Buying a car is one of the biggest financial decisions most Americans make outside of housing. Yet many people focus almost entirely on the monthly payment and overlook the interest rate, even though it plays a major role in how much the car truly costs.

Auto loan rates can vary dramatically from one borrower to another. Two people buying similar vehicles on the same day can receive very different APRs—sometimes separated by several percentage points. That difference doesn’t just affect your monthly bill; it affects how much of your income goes to interest instead of your future goals.

Confusion is common. People often assume the dealership will find them the “best rate,” that a longer loan automatically makes a car affordable, or that their credit score alone determines everything. None of those assumptions are fully accurate.

Understanding how auto loan rates really work—and how lenders decide what rate you get—puts you in control before you ever sign paperwork.

Key Takeaways

- Your credit profile, loan term, and where you borrow matter more than the car itself when it comes to auto loan APR.

- Preapproval before visiting a dealership gives you real negotiating power and helps you avoid marked-up financing.

- Shorter loan terms usually mean lower APRs, even though the monthly payment is higher.

- Rates vary widely by lender and borrower, and advertised “lowest rates” rarely apply to most buyers.

- Small differences in APR can cost—or save—you thousands of dollars over the life of a car loan.

What Is an Auto Loan APR?

APR (Annual Percentage Rate) is the yearly cost of borrowing money to buy a vehicle, expressed as a percentage. It includes:

- The interest rate

- Certain lender fees required to originate the loan

APR is not the same as your monthly payment. Two loans with similar monthly payments can have very different APRs—and very different total costs. A lower APR means:

- Less interest paid over time

- More of each payment goes toward the car, not the lender

In the U.S., lenders are required by federal law to disclose APR so borrowers can compare loan offers on equal terms.

How Auto Loan Rates Work in the United States

Auto loans in the U.S. are offered by:

- Banks

- Credit unions

- Online lenders

- Dealer-arranged financing (often through third-party lenders)

Each lender sets rates based on:

- Your creditworthiness

- Loan length

- Vehicle type and age

- Market interest rates

- Risk policies specific to that lender

There is no single “national” auto loan rate. Instead, rates exist in ranges, and you are placed somewhere within that range based on risk.

Lenders also price loans differently for:

- New vs. used vehicles

- Short vs. long terms

- Prime vs. subprime borrowers

Federal consumer protections and disclosure rules are enforced by agencies such as the Consumer Financial Protection Bureau (CFPB), but rate-setting itself is left to individual lenders.

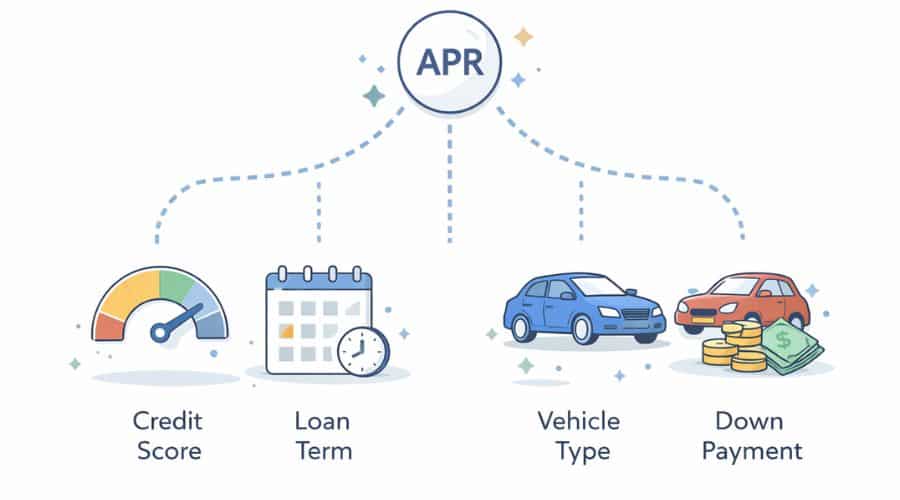

What Actually Determines Your Auto Loan APR

While lenders use different formulas, most auto loan rates are based on a small set of core risk factors.

1. Credit Score and Credit History

Your credit profile is usually the single most influential factor.

Lenders typically look at:

- Payment history

- Credit utilization

- Length of credit history

- Recent credit inquiries

- Types of credit accounts

A strong score with a thin or troubled history can still result in higher rates. Conversely, a slightly lower score with a long, clean history may receive better pricing.

2. Loan Term Length

Shorter terms usually get lower APRs.

| Loan Term | Typical APR Trend |

|---|---|

| 36 months | Lowest |

| 48 months | Low |

| 60 months | Moderate |

| 72–84 months | Highest |

Longer terms increase lender risk, so lenders charge more to compensate—even though the monthly payment looks smaller.

3. New vs. Used Vehicle

- New cars often qualify for lower rates

- Used cars carry higher APRs due to depreciation and resale risk

Older vehicles or high-mileage cars may face limited lender options.

4. Down Payment

A larger down payment:

- Reduces the loan amount

- Lowers the lender’s risk

- Can result in a lower APR

Zero-down loans often carry higher rates.

