A single missed payment can drop your credit score by dozens of points — and the damage doesn’t disappear overnight. Late payments can stay on your credit report for years, affecting your ability to qualify for loans, credit cards, and even housing.

If you’ve ever missed a payment (or are worried you might), one of the most important questions is: how long does that mistake actually stay on your record?

In this guide, you’ll learn exactly how long late payments remain on your credit report, how they impact your credit score over time, and what you can do to recover faster and protect your financial future.

Key Takeaways

- Most late payments stay on your credit report for 7 years from the original delinquency date.

- Even one 30-day late payment can hurt your credit score.

- The impact fades over time, but recent late payments matter much more than old ones.

- Paying the account current does not remove the late mark, but it prevents further damage.

- Late payments affect future loan approvals, interest rates, and sometimes insurance premiums.

Why Late Payments Matter in Real Life

Missing a payment by a few days may not feel serious, especially when life gets busy. But once a payment is reported late to the credit bureaus, it can remain on your credit report for years and affect everyday financial decisions — from qualifying for a credit card to getting a reasonable car loan rate or even passing a rental application.

Many Americans are surprised to learn that even after they catch up and pay what they owe, the record of being late does not disappear right away. That gap between what feels “fixed” and what remains on your credit report causes a lot of confusion and frustration.

Understanding how long late payments stay on your credit report — and how they affect you over time — helps you make better decisions and avoid long-term damage from short-term problems.

What Counts as a Late Payment on a Credit Report?

A payment is not considered “late” for credit reporting purposes until it passes certain time thresholds set by lenders and credit bureaus.

Most lenders report late payments in these categories:

| Days Late | How It Appears on Credit Report |

|---|---|

| 1–29 days late | Usually not reported to credit bureaus (but fees may apply) |

| 30 days late | Reported as 30-day late |

| 60 days late | Reported as 60-day late |

| 90 days late | Reported as 90-day late |

| 120+ days late | May lead to charge-off or collections |

Important: A lender may charge a late fee after the due date or after a short grace period, but credit bureaus typically only receive reports once you are 30 days past due.

So if you pay within a few days after the due date, you may pay a fee but usually avoid credit damage. This is why setting reminders or automatic payments can help protect your credit, even if you occasionally pay a little late.

How Long Do Late Payments Stay on Your Credit Report?

Under the Fair Credit Reporting Act (FCRA), most negative information — including late payments — can remain on your credit report for:

Up to 7 years from the original delinquency date.

What Is the “Original Delinquency Date”?

This is the first date the account became late and was never brought fully current again before escalating.

For example:

- Payment due: March 1, 2024

- First missed payment: March 2024

- Account later becomes 60 or 90 days late

- Even if the lender reports later updates, the 7-year clock still starts from March 2024

Each late payment entry has its own timeline, but the clock does not reset just because the account continues to be late. This rule prevents lenders from keeping negative information on your report longer than the law allows.

Does Paying the Balance Remove the Late Payment?

No.

Paying the account current is very important, but it does not erase the late payment history.

What paying does:

- Stops additional late marks

- Prevents collections or charge-offs

- Helps your score begin recovering over time

What paying does NOT do:

- Remove existing late payment records

- Reset the 7-year reporting period

The late mark stays until it naturally falls off your credit report unless it is incorrect or reported in error.

Do All Late Payments Hurt Your Score the Same Way?

No. The impact depends on several factors.

How Late the Payment Was

A 90-day late payment is more damaging than a 30-day late payment. Credit scoring models treat deeper delinquencies as more serious risk signals.

How Recent the Late Payment Is

Recent late payments hurt much more than old ones.

- Last month’s late payment → strong negative impact

- Five-year-old late payment → much smaller impact

Even though the mark remains visible, its influence fades over time if you maintain good payment behavior afterward.

Your Overall Credit Profile

Late payments cause larger drops if:

- You previously had excellent credit

- You have few other accounts

- You have limited credit history

People who already have damaged credit may see smaller immediate drops, but repeated late payments can push them into much worse score ranges.

Which Accounts Can Report Late Payments?

