Life insurance is one of the most misunderstood financial products in the United States. Many people hear about it through employers, ads, or agents—but few truly understand how it works, who actually needs it, and how much coverage is enough.

This guide explains life insurance in clear, plain English, focusing on how it works in the U.S., the main policy types, costs, payouts, and common mistakes—so you can make informed decisions without confusion.

Key Takeaways

- Life insurance pays money to your chosen beneficiaries if you die while the policy is active.

- In the U.S., policies are regulated at the state level, with federal oversight on certain consumer protections and tax rules.

- The two main categories are term life (temporary coverage) and permanent life (lifelong coverage with a savings component).

- Premiums, coverage amount, and eligibility depend on age, health, policy type, and insurer rules.

- Life insurance is designed to protect people who depend on your income, not to serve as a short-term investment or emergency fund.

Why Life Insurance Matters in Real American Life

Many Americans first think about life insurance after a major life event—getting married, having a child, buying a home, or starting a business. The confusion usually starts right away. People mix it up with health insurance, assume it’s only for older adults, or believe it’s automatically provided by an employer.

At its core, life insurance is about income protection. If your paycheck helps pay rent or a mortgage, covers child care, or supports a spouse or parent, your death would create a financial gap. Life insurance exists to help close that gap. Understanding how it works in the U.S. helps people avoid overpaying, under-insuring, or buying a policy that doesn’t match their real needs.

What Is Life Insurance?

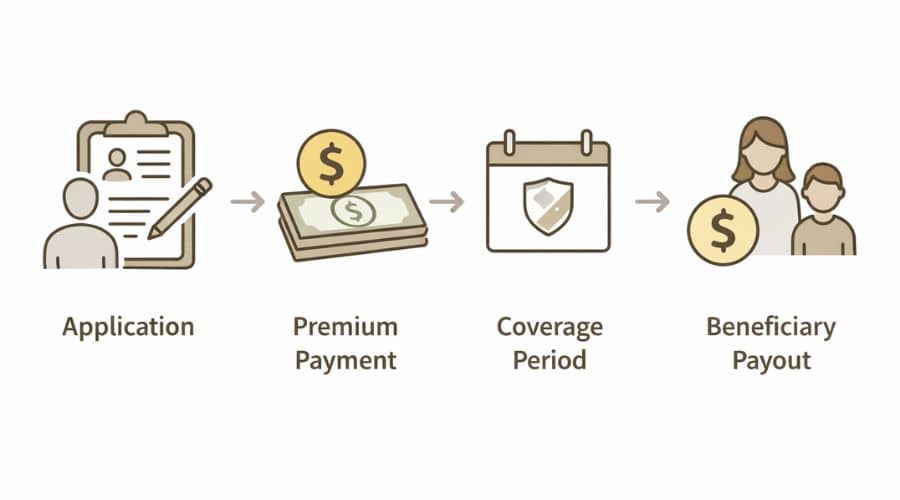

Life insurance is a contract between you and an insurance company.

You agree to pay regular premiums. In return, the insurer agrees to pay a death benefit—a lump sum of money—to your named beneficiaries if you die while the policy is in force.

Key terms you’ll see throughout this article:

- Policyholder: The person who owns the policy (usually you).

- Insured: The person whose life is covered (often the same as the policyholder).

- Premium: The amount you pay to keep the policy active.

- Beneficiary: The person or entity that receives the payout.

- Death benefit: The money paid out after the insured’s death.

Life insurance pays only when the insured person dies and the policy terms are met—not for illness, job loss, or retirement. It pays only when the insured person dies and the policy terms are met.

How Life Insurance Works in the United States

The Basic Mechanics

- You apply for a policy with an insurance company licensed in your state.

- The insurer evaluates risk, often using age, health history, lifestyle, and sometimes a medical exam.

- You receive an offer showing the premium, coverage amount, and policy terms.

- You pay premiums (monthly, quarterly, or annually).

