Key Takeaways

- Daily money account: Checking accounts are designed for everyday spending and bill payments.

- Easy access: You can use debit cards, checks, ATMs, and online transfers.

- Not for saving: These accounts usually earn little to no interest.

- Linked to income: Most people use checking accounts to receive paychecks and benefits.

- Affects financial stability: How you manage a checking account can impact fees, budgeting, and banking access.

Why Checking Accounts Matter in Everyday American Life

For most Americans, a checking account is the center of daily money activity.

It is where paychecks arrive, rent and utility bills get paid, debit cards pull money from, and automatic subscriptions are charged.

Without a checking account, many basic financial tasks become harder:

- Getting paid by an employer

- Paying bills online

- Avoiding expensive check-cashing services

- Managing money safely without carrying cash

Yet many people still feel confused about what a checking account actually is, how it works behind the scenes, and what rules control how banks handle these accounts. That confusion often leads to avoidable fees, declined payments, or account closures that could have been prevented with basic knowledge.

What Is a Checking Account? (Plain-English Definition)

A checking account is a bank or credit union account made for frequent money transactions, not long-term saving.

It allows you to:

- Deposit money

- Withdraw money

- Pay other people or businesses

- Move money electronically

Unlike savings accounts, checking accounts are built for regular activity, not storing money for months or years.

Think of it as your money traffic hub, not your storage vault. This is why most people keep only the money they plan to spend soon in checking, and move extra funds into savings.

How Checking Accounts Work in the United States

When you open a checking account, the bank creates a record that tracks:

- How much money you deposit

- How much you spend or withdraw

- Whether your balance goes below zero

- Whether fees apply

Your money is not stored as physical cash. Instead, it is recorded electronically and moved through U.S. payment networks when you use your account. Instead, banks track balances digitally and settle transactions between institutions through national payment systems.

Common Ways Money Moves Through Checking Accounts

| Method | What Happens |

|---|---|

| Debit card | Money is taken directly from your account when you swipe or tap. |

| Checks | Written instructions allowing someone to pull money from your account. |

| ACH transfers | Electronic payments used for payroll, bills, and subscriptions. |

| Wire transfers | Faster, usually paid transfers for large or urgent payments. |

| ATM withdrawals | Cash taken out using your debit card and PIN. |

Most transactions clear through national banking networks regulated by federal banking authorities, including the Federal Reserve and the CFPB (Consumer Financial Protection Bureau).

Where Checking Accounts Are Offered

In the U.S., you can open checking accounts at:

- Commercial banks

- Credit unions

- Online-only banks

All federally insured institutions protect deposits up to legal limits through:

- FDIC deposit insurance (banks)

- NCUA insurance (credit unions)

This insurance protects your money if the institution fails, but it does not protect you from losses caused by fraud, scams, or overdrafts unless the bank’s policies cover those situations.

What Checking Accounts Are Mainly Used For

Checking accounts support everyday financial life.

Typical Uses

- Receiving paychecks or government benefits

- Paying rent, utilities, and credit cards

- Buying groceries, gas, and online purchases

- Sending money to others

- Automatic bill payments

Because money moves in and out frequently, checking accounts are designed to process high transaction volume, not to grow money through interest.

Who Checking Accounts Are Best For

Checking accounts are appropriate for most adults who:

- Earn income

- Pay recurring bills

- Use debit cards or online payments

- Want electronic money access

They are also commonly used by:

- Students

- Retirees receiving Social Security

- Small business owners (with business checking accounts)

In modern U.S. financial systems, it is extremely difficult to function fully without some form of checking access.

Who Should Be Cautious With Checking Accounts

Checking accounts are not risk-free when mismanaged.

People who may face challenges include:

- Those who frequently spend more than their balance

- People with unstable income who risk overdrafts

- Anyone who ignores account alerts and statements

Most serious problems start small and grow because people stop checking balances regularly.

Important warning: Repeated overdrafts, unpaid fees, or suspected fraud can lead to account closure and reporting to banking databases that make opening future accounts harder.

This does not affect credit scores directly, but it can affect access to basic banking services.

Real-Life Example

Maria works full-time and gets paid every two weeks by direct deposit.

Her checking account:

- Receives her paycheck

- Pays her phone bill and rent automatically

- Covers grocery and gas spending

- Transfers leftover money to savings

When her account balance drops too low before payday, she risks overdraft fees if payments still process. Managing timing and balances matters more than the account type itself.

This example reflects how most Americans interact with checking accounts every day.

What Checking Accounts Are NOT Designed For

Checking accounts are not meant to:

- Grow your money

- Store emergency savings

- Earn meaningful interest or protect long-term savings from everyday spending decisions.

Even when banks offer interest-bearing checking accounts, the rates are usually far lower than savings accounts or other long-term options.

Using checking accounts for long-term storage increases the risk of:

- Spending money that should be saved

- Losing money to fees

- Missing better interest opportunities

Early Common Misunderstandings

Many beginners believe:

- “If money is in my account, I can spend it anytime safely.”

→ Pending transactions can still reduce your balance later. - “Banks will always block payments if I don’t have money.”

→ Some banks allow overdrafts and charge fees instead. - “Checking accounts help build credit.”

→ Regular checking activity does not build credit by itself.

Understanding these realities early prevents expensive surprises later.

Types of Checking Accounts in the United States

Not all checking accounts work the same way. Banks and credit unions offer different versions based on how people use their money, how much they keep in the account, and what services they need.

Understanding these types matters because fees, access, and protections can change significantly depending on the account structure.

Standard (Basic) Checking Accounts

This is the most common type of checking account used by adults. Most traditional bank checking accounts fall into this category.

