Key Takeaways at a Glance

- A credit card lets you borrow money from a bank or issuer to make purchases, up to a preset credit limit.

- You repay what you borrow later—either in full or over time—with interest if you carry a balance.

- Used carefully, credit cards can help with cash flow, fraud protection, and credit history.

- Used poorly, they can lead to high interest costs, debt stress, and credit damage.

- In the U.S., credit cards are governed by federal consumer protection laws, but terms still vary by issuer and by your personal credit profile.

Why credit cards matter in everyday American life

For many Americans, credit cards sit quietly behind daily decisions—paying for groceries, booking travel, handling an emergency car repair, or shopping online. They’re also one of the most common ways people build or damage their credit history, which affects future borrowing costs for auto loans, mortgages, and even insurance pricing in some states.

At the same time, credit cards are widely misunderstood. Some people assume they’re free money. Others avoid them entirely out of fear of debt. The reality sits in the middle: a credit card is a financial tool. Like any tool, outcomes depend on how it’s used, the rules attached to it, and the user’s understanding of those rules.

What is a Credit Card?

A credit card is a payment card issued by a bank or financial institution that allows you to borrow money to pay for goods or services, with the agreement that you’ll repay the amount later.

Instead of pulling money directly from your checking account (as a debit card does), a credit card creates a temporary loan each time you use it.

Key elements involved:

- Issuer: The bank or institution that provides the card and sets its terms

- Credit limit: The maximum amount you’re allowed to borrow at one time

- Balance: The amount you currently owe

- Billing cycle: The monthly period during which charges are tracked

- Payment due date: The deadline to pay at least the required minimum

If you pay your statement balance in full by the due date, you generally avoid interest. If you don’t, interest begins accruing on the unpaid amount.

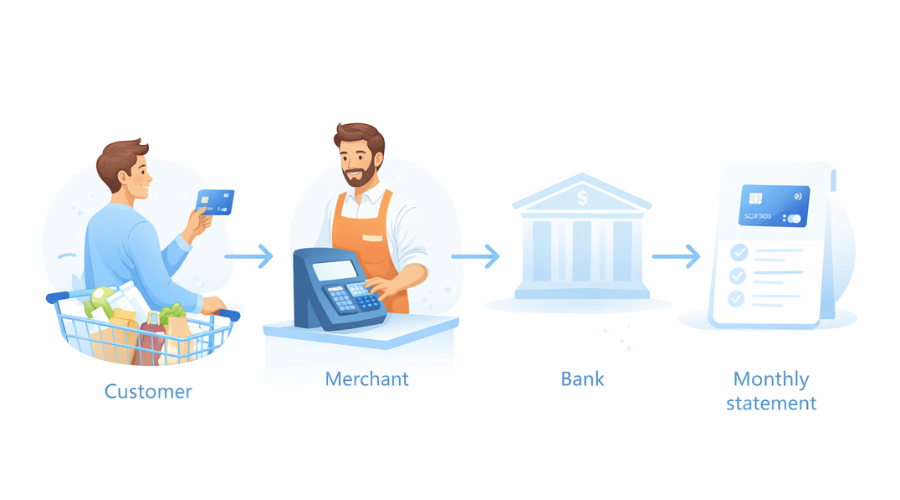

How a credit card works in the United States

Although individual card terms vary, the core process is the same across U.S. issuers.

1. You make a purchase

When you swipe, tap, or enter your card details online, the card issuer:

- Verifies your account is active

- Confirms the charge doesn’t exceed your credit limit

- Temporarily approves the transaction

The merchant gets paid, and the amount is added to your card balance.

2. The billing cycle closes

At the end of each billing cycle (usually about 30 days), the issuer creates a statement showing:

- Total purchases and credits

- Your statement balance

- The minimum payment required

- The payment due date

3. You repay what you borrowed

You have options:

- Pay the full statement balance → typically no interest charged

- Pay part of the balance → interest applies to the remaining amount

- Pay only the minimum → interest accrues and the debt lasts longer

Interest rates on U.S. credit cards are usually high compared to other loans, especially for balances carried month to month.