- If you die while the policy is active, the insurer pays the death benefit to your beneficiaries.

Regulation and Consumer Protection

Life insurance in the U.S. is primarily regulated by state insurance departments, which set rules for policy approval, solvency, and claims handling. At the federal level, consumer protection and financial oversight are influenced by agencies such as the Consumer Financial Protection Bureau, while tax treatment is governed by the Internal Revenue Service. Certain investment-related products fall under guidance from the Securities and Exchange Commission.

Because rules can vary by state and insurer, policy details like grace periods, contestability rules, and beneficiary rights may differ.

What the Policy Covers—and What It Doesn’t

Most life insurance policies cover death from natural causes and accidents. Common exclusions or limitations may include:

- Suicide clauses during the first two policy years (varies by state and policy).

- Material misrepresentation, such as lying on the application.

- Lapsed policies due to unpaid premiums.

The Two Main Types of Life Insurance (High-Level Overview)

Before diving deeper later, it helps to understand the broad categories:

Term Life Insurance

- Covers you for a specific period (commonly 10, 20, or 30 years).

- Pays out only if death occurs during that term.

- Typically the least expensive option.

Permanent Life Insurance

- Designed to last your entire life, as long as premiums are paid.

- Includes a cash value component that grows over time.

- Significantly more expensive and more complex than term life.

We’ll break these down in detail—including costs, use cases, and risks—in the next sections.

Term Life Insurance: How It Works and When It Makes Sense

Term life insurance is the simplest and most common form of life insurance in the U.S. For many households, it’s also the most practical.

What Term Life Insurance Is

Term life insurance provides coverage for a fixed period of time, called the term. Common terms are 10, 15, 20, or 30 years. If you die during that period, your beneficiaries receive the death benefit. If you outlive the term, the policy expires and no money is paid.

There is no savings or investment component. You are paying strictly for protection.

How Term Life Insurance Works Step by Step

- Choose a term length

Most people match the term to a major financial responsibility, such as:- Years until children are financially independent

- Remaining mortgage duration

- Expected working years until retirement

- Select a coverage amount

Coverage is usually based on:- Income replacement needs

- Outstanding debts

- Future expenses (education, housing, caregiving)

- Apply and undergo underwriting

Depending on the policy:- Some require a medical exam

- Others use health questionnaires and data checks

- Pay fixed premiums

Premiums typically stay level for the entire term, which makes budgeting predictable. - Policy either pays out or expires

- Death during term → beneficiaries receive payout

- Survival past term → coverage ends

Typical Term Lengths and Common Use Cases

| Term Length | Common Situations |

|---|---|

| 10 years | Short-term income gap, temporary debt |

| 20 years | Raising children, paying down a mortgage |

| 30 years | Young families with long-term obligations |

Pros and Cons of Term Life Insurance

| Pros | Cons |

|---|---|

| Lower premiums compared to permanent life | No payout if you outlive the term |

| Simple and easy to understand | Coverage eventually ends |

| Predictable, fixed costs | Renewal can be expensive or unavailable |

| Flexible coverage amounts | No cash value |

Common Term Life Policy Features

Level Term

- Premium and death benefit stay the same for the full term.

- Most popular option in the U.S.

Convertible Term

- Allows conversion to a permanent policy without new medical underwriting.

- Conversion deadlines and rules vary by insurer.

Renewable Term

- Allows renewal after the term ends.

- Premiums usually increase sharply with age.

Who Term Life Insurance Is Best For

Term life insurance is generally well-suited for people who:

- Have financial dependents

- Are working and earning income

- Need maximum coverage at the lowest cost

- Want straightforward protection, not complexity

It is especially common among:

- Young families

- First-time homeowners

- Single-income households

- Small business owners with temporary obligations

Common Mistakes With Term Life Insurance

- Choosing a term that’s too short, leaving coverage gaps later

- Underestimating coverage needs, especially future expenses

- Letting policies lapse unintentionally

- Assuming employer-provided life insurance is sufficient

Employer life insurance is often limited (for example, 1–2× salary) and usually ends when employment ends.