Any lender that reports to the credit bureaus can report late payments, including:

- Credit cards

- Auto loans

- Mortgages

- Student loans

- Personal loans

- Retail store cards

Some utility and phone companies may not report regular payments, but they often report collections if bills go unpaid long enough. Medical bills, in particular, often appear only after they are sent to collections rather than as regular late payments.

Why Credit Scores Care So Much About Late Payments

Payment history is the largest factor in most U.S. credit scoring models.

Approximate influence in major models:

| Factor | Share of Score |

|---|---|

| Payment history | ~35% |

| Credit utilization | ~30% |

| Length of credit history | ~15% |

| New credit | ~10% |

| Credit mix | ~10% |

This is why even a single missed payment can cause noticeable score changes, especially if your history was previously clean.

Common Misunderstandings About Late Payments

Myth: Paying off the account deletes the late payment.

Fact: Payment stops further damage, but the history stays until it ages off.

Myth: Lenders must remove late payments after a few years.

Fact: They can legally report accurate late payments for the full 7-year period.

Myth: All late payments are equally harmful.

Fact: Severity and recency matter a lot.

Myth: Closing the account removes the late history.

Fact: Closing does not erase reported payment behavior.

How Late Payments Affect Your Credit Score Over Time

The damage from a late payment is not permanent, but it usually follows a predictable pattern. Most people see the biggest credit score drop shortly after the missed payment, followed by gradual recovery if no new problems appear. Understanding this timeline helps set realistic expectations and prevents unnecessary panic.

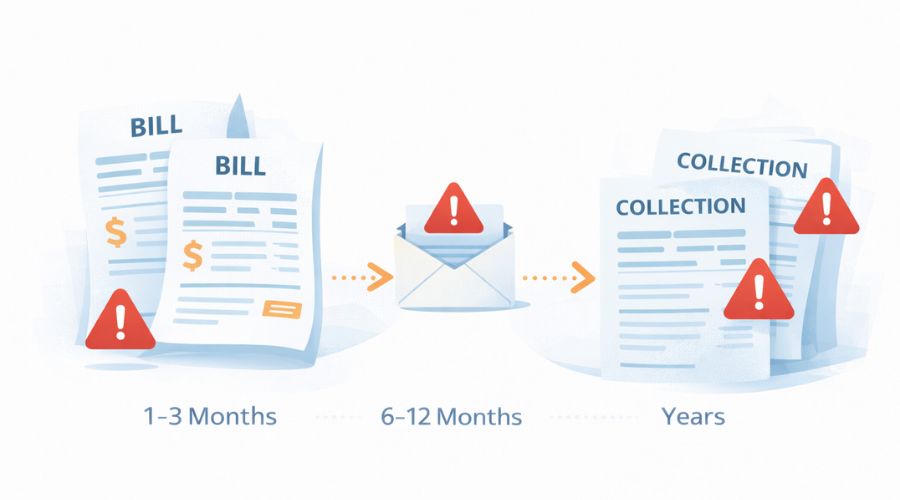

Immediate Impact (First 1–3 Months)

When a late payment is first reported:

- Credit scores may drop significantly, especially if your prior history was clean

- The drop is usually larger for 60- or 90-day late payments

- Lenders view this as a recent risk signal

At this stage, the late payment is both visible and heavily weighted in scoring models. This is why most of the score damage happens early, even though the late mark remains on your report for years.

Medium-Term Impact (6 Months to 2 Years)

If you make all payments on time after the mistake:

- The negative effect gradually weakens

- Positive payment history begins to offset the damage

- Score recovery becomes noticeable, though not complete

You may still qualify for credit, but often at higher interest rates during this phase.

Long-Term Impact (3 to 7 Years)

As the late payment gets older:

- It carries much less weight in scoring formulas

- Many lenders focus more on recent behavior than old mistakes

- Your score may return close to previous levels if no new issues occur

Even though the late mark still appears on the report, its practical impact becomes small toward the end of the 7-year period.

Can Late Payments Be Removed Before 7 Years?

Only under specific conditions.

