pays off your old loan directly

- Your old account is closed (or marked paid in full)

- You begin making payments on the new loan

4. You Repay the New Loan Under New Terms

From this point forward:

- Your payment schedule resets

- Interest accrues based on the new rate and term

- Your payoff timeline may be shorter or longer than before

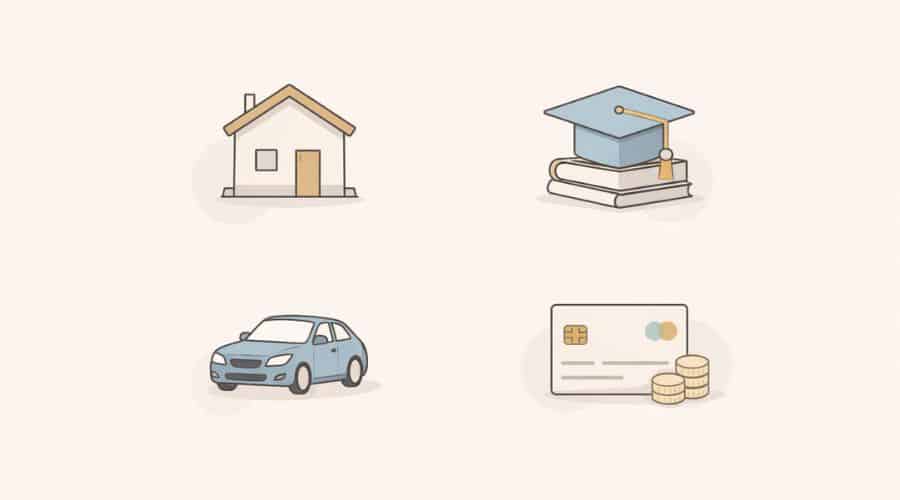

Common Types of Loans That Can Be Refinanced

Refinancing rules, risks, and borrower protections vary significantly by loan type. Understanding these differences is essential before deciding to refinance.

Mortgage Loans

Homeowners refinance mortgages to:

- Lower interest rates

- Switch from adjustable-rate to fixed-rate

- Shorten or extend the loan term

- Access home equity (cash-out refinance)

Mortgage refinancing is heavily regulated and involves closing costs, disclosures, and consumer protections enforced by agencies like the Consumer Financial Protection Bureau.

Student Loans

Both federal and private student loans can be refinanced, but the consequences differ:

- Federal loan refinancing converts them into private loans, permanently giving up federal protections.

- Private loan refinancing focuses on rate and term changes.

Federal student loan programs are overseen by the U.S. Department of Education, while tax treatment of interest is governed by the Internal Revenue Service.

Auto Loans

Auto refinancing is common when:

- Credit has improved since purchase

- Interest rates have dropped

- Monthly payments are too high

The car remains collateral, and loan terms often depend on vehicle age and mileage.

Personal Loans

Unsecured personal loans can be refinanced to:

- Reduce interest rates

- Consolidate multiple debts

- Adjust monthly payments

Because there’s no collateral, rates depend heavily on creditworthiness.

What Refinancing Can Change—and What It Can’t

Refinancing can change:

- Interest rate

- Monthly payment

- Loan length

- Total interest paid

- Lender relationship

Refinancing cannot:

- Eliminate debt without repayment

- Fix chronic overspending

- Guarantee savings without costs

- Reverse past late payments or defaults

Understanding these limits helps prevent costly assumptions.

When Refinancing Starts to Make Sense

Refinancing deserves a closer look when:

- Interest rates are meaningfully lower than your current rate

- Your credit profile has improved

- Your income is more stable

- You plan to keep the loan long enough to recoup fees

These conditions don’t guarantee a good refinance—but without them, refinancing often increases long-term costs instead of reducing them.

When Loan Refinancing Makes Financial Sense

Refinancing works best when it solves a specific financial problem—not just because a lender advertises a lower rate. The decision should be driven by math, timing, and your personal financial situation. Below are the most common situations where refinancing tends to make sense for U.S. borrowers, assuming fees and risks are carefully evaluated.

1. Interest Rates Are Significantly Lower Than Your Current Rate

A meaningful rate drop can reduce interest costs over time. As a general rule, a small reduction may not justify fees, while a larger drop often does—especially on long-term loans.