Typical features

- Debit card access

- Online and mobile banking

- Bill pay and electronic transfers

- Check-writing (sometimes optional)

Common conditions

These accounts often waive fees only if certain rules are met.

- Monthly maintenance fee unless you meet certain requirements, such as:

- Maintaining a minimum balance

- Receiving qualifying direct deposits

- Linking another account at the same bank

Who this works best for

People who receive regular income and can meet the bank’s basic requirements to avoid monthly fees.

Free Checking (No Monthly Maintenance Fee)

Some institutions offer accounts advertised as “free checking.”

What “free” usually means

- No monthly maintenance fee

- No minimum balance requirement

What may still cost money. Many people assume “free” means no fees at all, which is not true.

- Overdraft fees

- Out-of-network ATM fees

- Paper statement fees

- Cashier’s check or wire fees

Important note: “Free” usually applies only to the monthly account fee, not to every possible service charge.

Who this works best for

People who want simple access without worrying about balance rules, and who can manage spending to avoid overdrafts.

Student Checking Accounts

Designed for high school and college students.

Typical features

- No or very low monthly fees

- No minimum balance requirement

- Debit card and mobile banking

- Limited or no overdraft options

Common restrictions

- Age limits

- Enrollment verification may be required

- Accounts may convert to standard checking after graduation. Fees and minimum balance rules may start applying after conversion.

Who this works best for

Students who need everyday banking while keeping fees low during school years.

Interest-Bearing Checking Accounts

These are often marketed as a way to earn interest while keeping spending access.

Some checking accounts pay interest on balances.

How they usually work

- Earn small amounts of interest

- Often require higher minimum balances

- May require debit card usage or direct deposits

Reality check

Interest rates on checking accounts are usually much lower than savings accounts, and requirements may make them harder to maintain without fees.

Who this works best for

People who keep larger balances and can easily meet activity requirements.

Joint Checking Accounts

Owned by two or more people together.

Common uses

- Couples managing shared bills

- Family members sharing expenses

Key responsibilities

- All account holders can withdraw money

- All account holders are legally responsible for overdrafts and fees. Banks do not mediate personal disputes over who caused the charges.

Important warning: Disputes or misuse by one person can affect everyone on the account.

Who this works best for

People with high trust and clear shared financial arrangements.

Second-Chance Checking Accounts

Designed for people who had banking problems in the past.

Why banks offer these

Some customers were previously reported for:

- Overdraft abuse

- Unpaid fees

- Suspected account misuse

These reports can block new account openings at many banks.

Typical features

- Limited services

- Monthly fees

- No overdraft options

Who this works best for

People rebuilding access to basic banking who may not qualify for standard accounts yet.

How Checking Account Fees Typically Work

Fees are one of the biggest differences between account types.

Common Fee Categories

| Fee Type | What Triggers It |

|---|---|

| Monthly maintenance | Not meeting balance or deposit rules |

| Overdraft fee | Spending more than available balance |

| ATM fee | Using machines outside the bank’s network |

| Paper statement fee | Receiving mailed statements |

| Wire transfer fee | Sending or receiving wire payments |

Fee structures vary widely by institution and state regulations.

Always reviewing the bank’s official fee schedule matters more than the account name.

Why Banks Set Rules on Checking Accounts

Banks use fees and requirements to:

- Cover transaction processing costs

- Limit account misuse

- Encourage stable balances and deposits

From a consumer side, the goal is to choose an account that matches your real money behavior, not the one with the best marketing name.

Choosing the Right Type Depends on Behavior, Not Income

A higher-income person who overspends can pay more in fees than a lower-income person who carefully manages balances.

What matters most:

- How often money moves in and out

- Whether income arrives regularly

- How closely you track balances

- Whether you rely on overdraft coverage

Account type cannot fix money habits, but the wrong account type can make problems more expensive.

Early Fee Mistakes Many People Make

Common beginner errors include:

- Ignoring minimum balance rules

- Not knowing when deposits actually clear

- Assuming debit card purchases always show instantly

- Forgetting automatic subscriptions

These mistakes often lead to overdraft charges even when people believe they had enough money.

Pros and Cons of Checking Accounts

Checking accounts play a central role in personal finance, but they are not perfect tools. Understanding both benefits and drawbacks helps avoid unrealistic expectations and poor money decisions.

Pros and Cons Overview

| Pros | Cons |

|---|---|

| Easy access to money | Low or no interest earnings |

| Supports direct deposit and bill pay | Overdraft fees can be expensive |

| Safer than carrying cash | Some accounts charge monthly fees |

| Widely accepted for payments | Not designed for long-term saving |

| Helps track spending digitally | Account misuse can lead to closure |

Major Benefits of Using a Checking Account

1. Convenient Access to Money

Checking accounts allow quick access through:

- Debit cards

- ATMs

- Online transfers

- Mobile payment apps

This makes everyday transactions simple and fast without needing physical cash.

2. Direct Deposit and Automatic Payments

Most employers and government agencies pay benefits using direct deposit.

Checking accounts also support:

- Rent payments

- Utility bills

- Insurance premiums

- Subscription services

Automation reduces missed payments and late fees when balances are managed properly. his also helps maintain consistent payment history on credit accounts, which can indirectly support credit health.

3. Strong Consumer Protections

Federal rules limit consumer liability for unauthorized transactions when reported promptly.

Protections can include:

- Fraud investigation rights

- Provisional credit during disputes

- Transaction monitoring by banks

Important: Protection depends on reporting suspicious activity quickly and following bank procedures. Delays in reporting can reduce or eliminate reimbursement rights under federal rules.