Who credit cards are designed for—and who should be cautious

Credit cards are commonly used by:

- People who want flexibility in monthly cash flow

- Those building or maintaining a U.S. credit history

- Consumers who value fraud protections and dispute rights

- Households that pay balances in full and avoid interest

Extra caution is needed if:

- You already carry high-interest debt

- Your income is unpredictable and payments may be late

- You’re prone to overspending with borrowed money

A credit card itself isn’t good or bad—but it amplifies habits. Strong repayment habits are rewarded; weak ones become expensive quickly.

What a credit card is not

Clearing up common misunderstandings helps prevent costly mistakes.

- Not extra income: Every dollar spent must be repaid

- Not the same as a debit card: Funds don’t come directly from your bank account

- Not a long-term loan: Carrying balances long-term is usually costly

- Not guaranteed approval: Issuers evaluate credit history and risk

Understanding these limits is essential before using a card regularly.

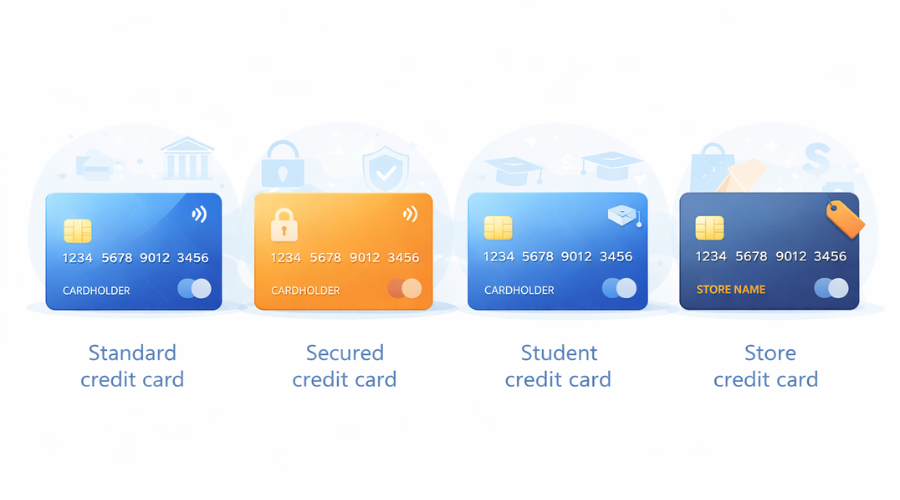

Common types of credit cards in the U.S.

Credit cards aren’t one-size-fits-all. In the United States, issuers design different card types to match how people spend, borrow, and manage credit. Understanding these categories helps avoid mismatches between a card’s structure and a person’s financial behavior.

Standard (unsecured) credit cards

These are the most common cards.

- No upfront deposit required

- Credit limits are based on income, credit history, and risk

- Typically include interest charges if balances are carried

Most everyday consumer credit cards fall into this category.

Secured credit cards

Designed mainly for credit building or rebuilding.

- Require a refundable cash deposit (often equal to the credit limit)

- Used by people with limited or damaged credit history

- Activity is usually reported to the major U.S. credit bureaus

Despite the deposit, they function like regular credit cards in daily use.

Student credit cards

Targeted at college students with limited credit history.

- Lower credit limits

- Fewer qualification requirements

- Often designed to help establish initial credit records

Approval standards and terms still vary by issuer.

Charge cards

Less common, but still important to understand.

- Typically require the full balance to be paid each month

- No preset spending limit (though internal limits still exist)

- Late payments can trigger immediate penalties

Unlike traditional credit cards, carrying a balance is usually not allowed.

Store and retail credit cards

Issued by or for specific retailers.

- Usable only at certain stores or brands

- Often come with higher interest rates

- Sometimes easier to qualify for than general-purpose cards

They can limit flexibility and increase borrowing costs if balances are carried.