What Happens When a Term Policy Ends

When the term expires:

- Coverage stops

- No refund is issued

- Renewal (if allowed) is usually much more expensive

Some people:

- Replace term coverage with a new policy

- Convert to permanent insurance

- Decide coverage is no longer needed

This decision depends on age, health, and financial responsibilities at that time.

Permanent Life Insurance: How It Works and Why It’s More Complex

Permanent life insurance is designed to last your entire lifetime, not just a fixed number of years. It combines life insurance protection with a long-term savings component, which is why it’s often misunderstood—and sometimes misused.

What Permanent Life Insurance Is

Permanent life insurance provides lifelong coverage as long as required premiums are paid. Unlike term life insurance, it includes a cash value account that grows over time.

The policy has two core parts:

- Death benefit: Paid to beneficiaries when you die

- Cash value: A portion of premiums set aside and grown inside the policy

Permanent policies are significantly more expensive than term life, especially in the early years, and require long-term commitment.

How Permanent Life Insurance Works in Practice

- You pay higher premiums than term life

- Part of each premium goes toward insurance costs

- Part goes into cash value, which grows based on the policy type

- Cash value grows tax-deferred under current U.S. tax rules

- Coverage remains active for life, if policy requirements are met

If premiums stop or cash value is mismanaged, the policy can lapse—even after many years.

Main Types of Permanent Life Insurance

Whole Life Insurance

- Fixed premiums

- Guaranteed death benefit

- Guaranteed minimum cash value growth

- Often pays dividends (not guaranteed)

Whole life is the most predictable permanent policy, but also one of the most expensive.

Universal Life Insurance

- Flexible premiums

- Adjustable death benefit

- Cash value growth tied to interest rates or insurer formulas

This flexibility comes with risk. Poor performance or underfunding can cause policy failure.

Variable Life Insurance

- Cash value invested in sub-accounts similar to mutual funds

- Growth depends on market performance

- Subject to market risk

Because of its investment component, variable life is overseen in part by the Securities and Exchange Commission.

Cash Value: What It Is—and What It Isn’t

Cash value is not a bank account.

It grows slowly in the early years and is reduced by:

- Insurance costs

- Policy fees

- Rider charges

You can access cash value by:

- Policy loans (borrowed amounts accrue interest)

- Withdrawals (may reduce death benefit)

Unpaid loans can reduce or eliminate the death benefit.

Tax Treatment in the U.S.

Under current federal tax rules:

- Cash value growth is tax-deferred

- Death benefits are generally income-tax-free to beneficiaries

- Withdrawals and loans can trigger taxes if not structured properly

Tax treatment is governed by the Internal Revenue Service, and rules can change over time.

Pros and Cons of Permanent Life Insurance

| Pros | Cons |

|---|---|

| Lifelong coverage | Much higher premiums |

| Tax-deferred cash value growth | Complex structure |

| Can support estate planning | Slow early cash value growth |

| Predictable for long-term needs | Risk of lapse if mismanaged |

Who Permanent Life Insurance May Be Appropriate For

Permanent life insurance is sometimes used by people who:

- Have long-term dependents (such as a disabled child)

- Need estate liquidity for taxes or business succession

- Have already maxed out other tax-advantaged savings

- Want guaranteed lifelong coverage

It is not typically appropriate for people seeking:

- Low-cost protection

- Short- or medium-term coverage

- Simple financial products

Common Mistakes With Permanent Life Insurance

- Buying it without a clear long-term purpose

- Underfunding the policy

- Treating it as a primary investment

- Not understanding ongoing costs and risks

Permanent life insurance requires active management and long-term commitment.

How Life Insurance Payouts Work in the U.S.

Understanding how payouts actually happen is critical. Many problems arise not because a policy didn’t exist, but because beneficiaries didn’t know what to do—or because the policy wasn’t structured correctly.