4. Spending Records and Budgeting Support

Every transaction is logged, allowing people to:

- Review statements

- Track categories of spending

- Identify mistakes or fraud

This data becomes useful for budgeting and financial planning.

Downsides and Risks of Checking Accounts

1. Overdraft Fees Can Add Up Quickly

Overdrafts happen when spending exceeds available balance.

Consequences may include:

- Per-transaction fees

- Extended overdraft fees if not repaid quickly

- Account suspension

Even small purchases can trigger large fees if the account is already low. Multiple transactions in the same day can result in several fees from a single low balance.

2. Monthly Maintenance Fees

Some accounts charge monthly fees unless conditions are met, such as:

- Minimum balances

- Regular direct deposits

Missing those conditions can quietly reduce account balances over time.

3. Easy Access Can Encourage Overspending

Because money is instantly available:

- People may spend without checking balances

- Automatic charges may pile up unnoticed

Convenience can weaken spending awareness if balances and transactions are not reviewed regularly.

4. Account Closure Can Limit Future Banking Access

Repeated overdrafts, unpaid fees, or suspicious activity may lead to:

- Account termination

- Reporting to banking history databases

- Difficulty opening new accounts elsewhere

This does not affect credit scores directly, but it affects access to basic financial services.

Behavioral Impact: How Checking Accounts Shape Money Habits

Checking accounts influence how people manage money psychologically.

They can:

- Encourage quick spending

- Make money feel abstract

- Hide real-time balances due to pending transactions

People who treat checking accounts as spending tools — not storage — usually avoid more problems.

Separating savings into different accounts helps prevent accidental spending.

When Checking Accounts Create False Security

Some users assume:

- Banks will block transactions if money is insufficient

- Overdraft protection means no consequences

In reality:

- Transactions may still go through

- Fees may apply afterward

Understanding how balances and authorizations work matters more than relying on bank safeguards.

Who Might Need Extra Caution

People who should monitor checking accounts more carefully include:

- Those with irregular income

- People managing multiple subscriptions

- Anyone living close to paycheck-to-paycheck

In these situations, timing of deposits and withdrawals becomes critical. Even one delayed paycheck or early bill can cause multiple payments to fail or overdraft.

How Checking Accounts Affect Credit, Taxes, and Legal Responsibilities in the U.S.

Checking accounts are not credit products, but they still interact with important parts of the U.S. financial system. Misunderstanding these connections often leads to confusion about credit scores, tax reporting, and legal liability.

Do Checking Accounts Affect Your Credit Score?

Directly: No.

Regular checking account activity does not appear on your credit report and does not help build credit.

That means:

- Deposits do not raise credit scores

- Paying bills from checking does not build credit

- Keeping high balances does not improve credit

Credit bureaus track credit accounts, not deposit accounts.

When Checking Accounts Can Indirectly Affect Credit

Checking accounts can affect credit only in limited situations:

- Unpaid Overdraft Fees Sent to Collections

If a bank closes an account with unpaid negative balances and sends the debt to collections, that collection account may appear on your credit report. - Linked Credit Products

If checking is connected to:- Overdraft lines of credit

- Credit cards

Then missed payments on those credit products can affect credit scores.

But normal checking activity alone does not build or damage credit.

Banking History Databases (Not Credit Bureaus)

Banks often use specialized databases to track account behavior. These databases are used only by banks and credit unions, not by landlords, employers, or credit card companies.

These systems may record:

- Repeated overdrafts

- Unpaid balances

- Suspected fraud

- Account abuse

If reported, future banks may deny new account applications even if your credit score is good.

Important distinction:

This is separate from credit reports and is used only by financial institutions, not lenders.

Are Checking Accounts Reported to the IRS?

Usually, regular checking account transactions are not reported to the IRS.

However, banks may report certain information:

Situations That Trigger IRS Reporting

Banks are required to report certain financial activity under federal law, regardless of account type.

- Interest earned above federal reporting thresholds

- Large cash transactions (typically $10,000 or more in cash deposits or withdrawals)

- Certain business-related activities

If interest is earned, banks issue tax forms showing:

- Amount of interest paid

- Account holder information

That interest may be taxable interest income depending on your tax situation.

Are Deposits Taxable?

Deposits themselves are not automatically taxable.

Examples of non-taxable deposits:

- Transfers from your own accounts

- Refunds

- Personal gifts (with exceptions for gift tax rules)

Examples of potentially taxable deposits:

- Paychecks

- Business income

- Investment income

Tax responsibility depends on where the money came from, not where it is deposited.

Banks do not determine tax obligations — they only report certain required information to the IRS.

Legal Ownership and Responsibility

Individual Accounts

Only the named account holder is legally responsible for:

- Fees

- Overdrafts

- Account misuse

Joint Accounts

All account holders are fully responsible.

That means:

- One person’s spending can overdraft the account

- Both people are responsible for repaying fees

- Legal disputes do not change bank responsibility

Banks do not divide responsibility between account holders. Even if one person caused the overdraft, the bank can legally collect from any account holder.

What Happens If a Checking Account Goes Negative

If an account is overdrawn and not repaid:

- Fees may continue to accumulate

- The bank may close the account

- The unpaid balance may be sent to collections. Collection agencies may attempt to recover the debt and may charge additional fees or interest.

- Banking history databases may be updated

This can limit access to future banking and increase financial stress.

Consumer Rights and Protections

U.S. law provides certain protections for checking account holders.

These rules are enforced by the Consumer Financial Protection Bureau and other banking regulators.