When Removal Is Possible

Late payments may be removed early if:

- The information is inaccurate

- The payment was never actually late

- The lender reported the wrong dates or amounts

- The account does not belong to you (identity errors)

In these cases, you have the legal right to dispute the entry with:

If the lender cannot verify the information, the bureau must remove or correct it. This is why it helps to include clear documents when you file a dispute, such as payment confirmations or bank statements.

Goodwill Adjustments (Not Guaranteed)

Some lenders may remove a late mark as a one-time courtesy if:

- You have a long history of on-time payments

- The late payment was caused by an unusual situation

- The account is now fully current

This is called a goodwill adjustment. Lenders are not required to approve these requests, and many deny them, but some consumers do succeed with polite, well-documented requests.

When Removal Is Not Allowed

If the late payment is:

- Accurate

- Verified by the lender

- Properly reported

Then it must legally remain until the reporting period ends.

Credit bureaus are not allowed to delete correct negative information simply because it hurts your score.

What Happens If Late Payments Lead to Collections or Charge-Offs?

Late payments can escalate if they continue.

Typical Progression

- 30–90 days late → Delinquency marks

- 120–180 days late → Charge-off by lender

- Account may be sold to collections agency

- Separate collection account may appear. This means one missed account can result in multiple negative entries on your credit report.

Each of these events:

- Creates additional negative marks

- Has its own 7-year reporting timeline

- Causes deeper score damage

Important:

Paying a collection does not erase the original late payment history or the collection record, though it can prevent lawsuits and further harm.

How Late Payments Affect Loan and Credit Approvals

Late payments influence both:

- Whether you are approved

- How much you pay in interest

Some lenders may also require larger down payments or additional documentation.

Mortgage and Auto Loans

Lenders often review:

- How recent the late payment was

- How severe it was (30 vs. 90 days)

- Whether it involved housing or installment debt

Recent mortgage late payments are treated especially seriously for future home loans.

Credit Cards and Personal Loans

Card issuers may:

- Deny applications

- Offer lower limits

- Assign higher interest rates

Even if approved, borrowers with recent late payments often receive less favorable terms.

Insurance and Rentals (In Some States)

In many states:

- Insurers may use credit-based insurance scores

- Landlords may review credit reports for payment behavior

This means late payments can affect more than just borrowing.

Who Is Most at Risk From Long-Term Damage?

Late payments hurt everyone, but the impact is greater when:

- You have short credit history

- You have few active accounts

- You already have other negative marks

For someone building credit, even one missed payment can slow progress for years. This is why early-stage credit building requires extra attention to due dates and account management.

Steps to Reduce the Damage After a Late Payment

Once a late payment is reported, removal is difficult, but you can limit future harm.

Step 1: Bring the Account Current Immediately

The sooner you pay:

- The fewer late categories appear

- The less likely the account escalates to collections

Step 2: Set Automatic Payments

Even minimum payments help prevent future late marks.

Autopay reduces the risk of:

- Forgetting due dates

- Being late due to busy schedules

Step 3: Keep All Other Accounts Perfect

After a mistake, future on-time payments are the most powerful repair tool available.

Step 4: Monitor Your Credit Reports

Check reports from all three bureaus regularly to ensure:

- No duplicate entries

- No incorrect late dates

- No accounts you do not recognize

Step 5: Keep Credit Balances Low

High balances combined with late payments can slow recovery even more. Keeping credit card balances low helps your score rebound faster once payment history improves.

Real-Life Examples: How Late Payments Play Out

Seeing how late payments affect real situations helps explain why timing and patterns often matter more than a single credit score number.

Example 1: One Missed Credit Card Payment

Situation:

A borrower with a long, clean credit history forgets one credit card payment and pays it 35 days late.

Result:

- A 30-day late payment appears on the credit report

- Credit score drops noticeably at first

- After 6–12 months of perfect payments, most of the damage fades. Many card issuers may still approve new credit, but often with slightly higher interest rates at first.

- The late mark stays visible for years, but lenders care less over time

Key point: A single, isolated mistake usually causes short-term pain but not long-term financial lockout.