5. Where You Borrow

Rates vary significantly between:

- Banks

- Credit unions

- Online lenders

- Dealership financing desks

Credit unions, in particular, often offer lower average rates due to their nonprofit structure, though eligibility rules apply.

Why Preapproval Changes Everything

Getting preapproved before shopping for a car is one of the most effective ways to secure a low APR.

Preapproval means:

- A lender reviews your credit

- Offers a conditional rate and loan amount

- Locks terms for a short period (often 30–60 days)

This allows you to:

- Compare dealership financing against a real offer

- Avoid inflated rates marked up by dealers

- Focus negotiations on the vehicle price, not payment tricks

Who Is Most Likely to Qualify for the Lowest Auto Loan Rates

Borrowers who typically receive the best APRs:

- Have strong credit scores and clean histories

- Choose shorter loan terms

- Buy new or lightly used vehicles

- Make meaningful down payments

- Shop multiple lenders before committing

Who may struggle to get low rates:

- First-time borrowers with no credit history

- Buyers rolling negative equity into a new loan

- Those choosing very long loan terms

- Borrowers with recent delinquencies or high debt

Low rates are not a reward—they are a pricing decision based on risk.

Common Mistakes That Lead to Higher APRs

- Focusing only on the monthly payment

- Accepting the first offer without comparison

- Skipping preapproval

- Extending loan terms to “afford” a car

- Assuming dealer financing is automatically competitive

These mistakes often cost more than people realize, especially over 5–7 year loans.

Step-by-Step: How to Get the Lowest Auto Loan APR

Getting the best possible auto loan rate is mostly about preparation and timing—not luck. The steps below reflect how auto lenders in the U.S. actually evaluate borrowers and price risk.

Step 1: Check Your Credit Before You Apply

Before you talk to any lender or dealership, review your credit reports from all three major credit bureaus.

This allows you to:

- Spot errors that may be hurting your score

- Understand where you realistically fall in lender pricing tiers

- Avoid surprises after a hard credit pull

Important: Credit report errors are more common than many people realize, and even small inaccuracies can raise your APR.

Step 2: Improve What You Can (Even Small Changes Help)

You don’t need perfect credit to get a competitive rate, but you should address obvious red flags:

- Pay down high credit card balances

- Bring past-due accounts current

- Avoid opening new credit right before applying

- Limit loan applications to a short window

Even modest improvements can move you into a better rate bracket.

Step 3: Choose the Shortest Loan Term You Can Comfortably Afford

Long loan terms feel safer month to month, but they almost always cost more overall.

Key tradeoff to understand:

- Short term → higher payment, lower APR, less interest

- Long term → lower payment, higher APR, more interest

If affordability is tight, consider buying a less expensive vehicle rather than extending the loan length.

Step 4: Get Preapproved From at Least Two Lenders

Apply for preapproval from:

- A bank

- A credit union

- Or a reputable online lender

Multiple applications within a short period (typically 14–45 days, depending on scoring model) usually count as one inquiry for credit scoring purposes. This rate-shopping window is designed to encourage consumers to compare offers without being penalized for responsible shopping.

This lets you:

- Compare real APR offers

- Identify outliers

- Walk into the dealership with leverage

Step 5: Negotiate the Car Price Separately From Financing

Dealerships often mix price, trade-in value, and financing into one conversation. This makes it harder to see where money is being added.

Best practice:

- Negotiate the out-the-door vehicle price

- Finalize your trade-in (if any)

- Compare financing offers last

If the dealer can beat your preapproved rate, great. If not, you already have a solid backup.

Dealer Financing vs. Direct Lenders

Dealer-arranged financing is not automatically bad—but it requires caution.

How Dealer Financing Works

Dealers typically submit your application to multiple lenders and present you with the “best” offer they receive. However:

- The dealer may mark up the APR above the lender’s base rate

- The markup becomes profit for the dealership

- You may never see the unmarked rate unless you ask

When Dealer Financing Can Make Sense

- Manufacturer-sponsored promotional rates

- Situations where dealers match or beat preapproved offers

- Buyers with excellent credit during incentive periods

Always compare dealer financing against an outside preapproval.

Real-Life Example: How APR Changes Total Cost

Two borrowers finance the same $30,000 vehicle for 60 months.

| APR | Monthly Payment | Total Interest Paid |

|---|---|---|

| 4.5% | ~$560 | ~$3,600 |

| 7.5% | ~$602 | ~$6,100 |

Difference: About $2,500 in interest—without changing the car.

This is why APR matters even when the payment difference seems small.

Pros and Cons of Chasing the Lowest APR

| Pros | Cons |

|---|---|

| Lower total cost | May require shorter loan term |

| More money goes to principal | Stricter credit requirements |

| Faster equity buildup | Less flexibility for tight budgets |

| Easier refinancing later | Not always available for used cars |

A low APR is beneficial, but it should fit into a realistic budget, not force financial strain.