Important: Market rates alone don’t matter. What counts is the rate you personally qualify for based on credit, income, and risk profile.

On shorter-term loans like auto or personal loans, savings periods are smaller, so comparing fees becomes even more important.

2. Your Credit Profile Has Improved

Refinancing often makes sense if, since you took the original loan:

- Your credit score increased

- You reduced high-interest debt

- You established a longer, cleaner payment history

Lenders price loans based on current risk, not your past situation.

3. You Need to Change Your Monthly Payment—Strategically

Refinancing can:

- Lower payments by extending the loan term

- Raise payments by shortening the term (often to reduce total interest)

The key is intention. Lower payments help short-term cash flow, while higher payments reduce total interest. Problems arise when loan terms are extended without a clear plan.

Both approaches can be reasonable depending on cash flow, job stability, and long-term goals.

4. You Want More Predictable Payments

Switching from a variable-rate loan to a fixed-rate loan can protect against rising interest rates. This is common with:

- Adjustable-rate mortgages

- Variable-rate private student loans

Stability can be as valuable as savings.

5. You Plan to Keep the Loan Long Enough to Break Even

Refinancing costs money. You benefit only if you keep the loan long enough for monthly savings to outweigh upfront costs.

This is especially important for borrowers who expect job changes, relocation, or major life expenses in the near future.

When Refinancing Often Does Not Make Sense

Refinancing is frequently a bad idea when:

- Fees outweigh interest savings

- You’ll sell the asset or repay the loan soon

- Your credit has worsened

- You’re refinancing repeatedly without clear benefit

- You’re using refinancing to mask affordability problems

Key warning: Refinancing to lower payments while repeatedly extending the loan term often increases total interest paid, even when monthly bills feel easier.

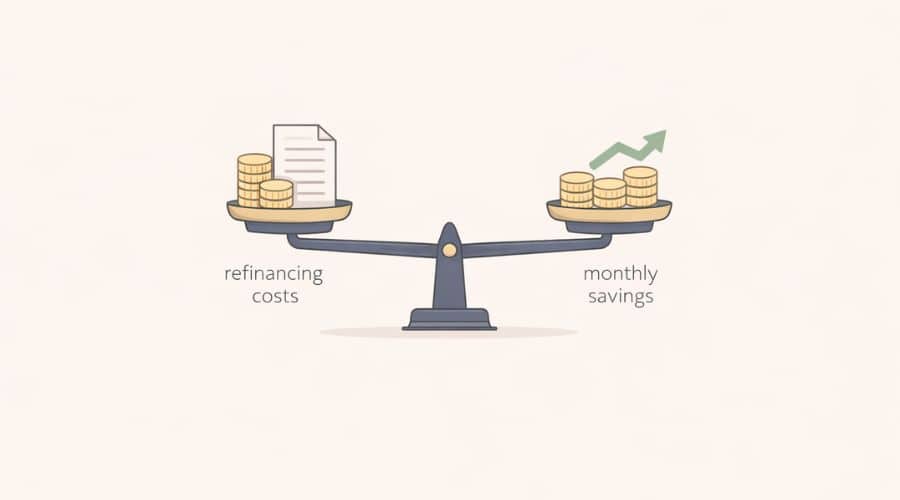

Understanding the Break-Even Point (Critical Concept)

The break-even point is when your cumulative savings equal your refinance costs.

Simple example (auto loan):

- Refinance costs: $900

- Monthly savings: $50

- Break-even time: 18 months

If you’ll keep the loan longer than 18 months, refinancing may save money.

If not, it likely won’t.

Always calculate this before refinancing.

Pros and Cons of Loan Refinancing

| Pros | Cons |

|---|---|

| Lower interest rate | Upfront fees and closing costs |

| Reduced monthly payment | Loan term may reset |

| Potential long-term savings | More interest if term is extended |

| Improved cash flow | Temporary credit score dip from hard inquiry |

| Fixed-rate stability | Loss of certain protections (loan-dependent) |

Real-Life U.S.-Based Examples

Example 1: Auto Loan Refinance

A borrower buys a car with limited credit history. Two years later, their credit improves.