These include:

- Right to dispute unauthorized transactions

- Error resolution timelines

- Disclosure of fees and terms

- Limits on liability if fraud is reported promptly. Federal law sets specific deadlines for reporting, often within days or weeks, depending on the situation.

However, protections apply only if:

- The customer reports issues within required timeframes

- Account terms were followed

Ignoring statements or alerts can weaken legal protections.

Why Legal and Regulatory Rules Matter for Everyday Users

Checking accounts feel simple, but they operate under federal banking laws and payment regulations.

These rules determine:

- How fast disputes are handled

- Whether banks must reimburse fraud

- What fees can legally be charged

Understanding that checking accounts are regulated financial products — not casual apps — helps people take account management more seriously.

Common Mistakes, Myths, and How Problems Start

Most checking account problems are not caused by complicated banking rules. They usually start with small misunderstandings that slowly turn into fees, declined payments, or account closures.

Clearing up these myths early can prevent long-term frustration.

Common Myths About Checking Accounts

Myth 1: “If my card works, I must have enough money.”

Fact:

Card authorizations and final charges can happen at different times. A purchase may be approved, but the actual charge can post later when your balance is lower.

This is common with:

- Restaurants

- Gas stations

- Hotels

- Online merchants

Pending charges can reduce available funds even if your balance looks higher. This is why checking available balance is more important than checking posted balance.

Myth 2: “Banks always block transactions if I don’t have enough money.”

Fact:

Many banks allow transactions to go through and then charge overdraft fees afterward, depending on your account settings and the type of transaction.

Blocking is not guaranteed protection.

Myth 3: “Overdraft protection means I won’t be charged.”

Fact:

Overdraft protection may move money from another account or credit line, but fees can still apply depending on the bank’s policy and the funding source.

Myth 4: “Keeping money in checking is the same as saving.”

Fact:

Checking accounts are spending tools, not storage tools. Easy access increases the chance that money meant for future needs gets spent.

Myth 5: “If my account closes, I can just open another one anywhere.”

Fact:

Account closures with unpaid balances or misuse may be visible to other banks, making new account approval harder for a period of time.

Small Mistakes That Often Lead to Fees

Many problems start with habits that seem harmless.

Common Triggers

- Not checking balances before spending

- Forgetting about subscriptions and automatic bills

- Assuming deposits are immediately available

- Relying on overdraft instead of adjusting spending

- Ignoring account alerts and statements

- Not updating payment dates when income timing changes

One missed deposit or delayed paycheck can trigger multiple fees if several payments post at once.

Timing Issues: When Money Leaves Faster Than Expected

Transaction timing plays a major role in checking account management.

Why Timing Causes Trouble

- Deposits may take time to fully clear

- Merchants may delay posting final charges

- Automatic payments may process overnight

As a result, balances can drop unexpectedly even when spending seems normal.

Tracking available balance, not just posted balance, matters most.

How People End Up With Account Closures

Banks usually close accounts after repeated problems, not one mistake.

Patterns That Raise Risk

- Frequent overdrafts

- Unpaid negative balances

- Suspected unauthorized activity

- Ignoring bank communications

Once closed, restoring access can be difficult, especially if fees remain unpaid. Some people may need to use restricted or second-chance accounts before qualifying for regular checking again.

Emotional Side of Checking Account Stress

Financial stress often increases when:

- Payments bounce

- Cards get declined

- Fees reduce already tight budgets

This can lead to avoidance, where people stop checking balances altogether, which makes problems worse.

Simple daily awareness often prevents major financial disruption.

What Helps Prevent Most Checking Account Problems

The most effective habits are simple:

- Checking balances before large purchases

- Keeping a small buffer above zero whenever possible

- Reviewing transactions weekly

- Turning on alerts for low balances

These actions do not require advanced financial knowledge, just consistency.

When to Reevaluate Your Account Type

If problems happen repeatedly, it may not be only behavior — the account itself may not fit your situation.

Reevaluation may help if:

- Monthly fees keep applying

- Overdraft happens often

- Minimum balance rules are hard to meet

Choosing an account that matches income timing and spending patterns can reduce pressure.

Checking Accounts vs. Savings Accounts: How They Function Differently in Real Life

Although both are bank deposit accounts, checking and savings accounts serve very different roles in personal finance. Confusing those roles often leads to overspending, missed savings goals, and unnecessary fees.

This section focuses on how they function differently in everyday use, not on how to open them or formal definitions already covered in your other articles.

Core Functional Differences

| Feature | Checking Account | Savings Account |

|---|---|---|

| Primary purpose | Spending and payments | Storing money |

| Transaction volume | High | Low to moderate |

| Debit card access | Usually yes | Rare or limited |

| Bill pay and subscriptions | Yes | Not designed for |

| Interest earnings | Very low or none | Higher than checking |

| Psychological role | “Money to use” | “Money to keep” |

How Americans Commonly Use Both Together

In healthy money systems, both accounts work as a pair.

Typical Setup

- Checking: receives income and pays expenses

- Savings: holds money for emergencies and short-term goals

Money moves from checking to savings, not the other way around except during emergencies or planned spending.

This separation helps protect savings from everyday spending decisions.

Why Savings Accounts Are Not Ideal for Daily Spending

Savings accounts may allow transfers, but they are not designed for frequent transactions.

Issues that arise when savings is used like checking:

- Limited electronic payment options

- Slower transfers

- Fewer fraud protections for debit spending

- Reduced savings discipline

Savings accounts are structured to slow down spending, not make it faster. This delay acts as a natural barrier that protects savings from impulse purchases.