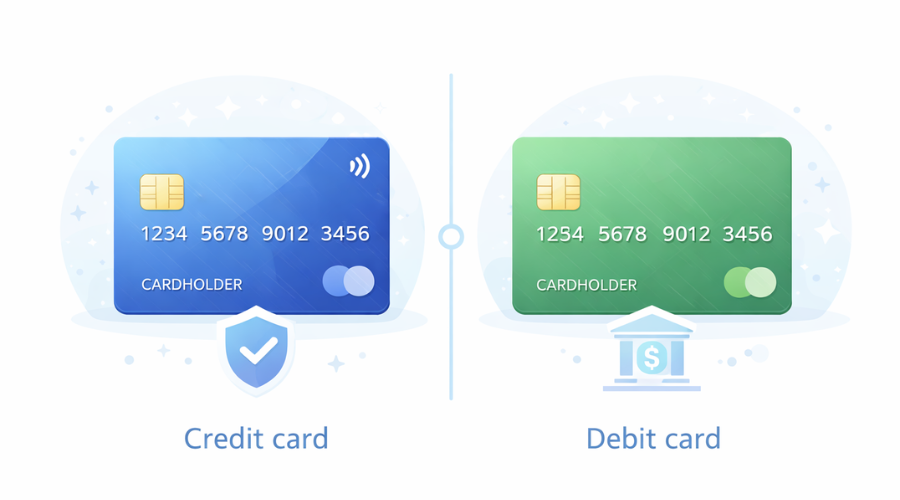

Credit cards vs. debit cards (important distinction)

Many payment experiences look identical at checkout, but the financial mechanics are very different.

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of funds | Borrowed money | Your bank account |

| Impact on credit | Yes (reported) | No |

| Fraud protection | Strong federal protections | Varies, often more limited |

| Interest charges | Possible | None |

| Spending limit | Credit limit | Account balance |

Because credit cards don’t pull money directly from your account, they often provide stronger consumer protections for disputes and fraud.

Advantages of using a credit card

When used responsibly, credit cards can provide practical benefits beyond convenience.

Financial flexibility

Credit cards allow short-term borrowing without applying for a loan each time an expense arises. This can help smooth timing gaps between expenses and income.

Fraud and dispute protections

Under U.S. federal law, credit card users typically have:

- Limited liability for unauthorized charges

- The right to dispute billing errors

- Protection when goods aren’t delivered as agreed

These protections are stronger and more consistent than those for debit cards.

Credit history building

Regular, on-time payments can help establish a positive payment record, which affects future borrowing costs.

Record keeping and budgeting

Monthly statements provide detailed spending records that can help track expenses and identify patterns.

Disadvantages and risks to understand

Credit cards can create long-term problems when misunderstood or misused.

High interest costs

U.S. credit card interest rates are often significantly higher than:

- Auto loans

- Student loans

- Mortgages

Carrying balances for long periods can dramatically increase the total cost of purchases.

Minimum payment trap

Paying only the minimum:

- Keeps accounts in good standing short-term

- Extends repayment for years

- Increases total interest paid

Many cardholders underestimate how long repayment actually takes.

Overspending risk

Because payment is delayed, it’s easier to spend more than intended—especially for discretionary purchases.

Credit damage from late payments

Late or missed payments can:

- Trigger fees

- Increase interest rates

- Negatively affect credit reports

Payment history is one of the most influential factors in U.S. credit scoring systems.

Common myths vs. facts about credit cards

| Myth | Reality |

|---|---|

| Carrying a balance builds credit | False — on-time payments matter, not interest paid |

| Credit cards are only for emergencies | False — they’re everyday tools with risks |

| Closing cards always helps credit | False — it can sometimes lower available credit |

| Debit cards are always safer | False — credit cards often offer better fraud protection |

Misunderstanding these points is one of the most common sources of financial frustration.

Key terms every U.S. credit card user must understand

Many credit card problems don’t come from bad intentions—they come from not fully understanding the terms. These concepts apply to nearly all U.S. credit cards, regardless of issuer.

Credit limit

The credit limit is the maximum amount you can borrow on the card at any given time.

It’s set by the issuer based on factors like income, credit history, and existing debt.

- Spending near the limit can increase financial stress

- Maxing out cards may negatively affect credit profiles

The limit can change over time, up or down, depending on account activity and risk reviews.

Annual Percentage Rate (APR)

The APR represents the yearly cost of borrowing if you carry a balance.