Myths vs. Facts About Auto Loan Rates

Myth: The dealership always gets the best rate

Fact: Many borrowers qualify for better rates elsewhere

Myth: Longer loans are cheaper because payments are lower

Fact: Longer loans almost always cost more overall

Myth: You must accept the rate you’re offered

Fact: Auto loan rates are negotiable—especially with alternatives

Myth: Checking rates will ruin your credit

Fact: Rate shopping within a short window usually has minimal impact

How Auto Loan Rates Affect Long-Term Finances

A higher APR doesn’t just affect your car—it affects:

- Your monthly cash flow

- Your ability to save or invest

- Your future borrowing costs

- Your risk of being underwater on the loan

Cars depreciate quickly. Paying excessive interest on a depreciating asset limits long-term financial flexibility.

Risks, Downsides, and Situations to Be Careful About

Even borrowers who secure competitive APRs can run into problems if the loan structure doesn’t match their financial reality.

Being “Underwater” on Your Loan

You are underwater when you owe more than the car is worth. This often happens when:

- You choose a long loan term

- You make a small or no down payment

- The car depreciates quickly

Being underwater limits your options if you need to sell, trade in, or refinance. It also increases the risk of financial stress if your income changes or the vehicle is totaled or stolen.

Warning: Rolling negative equity into a new loan almost always raises your APR and total cost.

Promotional Rates With Hidden Tradeoffs

Automaker-backed financing sometimes offers very low or even 0% APR. These offers can be legitimate, but they often come with conditions:

- Only available to top-tier credit

- Limited vehicle models or trims

- No flexibility on pricing or incentives

Sometimes a slightly higher APR paired with a lower vehicle price results in a better overall deal.

Add-Ons That Increase the Effective Cost

Extended warranties, protection packages, and other add-ons are often financed into the loan.

This means:

- You pay interest on those products

- The loan balance increases

- The APR may stay the same, but the total borrowing cost rises. This is why add-ons can quietly increase the true cost of financing, even when the interest rate looks reasonable.

Always evaluate add-ons separately from the loan itself.

Auto Loan Refinancing: When It Helps—and When It Doesn’t

Refinancing replaces your current auto loan with a new one, ideally at a lower APR.

Refinancing Can Make Sense If:

- Your credit has improved since you bought the car

- Market rates have dropped

- Your original loan had a high dealer markup

- You want to shorten the remaining term

Refinancing May Not Help If:

- The vehicle is very old or high-mileage

- You’re already near the end of the loan

- The savings are offset by fees

- You’re deeply underwater

Before refinancing, compare total remaining interest, not just the new monthly payment.

Special Situations That Affect Auto Loan Rates

Certain borrower profiles and life situations can affect how lenders price auto loans, even with similar credit scores.

First-Time Car Buyers

Lenders may charge higher APRs due to limited credit history, even with stable income. A co-signer can sometimes help—but only if they have strong credit and understand the responsibility.

Self-Employed Borrowers

Rates are often comparable, but lenders may require:

- Additional income documentation

- Longer review periods

- Conservative loan terms

Military Members

Active-duty service members have additional protections under federal law, including interest rate caps on certain pre-service obligations. Coverage depends on timing and loan details.

Common Beginner Misunderstandings

- “I can always refinance later.”

Refinancing is not guaranteed and depends on credit, vehicle value, and market rates. - “The payment fits, so the loan is fine.”

Payment size alone does not reflect total cost or risk. - “Rates are the same everywhere.”

Auto loan pricing varies widely by lender and borrower profile. - “New cars always get the best rates.”

Not if the borrower’s credit or loan structure is weak.

Frequently Asked Questions (FAQ)

These answers address common questions from U.S. car buyers, but individual offers and rates will always vary.

-

What is a good auto loan APR right now?

A “good” rate depends on credit profile, loan term, and vehicle type. Borrowers with strong credit typically qualify for the lowest tier available from a given lender, while others fall into higher ranges.

-

Does shopping for auto loans hurt your credit?

Rate shopping within a short time window is generally treated as a single inquiry for scoring purposes. Applying over several months can have a larger impact.

-

Is it better to finance through a bank or dealership?

Neither is always better. The best option is the one with the lowest total cost, after comparing APR, fees, and loan terms.

-

Can I negotiate an auto loan APR?

Yes. Having a preapproval gives you leverage to ask a dealer to match or beat your rate.

-

Do larger down payments lower APR?

Often, yes. A lower loan-to-value ratio reduces lender risk, which can result in better pricing.

-

Are online lenders safe for auto loans?

Many are legitimate, but borrowers should verify licensing, disclosures, and customer service access before committing.

Final Thoughts

The lowest auto loan rate isn’t reserved for experts or insiders. It usually goes to borrowers who prepare, compare offers, and understand how lenders price risk.

A car should support your life—not quietly drain your finances through avoidable interest costs. Taking the time to understand APR before you sign can protect your budget for years.

Disclaimer

This content is provided for educational and informational purposes only. It is not legal, tax, or financial advice. Auto loan terms, interest rates, and eligibility vary by lender, state, and individual circumstances. Readers should consult a qualified financial, legal, or tax professional before making personal financial decisions.