Why Checking Accounts Are Risky for Long-Term Storage

Keeping large balances in checking increases exposure to:

- Spending temptation

- Subscription creep

- Lower interest earnings

- Greater fraud risk due to frequent transactions

- More exposure if debit card details are compromised

Even small interest differences matter over time when balances grow.

When People Blur the Line Between the Two

This often happens when:

- Income is irregular

- Expenses are unpredictable

- Emergency savings are not built yet

In these situations, people may pull from savings often or leave extra money in checking, which weakens the purpose of both accounts.

Behavioral Impact of Account Separation

Psychologically, people treat money differently based on where it is stored. This effect is well documented in behavioral finance research.

Money in checking feels:

- Available

- Spendable

- Part of daily routine

Money in savings feels:

- Reserved

- Harder to touch

- Protected for future needs

This mental separation improves financial control without complex budgeting tools.

When Using Only One Account Becomes a Problem

Some people try to manage everything in a single checking account.

Risks include:

- No emergency buffer

- Higher chance of overdraft

- No mental boundary between spending and saving

Over time, this often leads to financial instability even when income is sufficient. The problem is usually cash flow management, not total income.

Why Banks Encourage Both Accounts

Banks design products assuming people will use both:

- Checking for transactions

- Savings for reserves

This structure aligns with:

- Federal banking rules

- Payment system design

- Consumer protection frameworks

Using accounts as intended reduces both system-level processing problems and personal financial risk.

Key Reality

Checking accounts help money move.

Savings accounts help money stay.

Using each for its intended role simplifies money management more than most people realize.

How Checking Account Transactions Actually Clear (and Why Balances Change Unexpectedly)

Many checking account problems happen not because people overspend, but because they misunderstand when money actually leaves the account. The timing of transactions can be confusing, even for careful users.

Understanding this process helps prevent overdrafts and declined payments.

Two Balances: Posted Balance vs. Available Balance

Banks usually show two numbers:

- Posted (ledger) balance — transactions that have fully processed

- Available balance — money you can safely spend right now

Pending transactions reduce available balance even if they have not fully posted yet.

Relying only on posted balance can lead to accidental overspending.

Step-by-Step: What Happens When You Use Your Debit Card

- Authorization

The merchant asks your bank if funds are available.

If approved, the amount is temporarily held. - Pending Stage

The transaction shows as pending.

The money is not yet fully withdrawn but is reserved. - Final Posting (Settlement)

The merchant completes the charge, and money officially leaves your account.

This process can take one to several business days, depending on the merchant and payment network. Until final posting happens, your available balance remains reduced by the pending amount.

Why Some Charges Change Amounts

Certain businesses adjust final amounts after authorization.

Examples include:

- Restaurants adding tips

- Gas stations estimating fuel amounts

- Hotels placing large temporary holds

Final charges may be higher or lower than the original hold.

How Deposits Clear

Deposits also go through stages.

Common Deposit Types

| Deposit Type | Typical Clearing Behavior |

|---|---|

| Direct deposit (payroll) | Often available same day |

| Cash deposits | Usually immediate |

| Check deposits | May be partially available first |

| Mobile check deposits | Often delayed |

Banks may release part of a deposit first and hold the rest until the check fully clears. Holds are applied to protect banks from returned or fraudulent checks.

This means seeing a deposit does not always mean all funds are usable immediately.

Why Automatic Payments Can Surprise People

Automatic payments may process:

- Early in the morning

- On weekends or holidays

- Before deposits become available

This is common when bills are scheduled for the same day as payday.

So timing matters even when income and bills are predictable.

Why Declines and Overdrafts Can Happen Together

It may seem confusing, but:

- Some transactions are declined immediately

- Others are approved and charged later with fees

This depends on:

- Transaction type

- Bank policies

- Available overdraft coverage

There is no single rule that applies to every purchase.

Why Weekend and Holiday Timing Matters

Bank processing usually follows business days.

This can cause:

- Delays in deposit availability

- Multiple payments posting at once

- Larger balance swings after weekends. Several days of transactions may settle at once when banks reopen.

Planning for non-business days helps avoid surprises.

What Helps Manage Timing Risks

Helpful habits include:

- Tracking available balance, not just posted balance

- Leaving a small cushion in the account whenever possible

- Reviewing pending transactions

- Scheduling payments after deposit days when possible

These steps reduce dependence on overdraft systems.

Why This Matters for Long-Term Stability

Repeated timing mistakes can create cycles of:

- Fees

- Negative balances

- Stress-driven financial decisions

Understanding clearing timelines gives people more control without needing complex tools.

Who Should Avoid Certain Checking Account Features (and How to Reduce Fee Risk)

Not all checking account features are helpful for everyone. Some options are convenient for certain users but risky for others, especially when income or balances are unpredictable.

Knowing which features to limit can reduce unnecessary fees.

Overdraft Services: Helpful for Some, Risky for Others

Overdraft services allow transactions to go through when there isn’t enough money in the account. Whether overdraft is allowed depends on bank policy and customer opt-in settings for certain transactions.

When Overdraft May Help

- Prevents declined rent or utility payments

- Avoids late-payment consequences with essential bills

When Overdraft Creates More Harm

- Small purchases trigger large fees

- Multiple charges stack up quickly

- Negative balances become hard to recover from

Critical warning:

Overdraft should not be used as a budgeting tool. It is a short-term safety net, not income support.

Debit Card Overdraft vs. ACH Overdraft

Not all overdrafts happen the same way.

| Transaction Type | How Overdraft Happens |

|---|---|

| Debit card | May be declined or allowed with fee |

| Automatic bill payments (ACH) | Often processed even if funds are low |

| Checks | Usually processed and may create overdraft |

Some people turn off debit card overdraft but still experience overdrafts from automatic bills.