Knowing these steps in advance can prevent delays, confusion, and financial stress for surviving family members.

What Happens When the Insured Person Dies

When the insured person dies, beneficiaries must:

- Notify the insurance company

- Submit a claim along with a certified death certificate

- Provide identification and claim forms as required by the insurer

Once approved, the insurer pays the death benefit according to the policy terms.

Most insurers process straightforward claims within a few weeks, though timelines vary by company and state.

How Beneficiaries Receive the Money

Beneficiaries typically have several payout options:

Lump-Sum Payment

- Entire death benefit paid at once

- Most common choice

- Generally income-tax-free under federal law

Installment Payments

- Paid over time (monthly or annually)

- Interest earned may be taxable

Retained Asset Accounts

- Funds held by insurer in an interest-bearing account

- Beneficiary can withdraw funds as needed

The availability of these options depends on the insurer and policy contract.

Are Life Insurance Payouts Taxable?

Under current U.S. federal law:

- Death benefits are usually not subject to federal income tax

- Interest earned after the payout may be taxable

- Estate taxes may apply for very large estates

Tax rules are governed by the Internal Revenue Service and can change over time.

State taxes may also apply depending on where the insured lived.

When a Claim Can Be Delayed or Denied

Claims are rarely denied outright, but delays can occur due to:

- Incomplete documentation

- Policy lapse due to unpaid premiums

- Death during the contestability period (usually first two years)

- Material misstatements on the application

During the contestability period, insurers may review medical records and application details closely.

Beneficiary Designations: A Critical Detail

Life insurance payouts are governed by beneficiary designations, not wills.

Important rules:

- Named beneficiaries receive the money directly

- Proceeds generally avoid probate

- Outdated beneficiaries can cause unintended outcomes

Life events such as marriage, divorce, births, and deaths should trigger a beneficiary review.

Minor Children as Beneficiaries

Naming a minor directly can create legal complications. Because minors cannot legally control large sums of money, special planning is usually required.

- Insurers may require a court-appointed guardian

- Funds may be held until adulthood

Many people use:

- Trusts

- Custodial arrangements allowed under state law

Rules vary by state.

Common Payout Mistakes to Avoid

- Never updating beneficiaries

- Assuming employer policies cover everything

- Not telling beneficiaries where policies are stored

- Choosing payout options without understanding tax implications

Who Needs Life Insurance—and Who May Not

Life insurance is not automatically necessary for every adult. Its value depends on whether someone else would face a financial loss if you died. The key question is whether your death would create a financial hardship for someone else.

People Who Commonly Need Life Insurance

Life insurance is most relevant when your death would create a financial gap for others.

Parents and Guardians

If children depend on your income or caregiving:

- Life insurance can replace lost income

- It can help cover housing, education, and daily living costs

- It can support child care or guardianship arrangements

Both working and non-working parents are often insured, because caregiving has real economic value.

Married or Partnered Households

If one partner relies on the other’s income or benefits:

- Life insurance helps the surviving partner maintain stability

- It can help pay off shared debts, including mortgages and loans

This applies even when both partners work, especially if one income is significantly higher.

Homeowners With a Mortgage

Life insurance can:

- Help pay off or service a mortgage

- Prevent a forced home sale after a death

Mortgage balance and remaining term often guide coverage decisions.

Single-Income or Uneven-Income Families

When one income supports most household expenses:

- Life insurance helps preserve the household’s standard of living

- It can buy time for financial adjustment

Business Owners

Life insurance may be used to:

- Fund buy-sell agreements

- Cover key-person risk

- Support business continuity

Business-related uses are highly structured and vary by state and insurer.

People Who May Not Need Life Insurance

Life insurance may be unnecessary or minimal in some cases.

Single Adults With No Dependents

If no one relies on your income and you have:

- Minimal debt

- Enough savings to cover final expenses

Life insurance may not be a priority.