Important points:

- Most cards have variable APRs that can change with market rates

- Different APRs may apply to purchases, balance transfers, and cash advances

- Interest usually applies only if you don’t pay the full statement balance

APR is one of the most expensive features of credit cards when balances are carried.

Grace period

The grace period is the time between the statement closing date and the payment due date.

- If you pay the full statement balance within this window, you usually avoid interest

- Grace periods often disappear if a balance is carried month to month

Not all transactions (such as cash advances) receive a grace period.

Minimum payment

The minimum payment is the smallest amount required to keep the account current.

- Paying only the minimum avoids late fees

- It does not prevent interest from accumulating

- It extends repayment and increases total cost

Minimum payments are designed to protect the lender—not to help you get out of debt quickly.

Fees

Common U.S. credit card fees may include:

- Annual fees

- Late payment fees

- Returned payment fees

- Cash advance fees

- Foreign transaction fees

Not every card charges all of these, but understanding which apply matters.

How credit cards affect your credit profile

Credit cards play a central role in U.S. credit reporting systems.

Payment history

On-time payments help build a positive record.

Late payments—especially those 30 days or more past due—can cause lasting harm.

Credit card payment behavior directly affects your overall credit profile, which is explained in more detail in our guide on What Is a Credit Score.

Credit utilization

Credit utilization refers to how much of your available credit you’re using.

Example:

- Credit limit: $5,000

- Balance: $2,500

- Utilization: 50%

Lower utilization generally reflects lower risk.

Account age and mix

- Older accounts can strengthen credit profiles over time

- Credit cards contribute to credit mix alongside loans

Closing accounts without understanding the impact can sometimes backfire.

Real-life U.S. example: two different outcomes

Example 1: Paying in full

- Monthly spending: $1,200

- Statement balance paid in full each month

- Interest paid: $0

- Result: clean payment history, predictable costs

Example 2: Carrying a balance

- Monthly spending: $1,200

- Pays only the minimum

- Balance rolls over

- Interest compounds monthly

- Result: higher total cost, slower progress, added stress

The same card produces very different outcomes based on behavior.

Pros and cons of credit cards (summary)

| Pros | Cons |

|---|---|

| Short-term borrowing flexibility | High interest if balances are carried |

| Strong consumer protections | Easy to overspend |

| Builds credit history | Fees and penalties possible |

| Useful expense tracking | Credit damage from late payments |

Credit cards reward discipline and punish neglect.

Common beginner mistakes to avoid

- Treating credit limits as spending targets

- Paying late or forgetting due dates

- Assuming interest only applies yearly (it accrues more often)

- Using cards for long-term borrowing

- Ignoring statements and terms

Most of these mistakes are preventable with basic awareness.

U.S. laws and consumer protections that apply to credit cards

Credit cards in the United States are not governed only by bank policies. Several federal consumer protection laws shape how cards work and what rights cardholders have.

Truth in Lending Act (TILA)

This law requires issuers to clearly disclose:

- Interest rates (APR)

- Fees

- Billing methods

- Payment calculations

It exists so consumers can understand the true cost of borrowing before using credit.

Credit CARD Act of 2009

Often called the CARD Act, this law introduced major protections, including:

- Limits on sudden interest rate increases

- Restrictions on certain fees

- Clearer monthly statements

- Extra protections for consumers under 21

It also requires issuers to show how long repayment takes if only minimum payments are made.

Fair Credit Billing Act (FCBA)

This law gives cardholders the right to:

- Dispute billing errors

- Challenge unauthorized charges

- Withhold payment during an investigation

There are strict timelines and procedures, which is why reviewing statements promptly matters.

Fraud liability limits

In most cases:

- Maximum liability for unauthorized credit card charges is limited

- Many issuers go further and offer zero-liability policies

This is one reason credit cards are often safer than debit cards for online and travel use.

When using a credit card makes sense—and when it doesn’t

Credit cards work best in specific situations and poorly in others.

Situations where credit cards often make sense

- Regular expenses you can pay off in full each month

- Purchases where fraud protection matters

- Building or maintaining a credit record

- Short-term cash flow timing gaps

Situations where credit cards may cause harm

- Covering ongoing income shortfalls

- Long-term borrowing for necessities

- Spending beyond a realistic budget

- Replacing emergency savings

Using a credit card to delay financial problems often makes them worse, not better.