- Original rate: 9.5%

- New rate: 5.2%

- Monthly payment drops

- Loan term stays similar

Result: Legitimate savings with minimal downside.

Example 2: Mortgage Refinance With a Catch

A homeowner refinances to lower monthly payments but restarts a 30-year term after 7 years of payments.

Result: Monthly relief, but significantly more interest paid over time.

Example 3: Student Loan Refinance Trade-Off

A borrower refinances federal student loans into a private loan to get a lower rate.

Result: Lower interest, but permanent loss of federal income-driven repayment and hardship protections.

How Refinancing Affects Your Credit Score

Refinancing can have short-term and long-term effects:

Short-term:

- Hard credit inquiry (temporary dip)

- New account lowers average account age

Long-term (if managed well):

- On-time payments help payment history

- Lower balances may improve utilization

Important: Multiple refinance applications within a short time may be grouped as a single inquiry for certain loan types, but rules vary by credit bureau and loan category.

Common Refinancing Mistakes to Avoid

- Focusing only on the interest rate

- Ignoring total loan cost

- Resetting terms without realizing it

- Refinancing too frequently

- Not comparing loan estimates carefully

Biggest mistake: Confusing lower monthly payments with lower total cost.

Myths vs. Facts About Loan Refinancing

Myth: Refinancing always saves money

Fact: It only saves money if costs and timing align

Myth: You need perfect credit

Fact: Improvement—not perfection—is what matters

Myth: Refinancing fixes financial problems

Fact: It’s a tool, not a solution

Step-by-Step: How to Refinance a Loan Responsibly

This is a practical, borrower-focused process that applies to most U.S. loan types. The goal is to confirm real savings and avoid costly refinancing mistakes before you commit.

Step 1: Clarify Your Primary Goal

Be specific. Are you trying to:

- Lower total interest paid?

- Reduce monthly payments?

- Change loan length?

- Move from variable to fixed?

If you can’t name the goal, refinancing is premature. Refinancing without a clear objective often leads to higher long-term costs, even when monthly payments look lower.

Step 2: Gather Your Current Loan Details

You’ll need:

- Current interest rate and APR

- Remaining balance

- Remaining term

- Monthly payment

- Any prepayment penalties (some loans still have them)

Without this baseline, you can’t measure improvement.

Step 3: Check Your Credit and Financial Profile

Review:

- Credit reports for errors

- Current credit score range

- Debt-to-income ratio

- Income stability

Important: Apply only when your profile is at its strongest. Small improvements can materially change offers. Even small credit score increases can result in noticeably better rates and lower fees.

Step 4: Request Multiple Loan Estimates

Compare Loan Estimates or equivalent disclosures—not ads or teaser rates. Focus on:

- APR (not just the rate)

- Total closing costs or fees

- Term length

- Whether the rate is fixed or variable

Never compare offers with different terms without adjusting for total cost.

Step 5: Calculate the Break-Even Point

Use your actual numbers to determine how long it takes to recover fees. If the break-even period exceeds how long you expect to keep the loan, refinancing is usually a bad choice. This is especially important if you plan to move, sell the asset, or refinance again within a short period.

Step 6: Review the Final Disclosure Carefully

Before closing:

- Confirm fees didn’t increase

- Verify the interest rate and term

- Check for add-ons you didn’t request

Walk away if something doesn’t match what you were quoted. You are never obligated to proceed if the final terms differ from the original offer.

Legal, Tax, and Regulatory Considerations (U.S. Only)

Consumer Protections

Certain loans—especially mortgages—come with federal disclosure requirements, timing rules, and rescission rights. These rules are designed to prevent last-minute surprises but do not guarantee a good deal. Borrowers are still responsible for evaluating costs, terms, and long-term impact.

Tax Treatment

- Mortgage interest may be deductible if you itemize, subject to IRS rules and limits.

- Student loan interest may be deductible within income thresholds.

- Personal and auto loan interest is generally not deductible.

Refinancing can change deductibility depending on loan structure and use of funds.

Loss of Existing Protections

Refinancing can permanently remove:

- Federal student loan repayment options

- Deferment or forbearance rights

- Certain borrower assistance programs

Key warning: Once these protections are gone, they cannot be restored. This is most critical when refinancing federal student loans into private loans.