Retirees With Adequate Assets

If retirement income, savings, and pensions are sufficient for survivors:

- Additional life insurance may offer limited benefit

- Existing permanent policies may still play a role in estate planning

People With Sufficient Employer or Asset Coverage

Some households already have:

- Substantial assets

- Pensions or survivor benefits

- Existing policies that fully cover needs

In these cases, additional coverage may be redundant.

A Common Misunderstanding

Life insurance is not about you.

It is about the people who would be financially affected by your absence.

That’s why two people with the same income may need very different coverage amounts—or none at all.

Employer-Provided Life Insurance: Helpful but Limited

Many U.S. employers offer group life insurance, often:

- 1× to 2× annual salary

- Coverage tied to employment

- Limited portability

For households with dependents, employer coverage alone is often not enough and may disappear if the job ends.

How Much Life Insurance Coverage Do Americans Usually Need?

There is no single “correct” amount of life insurance. To understand how much coverage is actually right for your situation, you can read our detailed guide on how much life insurance coverage you need. The right coverage depends on who relies on your income, for how long, and for what purpose. In the U.S., coverage decisions are usually driven by practical math, not rules of thumb.

The Core Question to Ask

If you died tomorrow, how much money would your household need to stay financially stable?

That usually includes:

- Replacing lost income

- Paying off major debts

- Covering future obligations

- Allowing time for adjustment

Common Coverage Components (U.S.-Based)

Income Replacement

Many households aim to replace:

- 5–15 years of income, depending on age and family situation

This helps survivors pay for:

- Housing

- Food and utilities

- Health insurance

- Childcare or elder care

There is no federal standard. This is a planning convention, not a legal rule.

Outstanding Debts

Coverage often includes:

- Mortgage balance

- Auto loans

- Personal loans

- Private student loans (federal student loans are usually discharged at death)

Credit card debt may or may not transfer, depending on account structure and state law.

Future Expenses

Depending on the household, this may include:

- College or vocational education costs

- Childcare expenses

- Medical or caregiving needs

- Final expenses (funeral and burial)

A Simple Coverage Framework (Not a Formula)

Many financial educators use this structure to estimate needs:

| Category | Typical Consideration |

|---|---|

| Income | Years of income needed |

| Debts | Total outstanding balances |

| Future costs | Education, care, major goals |

| Existing assets | Savings, investments, benefits |

Existing assets and survivor benefits can reduce the amount of insurance needed.

Why “10× Income” Can Be Misleading

You’ll often hear that life insurance should equal 10 times income. This can be:

- Too high for some households

- Too low for others

It ignores:

- Debt levels

- Childcare costs

- Existing savings

- Survivor benefits

- Regional cost differences

Coverage should reflect real expenses, not a single multiplier.

How Much Does Life Insurance Cost in the U.S.?

Life insurance pricing is based on risk. Two people of the same age can pay very different premiums.

Main Factors That Affect Premiums

- Age (younger usually costs less)

- Health history

- Smoking status

- Policy type (term vs permanent)

- Coverage amount

- Term length (for term life)

Insurers use underwriting guidelines approved at the state level.

Typical Cost Differences: Term vs Permanent

| Feature | Term Life | Permanent Life |

|---|---|---|

| Monthly cost | Lower | Much higher |

| Duration | Fixed term | Lifetime |

| Cash value | No | Yes |

| Complexity | Simple | Complex |

For many families, term life provides far more coverage per dollar.

Medical Exams and No-Exam Policies

- Traditional policies often require a medical exam

- No-exam policies rely on health data and algorithms

- No-exam coverage is usually more expensive for the same benefit

Approval rules vary by insurer and state.

Why Buying Earlier Often Costs Less

Premiums are usually locked in at purchase for term life.

- Buying younger can mean decades of lower costs

- Health changes later can increase premiums or limit eligibility

This does not mean everyone should buy early—only when coverage is actually needed.