Automatic Payments: Convenience With Hidden Risks

Auto-pay prevents late bills, but it can:

- Pull money before deposits arrive

- Trigger overdrafts if balances are tight

- Continue charging forgotten subscriptions.

Automatic payments work best when income timing is stable and balances are monitored.

Mobile Deposits and Funds Availability

Mobile check deposits are convenient, but:

- Holds may apply

- Funds may not be fully available immediately

- Rejected checks can reverse deposits later

Relying on mobile deposits to cover same-day expenses can increase overdraft risk.

Alerts and Account Controls That Reduce Risk

Most banks offer free alerts that notify users of:

- Low balances

- Large transactions

- Deposits posting

- Payment failures

Turning these on helps people react before fees occur.

When to Consider Account Changes

Switching account types or banks may help when:

- Monthly fees keep applying

- Overdraft happens often

- ATM access is limited

- Account rules no longer match income patterns

Account terms are not permanent contracts. Changing accounts is allowed and often practical.

Who Benefits From Tighter Account Controls

People who may benefit from limiting certain features include:

- Those paid irregularly

- Students managing small balances

- Anyone recovering from past overdraft issues

Simpler accounts with fewer automatic features may reduce financial stress.

Why Fewer Features Can Sometimes Mean Fewer Problems

More tools mean more ways money can leave automatically.

Reducing:

- Auto-pay

- Stored card numbers

- Overdraft coverage

can increase awareness and reduce accidental spending.

The Goal Is Control, Not Restriction

Account features should support your behavior, not override it.

When users control how money moves, they avoid relying on bank safety nets that often come with fees.

Myths, Marketing Language, and Deeper Misunderstandings About Checking Accounts

Banks often use simple labels and attractive terms when describing checking accounts. While not dishonest, this marketing language can hide important details that affect real-world costs and account behavior.

Understanding what common terms really mean helps avoid unrealistic expectations.

“Free Checking” Does Not Mean Free Banking

Many people assume “free checking” means no charges at all.

In reality, it usually means:

- No monthly maintenance fee

It does not automatically mean:

- No overdraft fees

- No ATM fees

- No service charges for special transactions

Always separate monthly fees from transaction fees when evaluating accounts. Reviewing the full fee schedule is the only way to understand total costs.

“Overdraft Protection” Is Not the Same as Overdraft-Free

The term “protection” suggests safety, but overdraft services often mean:

- Transactions go through

- Fees are charged afterward

In some setups, money is transferred from another account or credit line, which may still involve fees or interest.

Protection reduces payment failures, not financial cost. In some cases, linked credit lines can also add interest charges on top of transfer fees.

“Premium” or “Advantage” Account Labels

Some accounts use labels like:

- Advantage

- Preferred

- Premium

These names often signal:

- Higher balance requirements

- More features

- Higher fee thresholds

They are not guarantees of better financial outcomes.

Marketing Focus vs. Practical Reality

Advertisements emphasize:

- Mobile apps

- Fast payments

- Convenience

But they rarely emphasize:

- Fee schedules

- Balance rules

- Overdraft conditions

The most important details are usually found in the account disclosure documents, not marketing pages.

Deeper Misunderstanding: Confusing Access With Ownership

Some people believe that because money is in their account:

- It can always be spent instantly

- Banks cannot restrict access

In reality, banks may:

- Freeze accounts during fraud investigations

- Delay certain transactions

- Reverse deposits that do not clear. These actions are allowed under banking agreements and fraud prevention laws.

Access to funds is subject to banking rules and verification processes.

Why People Underestimate Fee Risk

Fee risk is often underestimated because:

- Fees are small individually

- Charges happen after the transaction

- The trigger is not always obvious

Over time, repeated small fees can become a significant financial drain.

Another Misunderstanding: “I’ll Fix It Next Paycheck”

When overdrafts happen, people often plan to fix balances after their next deposit.

Problems arise when:

- Multiple payments hit before payday

- Fees reduce the incoming deposit

- The cycle repeats

This creates a pattern where each paycheck mostly repairs past fees instead of supporting current needs. Over time, this reduces financial progress even if income stays the same.

Why Reading Account Terms Matters More Than People Expect

Account disclosures explain:

- When fees apply

- When deposits are available

- What actions can close accounts

Most people skip these documents, but they control the real financial outcomes.

Understanding even the basic fee section can prevent costly surprises.

Marketing vs. Financial Fit

An account can look modern and convenient but still be a poor match for someone who:

- Lives close to zero balance

- Has irregular income

- Uses many automatic payments

Fit matters more than features.

When Checking Accounts May Not Be the Best Option (and What People Use Instead)

Checking accounts work well for most people, but they are not the only way Americans manage everyday money. In certain situations, alternatives may feel easier or more accessible, though they come with their own trade-offs.

Understanding these options helps people make informed choices rather than defaulting to costly services.

Situations Where People Avoid Traditional Checking Accounts

Some people avoid or lose access to checking accounts due to:

- Past overdraft problems

- Unpaid account balances

- Lack of required identification

- Distrust of banks

- Irregular income patterns or previous account closures reported to banking databases

In these cases, people often turn to non-bank financial tools.