Who Refinancing Is Best For—and Who Should Be Cautious

Refinancing outcomes vary widely depending on income stability, credit strength, and long-term plans.

Refinancing Often Works Well For:

- Borrowers with improved credit

- Stable income households

- Long-term loan holders

- People consolidating high-interest debt with discipline

Extra Caution Is Needed If You:

- Expect job or income changes

- Plan to sell or repay soon

- Are using refinancing to cover budget gaps

- Rely on federal loan protections

Refinancing should support financial stability—not substitute for it.

How Refinancing Affects Long-Term Finances

The long-term impact of refinancing depends entirely on how the new loan compares to the old one over time.

Done well, refinancing can:

- Reduce lifetime interest

- Improve cash flow

- Increase financial predictability

Done poorly, it can:

- Increase total debt cost

- Delay payoff timelines

- Encourage repeated borrowing cycles

The math—not the marketing—decides the outcome.

Refinancing vs. Other Debt Strategies (Important Comparisons)

Refinancing is not the only way to change how debt affects your finances. In some cases, another approach is more appropriate. Choosing the right strategy depends on your financial condition, loan terms, and long-term goals.

Refinancing vs. Loan Modification

- Refinancing replaces your loan with a new one.

- Loan modification changes terms on your existing loan, usually due to hardship.

Loan modifications are typically limited, lender-specific, and not available unless you’re already struggling.

Refinancing vs. Debt Consolidation

- Refinancing usually involves one existing loan.

- Debt consolidation often combines multiple debts into one new loan.

Consolidation can simplify payments but does not reduce debt by itself and may raise total costs if terms are extended. This is especially true when high-interest debts are moved into longer-term loans.

Refinancing vs. Paying Extra Principal

If your current loan has:

- A competitive interest rate

- No prepayment penalty

Making extra principal payments may reduce total interest without fees, making refinancing unnecessary. In these cases, staying with your existing loan can be the most cost-effective option.

Common Beginner Misunderstandings

- “Lower payment means better deal.”

Not always. Total interest matters more than monthly relief. - “Rates dropped, so I should refinance.”

Only if your offered rate and fees produce net savings. - “I can always refinance again later.”

Each refinance resets terms and adds cost. - “Refinancing fixes bad debt decisions.”

It can reduce damage—but it doesn’t erase it.

Frequently Asked Questions (FAQs)

Below are clear, practical answers to the most common refinancing questions from U.S. borrowers.

-

Does refinancing reset my loan term?

Yes. Most refinances start a new loan clock, even if the term length looks similar. This can increase total interest if you extend repayment.

-

How often can you refinance a loan?

There is no universal legal limit, but frequent refinancing often reduces benefits due to repeated fees and term resets.

-

Is refinancing bad for your credit score?

It can cause a small, temporary dip, but responsible repayment can improve credit over time.

-

Can you refinance with bad credit?

It’s possible, but offers are often worse than existing terms. Refinancing with poor credit frequently increases total cost.

-

Should I refinance if I’m planning to move or sell?

Usually no. Short holding periods rarely allow enough time to recover refinance costs.

-

Is refinancing federal student loans risky?

Yes. Refinancing federal loans into private loans permanently removes federal protections, even if rates are lower.

-

Are refinance fees negotiable?

Sometimes. Fees vary by lender and loan type. Comparing offers is the best leverage.

-

Does refinancing change my tax situation?

It can. Deductibility of interest depends on loan type, use of funds, and IRS rules.

Final Thoughts: When Refinancing Is a Smart Financial Tool

Refinancing works best when it’s intentional, math-driven, and timed correctly. It’s not about chasing the lowest advertised rate—it’s about aligning loan structure with your real financial life.

If refinancing doesn’t clearly improve your long-term position, walking away is not a missed opportunity—it’s good financial judgment.

Disclaimer

This content is for educational and informational purposes only and is not legal, tax, or financial advice. Loan rules, tax treatment, and financial outcomes vary by individual circumstances, lender policies, and state regulations. Readers should consult a qualified financial, tax, or legal professional before making personal financial decisions.