Example 2: Multiple Late Payments on Auto Loan

Situation:

A borrower misses three car payments over six months, reaching 90 days late before catching up.

Result:

- Several delinquency marks appear

- Much larger credit score drop

- Higher risk classification for future lenders. Higher risk classification for future lenders

- Auto refinancing becomes harder and more expensive

Key point:

Repeated late payments signal ongoing trouble, which lenders treat more seriously than one-time errors.

Example 3: Medical Bill Turns Into Collection

Situation:

A medical bill is forgotten and later sent to collections.

Result:

- Original late payment may not appear

- Collection account damages credit

- Separate negative entry remains for up to 7 years

- Even after paying, the collection can remain reported. However, paying can still prevent further collection actions and may improve lender perception in manual reviews.

Key point: Not all late payments show up the same way, but unpaid bills can still harm credit through collections.

Who Should Be Extra Careful About Late Payments?

Some people face higher consequences from late payments based on where they are in their financial journey.

Late payments are risky for everyone, but some groups face higher consequences.

People Planning Major Purchases

If you plan to apply for:

- A mortgage

- An auto loan

- A personal loan for large expenses

Even one recent late payment can affect approval and interest rates.

People With Thin Credit Files

If you have:

- Only one or two accounts

- A short credit history

Each payment carries more weight, so a single mistake can have a bigger scoring effect.

People Rebuilding Credit

When prior negatives already exist:

- New late payments slow recovery

- Lenders see a pattern instead of progress

Consistent on-time payments are critical during rebuilding periods.

When Late Payments Matter Less

While late payments are always negative, their practical impact may be smaller when:

- They are many years old

- Your recent history is strong

- Your income and overall finances are stable

Some lenders use manual underwriting or consider:

- Employment stability

- Debt-to-income ratio

- Cash reserves

In these cases, old late payments may not be deal-breakers, though they still influence pricing. However, recent late payments almost always carry more weight than income or savings alone.

Late Payments vs. Other Negative Credit Events

Not all credit problems carry the same weight.

| Event | Typical Severity |

|---|---|

| 30-day late payment | Moderate |

| 90-day late payment | High |

| Collection account | High |

| Charge-off | Very high |

| Bankruptcy | Severe |

Late payments are serious, but they are generally less damaging than charge-offs or bankruptcies, especially if they are isolated.

Myths vs. Facts About Credit Repair After Late Payments

Myth: Credit repair companies can erase real late payments.

Fact: Accurate negative information cannot be legally removed early.

Myth: Closing the account helps your score.

Fact: Closing does not remove payment history and may reduce available credit.

Myth: Paying more than the minimum reverses the damage.

Fact: Payment history records whether you paid on time, not how much extra you paid.

Myth: Waiting it out is the only option.

Fact: While time is required, strong ongoing payment behavior speeds recovery.

Myth: Disputing always removes late payments.

Fact: Disputes only work when information is incorrect or cannot be verified.

How Late Payments Affect Long-Term Financial Health

Late payments do more than lower a credit score number.

They can lead to:

- Higher borrowing costs over many years

- Fewer lender options

- Difficulty building emergency savings if credit costs rise

Small mistakes can quietly increase long-term expenses through higher interest rates, over time, this can add up to thousands of dollars in extra costs on loans and credit cards. even when no one explicitly mentions credit history.

Legal Rules That Control How Late Payments Are Reported

Late payments are not reported randomly. In the United States, federal law sets strict rules on what credit bureaus and lenders can report, how long negative information can remain, and when it must be removed.

Fair Credit Reporting Act (FCRA)

Under the Fair Credit Reporting Act, credit bureaus must:

- Report information that is accurate and verifiable

- Remove most negative information after 7 years

- Correct or delete information that cannot be verified

For late payments, the reporting period starts from the original delinquency date, not from when the account was last updated. This prevents lenders from extending the reporting period by repeatedly updating the same delinquency.

What Lenders Are Required to Report

Lenders are not required to report to credit bureaus, but if they do, they must:

- Report accurate payment status

- Update corrections when errors are found

- Not re-age accounts to extend reporting time

Re-aging — changing delinquency dates to keep negative marks longer — is illegal. If this happens, you can dispute the entry and report the issue to the credit bureau.