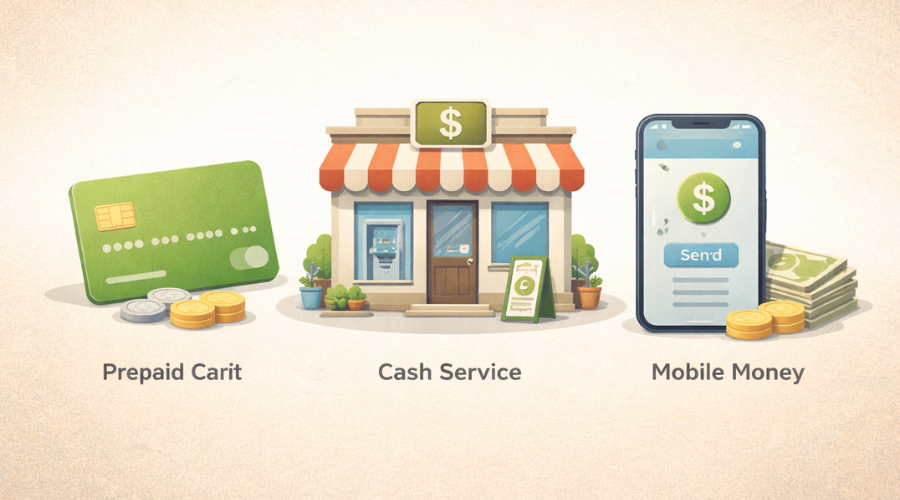

Prepaid Debit Cards

Prepaid cards allow users to load money and spend until the balance reaches zero.

How They Work

- Money is added in advance

- No overdraft is possible

- Card works for most purchases

Limitations

- Monthly or per-transaction fees

- Limited bill-pay options

- Less protection for disputes compared to federally regulated bank checking accounts

- Not all employers support direct deposit

Prepaid cards reduce overdraft risk but often increase service fees.

Check-Cashing Services

Some people rely on check-cashing stores to access income.

Why People Use Them

- Immediate access to cash

- No bank account required

Major Downsides

- High percentage-based fees

- No place to store money safely

- No electronic bill payment options

Over time, fees from check-cashing services can exceed typical bank fees by a large margin especially for people paid weekly or biweekly.

Cash-Only Systems

A few people try to operate fully in cash.

Risks Include

- Theft or loss

- No fraud protection

- No transaction history

- Difficulty paying modern bills

Cash works for small purchases but not for long-term financial stability.

Online Financial Platforms

Some online platforms offer money accounts with debit cards.

Common Features

- Mobile apps

- Early access to deposits

- Budgeting tools

Important Considerations

- Not all are traditional banks

- Deposit insurance varies by structure and may not be the same as FDIC or NCUA coverage in all cases.

- Dispute resolution may differ

Understanding who actually holds the money matters for consumer protection.

Why Traditional Checking Still Matters

Despite alternatives, checking accounts remain central because they support:

- Employer payroll systems

- Government benefit payments

- Automated bill infrastructure

- Legal deposit insurance

Most large-scale payment systems in the U.S. are built around checking accounts.

When Alternative Options May Make Sense Temporarily

Alternatives may serve as short-term solutions when:

- Rebuilding banking access

- Waiting for account approval

- Managing strict spending limits or while resolving identity or documentation issues

But long-term reliance on non-bank services often increases costs and limits financial flexibility.

Returning to Traditional Banking After Problems

Many people who had account closures can eventually return to standard banking by:

- Paying off negative balances

- Using restricted accounts temporarily

- Demonstrating stable account behavior

Time and improved account management usually restore eligibility.

Choosing Based on Total Cost, Not Just Access

Access alone does not equal affordability.

People often pay more over time through:

- Per-transaction fees

- Reload fees

- Service charges

Even fee-based checking accounts may cost less than alternatives when used responsibly. Reviewing monthly and annual fees together gives a clearer picture than looking at single charges.

Long-Term Financial Impact of How You Use a Checking Account

Checking accounts may seem like short-term tools for daily spending, but the way they are managed can influence long-term financial stability more than most people expect.

Patterns repeated every month shape future financial options.

Fee Cycles Reduce Money Available for Savings

When fees occur regularly, they:

- Reduce usable income

- Delay savings goals

- Increase reliance on future deposits to recover which can trap people in a cycle where each paycheck repairs past problems instead of building stability.

Over time, even modest monthly fees can prevent emergency funds from growing.

Missed Payments Can Trigger Larger Financial Problems

If checking account issues cause:

- Rent payments to fail

- Utility bills to bounce

- Loan payments to post late

Then consequences may include:

- Late fees

- Service interruptions

- Damage to credit on unrelated accounts

A checking account does not affect credit directly, but payment failures absolutely can.

Banking Access Affects Financial Opportunities

Stable banking access helps with:

- Faster payroll deposits

- Easier bill management

- Lower transaction costs

Limited access may force people into:

- Fee-based services

- Slower payment methods

- Fewer financial options

This creates ongoing friction in everyday finances and makes long-term financial planning harder.

Checking Accounts and Financial Planning

People who manage checking accounts well tend to:

- Maintain emergency savings

- Separate spending and saving

- Track recurring expenses

These habits support:

- Debt reduction

- Investment readiness

- Financial resilience

Good account management does not guarantee wealth, but poor management almost guarantees ongoing stress.

Relationship Between Income Stability and Account Stability

When income is unpredictable:

- Timing mistakes become more likely

- Auto-pay may conflict with deposit dates

- Overdraft risk increases

This makes monitoring and buffer planning even more important.

Account structure cannot replace income stability, but it can reduce added pressure. Choosing accounts with flexible fee rules becomes especially important when income varies.

How Checking Behavior Signals Financial Readiness

Banks and financial institutions often evaluate behavior patterns indirectly when offering:

- New accounts

- Credit products

- Premium services

Responsible account management supports broader financial credibility even if not shown on credit reports. This can affect how easily people qualify for standard banking services later.