Step-by-step: responsible credit card use in practice

This isn’t about optimization or rewards—it’s about financial safety and control.

- Charge only what you can repay

Treat the card like delayed cash, not extra money. - Track spending during the billing cycle

Don’t wait until the statement arrives to know your balance. - Pay the statement balance in full

This avoids interest and keeps costs predictable. - Pay on time, every time

Set reminders or autopay to avoid accidental late payments. - Review every statement

Look for errors, unfamiliar charges, and fee changes. - Avoid cash advances

They usually come with immediate interest and extra fees.

These habits matter more than card features or limits.

Credit cards and long-term financial impact

Over time, credit card behavior influences:

- Loan approvals and interest rates

- Insurance pricing in some states

- Rental and housing applications

- Financial stress levels

Credit cards don’t just affect monthly budgets—they affect future options.

A single late payment can remain on credit reports for years, while consistent on-time payments gradually build trust with lenders.

Final perspective before moving on

A credit card is neither a shortcut nor a solution.

It’s a contracted borrowing tool with clear rules, protections, and consequences.

When understood and used carefully, it can support financial stability.

When misunderstood, it quietly becomes one of the most expensive forms of debt in American households.

Frequently Asked Questions About Credit Cards (U.S.)

What happens if I don’t pay my credit card bill in full?

If you don’t pay the full statement balance by the due date, interest is charged on the remaining amount. Over time, this increases the total cost of your purchases. Paying less than the full balance can also remove the grace period for future charges until the balance is fully repaid.

Is it bad to use a credit card every month?

No. Using a credit card regularly is not harmful by itself. What matters is how it’s used. Regular use combined with on-time, full payments can help maintain a positive payment history. Problems arise when balances are carried or payments are missed.

Does paying interest help build credit?

No. Interest payments do not improve credit scores. Credit systems focus on on-time payments, amounts owed, and account history—not on how much interest you pay. Carrying a balance only increases cost, not credit benefits.

What is the difference between statement balance and current balance?

Statement balance: The amount owed at the end of the billing cycle

Current balance: The real-time total, including recent charges

Paying the statement balance by the due date usually avoids interest on those charges.

Can credit cards hurt my credit even if I pay on time?

Yes, in some cases. High credit utilization—using a large portion of your available credit—can negatively affect credit profiles, even if payments are on time. This impact is often temporary and changes as balances change.

What happens if I miss a credit card payment?

Missing a payment can result in:

Late fees

Increased interest rates

Negative reporting to credit bureaus (if sufficiently late)

Payment history is one of the most influential factors in U.S. credit scoring systems.

Are credit cards safer than debit cards?

Often, yes. Credit cards typically offer stronger protections for unauthorized charges and disputes. Because your bank account isn’t directly accessed, resolving fraud can be less disruptive.

Do credit cards have tax implications?

Generally, normal credit card purchases and interest payments are not tax-deductible for personal use. Some business-related expenses may be treated differently under IRS rules. Tax treatment depends on use and individual circumstances.

Should beginners avoid credit cards altogether?

Not necessarily. For many people, a credit card is one of the easiest ways to establish a U.S. credit history. The key is starting with clear rules, small balances, and consistent full payments.

How many credit cards should one person have?

There is no universal number. The appropriate number depends on:

Income stability

Spending habits

Ability to manage payments

More cards mean more responsibility. Fewer cards mean fewer moving parts—but also fewer buffers.

Can a credit card replace an emergency fund?

No. Credit cards can help temporarily, but relying on them for emergencies often leads to long-term high-interest debt. Emergency savings provide flexibility without ongoing borrowing costs.

Disclaimer

This content is provided for educational and informational purposes only.

It is not financial, legal, or tax advice.

Credit card rules, interest rates, fees, and consumer protections can vary by issuer, state, and individual financial situation. Before making personal financial decisions, you should consult a qualified financial professional, credit counselor, tax advisor, or legal expert who understands your specific circumstances.

6 thoughts on “What Is a Credit Card? How Credit Cards Work in the U.S. (Complete Guide)”