Common Cost Mistakes

- Overbuying permanent insurance when term would suffice

- Choosing premiums that strain monthly cash flow

- Letting policies lapse due to affordability issues

A policy that cannot be maintained long-term provides no protection.

Risks, Downsides, and Common Life Insurance Mistakes

Life insurance is straightforward in concept, but mistakes can be costly and hard to reverse. Most problems come from misunderstanding how policies work over time.

Letting a Policy Lapse

A policy lapses when premiums are not paid within the grace period.

- Coverage ends

- No payout is made

- Reinstatement may be impossible or expensive

This is one of the most common and preventable failures.

Buying the Wrong Type of Policy

Common mismatches include:

- Buying permanent life when short-term protection was needed

- Choosing a term that ends before major obligations do

- Relying solely on employer-provided coverage

The issue is usually misalignment, not the product itself.

Underinsuring

People often underestimate:

- Childcare and caregiving costs

- Healthcare and insurance costs for survivors

- How long income replacement is actually needed

Underinsurance can leave families financially exposed even with a policy in place.

Overcomplicating Coverage

Complex policies with riders, loans, and moving parts:

- Require ongoing attention

- Increase lapse risk

- Are often misunderstood by policyholders

Simplicity reduces long-term failure risk.

Not Reviewing Policies Over Time

Life insurance should be reviewed after:

- Marriage or divorce

- Birth or adoption of a child

- Buying or selling a home

- Major income changes

Outdated coverage and beneficiaries are a frequent source of problems.

Life Insurance Myths vs. Facts

| Myth | Fact |

|---|---|

| Life insurance is only for older people | Many younger families benefit most |

| Employer life insurance is enough | Often limited and temporary |

| Stay-at-home parents don’t need coverage | Caregiving has real economic value |

| Life insurance is an investment | Its primary role is protection |

| Payouts are always taxed | Death benefits are usually income-tax-free |

How Life Insurance Affects Long-Term Finances

Life insurance is not about growing wealth. It’s about protecting financial stability.

Properly structured life insurance can:

- Prevent debt accumulation after a death

- Reduce the need to sell assets under pressure

- Protect credit and housing stability for survivors

Poorly chosen or mismanaged policies can:

- Drain cash flow

- Create false expectations

- Provide little real protection

The long-term impact depends more on fit and maintenance than on policy size.

Frequently Asked Questions (FAQ)

-

Is life insurance required by law in the U.S.?

No. Life insurance is not legally required for individuals. Some lenders may require it indirectly for business or secured lending situations, but there is no federal mandate.

-

Can I have more than one life insurance policy?

Yes. Many people carry multiple policies to cover different needs, such as one policy for a mortgage and another for income replacement.

-

What happens if I stop paying premiums?

After the grace period, the policy typically lapses and coverage ends. Permanent policies may use cash value to cover premiums temporarily, but this is not guaranteed.

-

Does life insurance cover death from illness?

Yes. Most policies cover death from illness, including chronic and terminal conditions, unless specifically excluded.

-

Can beneficiaries be changed?

Yes. Most policies allow changes at any time unless an irrevocable beneficiary is named. Changes must be submitted to the insurer to be valid.

-

Are life insurance payouts affected by debt?

Life insurance proceeds go directly to beneficiaries and generally are not used to pay the insured’s debts, unless the estate is the beneficiary.

-

Is life insurance taxable at the state level?

Some states may tax interest earned after payout or include proceeds in estate tax calculations. Rules vary by state and estate size.

-

What if I outlive my term life insurance?

The policy expires with no payout. Some policies allow renewal or conversion, usually at a much higher cost.

Final Disclaimer

This content is provided for educational and informational purposes only. It does not constitute legal, tax, or financial advice. Life insurance rules, costs, and suitability vary by individual circumstances, insurer, and state law. Readers should consult a qualified insurance professional, financial advisor, or tax professional before making personal financial decisions.