Preventing Problems Is Easier Than Fixing Them

Once accounts are closed or balances go negative:

- Recovery takes time

- Fees may accumulate

- Access may remain limited temporarily

Preventive habits cost far less than repair efforts later.

Small Habits With Big Long-Term Effects

Long-term stability often comes from:

- Checking balances regularly

- Keeping small spending buffers when possible

- Reviewing statements monthly

- Adjusting automatic payments when income changes

These habits protect financial momentum.

Why This Matters Even When Money Is Tight

People under financial pressure often have less margin for error.

That makes:

- Fee avoidance

- Deposit timing

- Expense tracking

even more critical, not less.

Better checking management does not fix income gaps, but it reduces avoidable losses.

Frequently Asked Questions About Checking Accounts

These are real questions Americans commonly search when trying to understand or manage checking accounts.

Can I have more than one checking account?

Yes. Many people keep multiple checking accounts for different purposes, such as:

– One for bills

– One for daily spending

– One shared with a partner

There is no federal limit on how many checking accounts a person can have, as long as bank requirements are met. Each bank may still apply its own approval rules and minimum balance requirements.

Is my money safe in a checking account?

Money is protected against bank failure through:

– FDIC insurance at banks

– NCUA insurance at credit unions

Coverage applies up to legal limits per depositor per institution. Different accounts at the same bank may be combined for insurance purposes depending on ownership category.

However, insurance does not protect against:

– Authorized spending

– Scams where you willingly send money

– Overdraft fees

Fraud protection depends on reporting issues quickly and following bank procedures.

How quickly should I report unauthorized transactions?

As soon as you notice them.

Federal rules protect consumers, but:

– Delays can increase liability

– Banks may deny reimbursement if reports are late. Some protections require reporting within very short timeframes, sometimes within two business days.

Reviewing statements and alerts regularly improves protection.

Can a bank close my checking account without warning?

Yes, banks can close accounts if they believe there is:

– Repeated misuse

– Unpaid negative balances

– Suspicious activity

– Policy violations

Banks usually notify customers, but closures can happen quickly in fraud situations. Most closures are triggered by repeated issues, not single small mistakes.

What happens to automatic payments if my account is closed?

Payments may:

– Be declined

– Trigger late fees from billers

– Affect credit if loans or rent are involved

Updating payment methods immediately after account issues is critical to avoid further problems. Contacting major billers directly can sometimes prevent penalties if done quickly.

Are checking accounts required to have fees?

No. Many institutions offer accounts without monthly maintenance fees, but:

– Other fees may still apply

– Fee structures depend on bank policies

Reviewing the full fee schedule matters more than the account name. Fee schedules are usually available on bank websites and account disclosure documents.

Can checking accounts earn interest?

Some do, but:

– Rates are usually low

– Requirements may be strict

– Savings accounts usually pay more

Checking accounts are not designed for interest growth.

Does closing a checking account hurt my credit score?

Closing a checking account itself does not affect credit scores.

However, if the account closes with unpaid fees and the debt goes to collections, that collection account may affect credit. The original checking account itself is still not reported as a credit account.

Can my checking account be garnished?

In certain legal situations, courts may order banks to freeze or take funds for:

– Unpaid debts

– Child support

– Tax obligations

Some income sources may have legal protections, but rules depend on the type of debt and court orders. Banks must follow legal instructions and usually cannot release frozen funds without court approval.

Why do banks put holds on deposits?

Holds help banks manage risk when:

– Checks may bounce

– Deposits are large

– Account history shows past problems

Funds may appear in the account but not be fully available to spend yet. Spending unavailable funds can still trigger overdraft fees.

Should I keep emergency money in checking?

Generally no.

Emergency funds are safer in savings because:

– They earn more interest

– They are less likely to be spent accidentally

– They are not exposed to daily transaction risk

Checking should hold short-term spending money, not emergency reserves.

Can I switch banks easily if I’m unhappy?

Yes, but switching requires planning:

– Redirect direct deposits

– Update automatic payments

– Transfer remaining balances

Keep the old account open until all payments and deposits are confirmed switched.

Switching is allowed and common, but timing matters to avoid missed payments.

Why do some people struggle with checking accounts even with good income?

Problems often come from:

– Poor timing awareness

– Too many automatic payments

– No spending buffer

Income alone does not prevent overdrafts or fees.

Final Practical Perspective

A checking account is not just a place where money sits. It is a working financial tool that moves income, pays bills, and supports everyday life.

When used well, it helps people:

- Receive money reliably

- Pay obligations on time

- Track spending clearly

- Avoid high-cost financial services

When misunderstood or unmanaged, it can create:

- Repeated fees

- Missed payments

- Banking access problems

- Ongoing financial stress

The difference usually comes down to awareness of:

- How transactions clear

- How fees are triggered

- How automatic payments interact with income timing and how much buffer is kept in the account

Checking accounts are most effective when paired with savings accounts, monitored regularly, and matched to real income and spending patterns.

No account type can replace budgeting or income stability, but the right account structure can reduce friction and protect limited resources.

Disclaimer

This content is provided for educational and informational purposes only and is not intended as legal, tax, or financial advice.

Banking rules, fee structures, tax obligations, and consumer protections can vary by institution, state, and individual circumstances.

Readers should consult a qualified financial, legal, or tax professional for advice specific to their personal situation before making financial decisions.

5 thoughts on “What Is a Checking Account? How It Works, Types, Fees & Common Mistakes (U.S. Guide 2026)”