How to Dispute Incorrect Late Payments (Step-by-Step)

If you believe a late payment is wrong, you have the right to challenge it.

Step 1: Check All Three Credit Reports

Different lenders report to different bureaus.

You may see an error on one report but not the others.

Look for:

- Wrong payment dates

- Payments marked late that were on time

- Accounts that are not yours

Step 2: Gather Proof

Helpful documents include:

- Bank statements

- Payment confirmations

- Billing statements

- Letters from lenders screenshots of online payment confirmations (if available)

You do not need a lawyer or notarized documents for routine disputes.

Step 3: Submit Disputes to Each Bureau

You can dispute with:

- Experian

- Equifax

- TransUnion

Disputes can be submitted:

- Online

- By mail (slower but creates paper trail)

Phone disputes are possible, but they provide less documentation and are not recommended for complex cases.

Be specific about:

- Which account is wrong

- Which month is incorrect

- What correction you are requesting

Step 4: Investigation Timeline

By law, credit bureaus generally have:

- 30 days to investigate

- They contact the lender to verify the data

During this time, the account may be temporarily marked as “under dispute” on your credit report.

If the lender cannot verify:

- The entry must be corrected or removed

If it is verified:

- The late payment remains

Step 5: Check the Results

After the investigation, you will receive:

- Written results

- Updated credit report if changes were made

If errors remain, you can:

- Add a short consumer statement to the report

- Dispute again with new evidence

Can Credit Bureaus Remove Late Payments Automatically?

Yes — when the legal reporting period expires.

Once the 7-year limit passes:

- The bureau must remove the late payment entry

- You do not need to request deletion

However, outdated entries sometimes remain due to reporting errors, which is why checking your reports matters.

How Long Before Scores Recover After a Late Payment?

There is no fixed timeline, but patterns are consistent.

| Time After Late Payment | Typical Effect |

|---|---|

| 1–3 months | Largest score impact |

| 6–12 months | Partial recovery |

| 12–24 months | Much of the impact fades |

| 3+ years | Minimal scoring influence |

Actual recovery varies based on your overall credit profile and future payment behavior.

Recovery is faster when:

- All other accounts stay current

- Credit balances remain low

- No new negative items appear

Frequently Asked Questions (FAQ) About How Long Do Late Payments Stay on Credit Report

-

How long does a 30-day late payment stay on your credit report?

A 30-day late payment can stay for up to 7 years from the original delinquency date, even if the account is later paid in full and closed.

-

Will paying off my debt remove late payments?

No. Paying prevents further damage and helps your score recover over time, but it does not delete past late payments if they were accurately reported.

-

Do student loan late payments follow the same 7-year rule?

Yes. Federal and private student loan delinquencies are generally subject to the same FCRA 7-year reporting limit for late payments and defaults.

-

Can late payments affect employment background checks?

Most employers do not see full credit reports, but in roles involving money or security, credit history may be reviewed, depending on state laws and job type.

-

Do mortgage late payments hurt more than credit card late payments?

Scoring models treat all late payments seriously, but lenders reviewing applications often view housing-related late payments as higher risk, especially for future mortgages.

-

If I settle or pay a collection, does the late payment disappear?

No. The original delinquency and the collection account may both remain reported, though payment prevents further collection activity and legal risk.

-

Can setting up payment plans stop reporting?

Payment plans may stop further late marks, but past late payments already reported usually remain until they age off.

-

Do credit monitoring services remove late payments?

No. Monitoring services only show changes. They cannot delete accurate negative information from your credit report.

-

Can I ask a lender to stop reporting late payments in the future?

Lenders may agree to special hardship programs or payment plans that prevent new late marks, but they usually cannot remove accurate late payments already reported.

Disclaimer

This content is provided for educational and informational purposes only and does not constitute legal, tax, or financial advice. Credit laws, lender policies, and individual financial situations can vary. For advice specific to your circumstances, consult a qualified financial advisor, credit counselor, or attorney.