Understanding how credit scores work can feel surprisingly complicated, even for people who manage their finances responsibly. Many Americans assume that paying their credit card bill on time is the only thing that matters for maintaining a strong credit score. While payment history is extremely important, it is not the only factor that influences how lenders and credit scoring models evaluate your credit behavior.

One of the most influential — and often misunderstood — elements of credit scoring is your credit utilization ratio. This number reflects how much of your available credit you are currently using compared with your total credit limits. Even if you always pay your balances in full and never pay interest, high reported balances can still affect your credit score if a large portion of your available credit appears to be in use.

Credit utilization plays a significant role in widely used scoring systems such as FICO Score and VantageScore, and it can influence everything from loan approvals to the interest rates you are offered. Because of this, understanding how utilization works — and how it is calculated — is an important part of managing your overall credit health.

This guide explains what credit utilization ratio is, how lenders and credit bureaus measure it, why it can affect your credit score so strongly, and what practical steps you can take to keep your utilization within healthy ranges.

Key Takeaways

- Credit utilization ratio is the percentage of your available credit that you’re currently using.

- It is one of the most important factors in U.S. credit scoring models, including FICO and VantageScore.

- Using too much of your limit — even if you pay on time — can lower your credit score.

- For most people, keeping utilization below 30% helps protect their score, and below 10% is often better for top-tier credit profiles.

- Utilization is calculated using your statement balance, not the amount you pay by the due date later in the month.

Why Credit Utilization Causes So Much Confusion

Many Americans do everything else right: they pay on time, avoid collections, and don’t apply for credit often — yet their credit score still drops.

One of the most common reasons is high credit utilization, often without realizing it.

People are often told, “Just pay your bill on time and you’ll be fine.”

But credit scores don’t only look at whether you pay — they also look at how much of your available credit you’re using when your balance is reported. In other words, you can do everything “right” and still see score drops if your reported balances stay high.

That’s where credit utilization comes in, and it affects millions of everyday credit card users, even those who never carry interest.

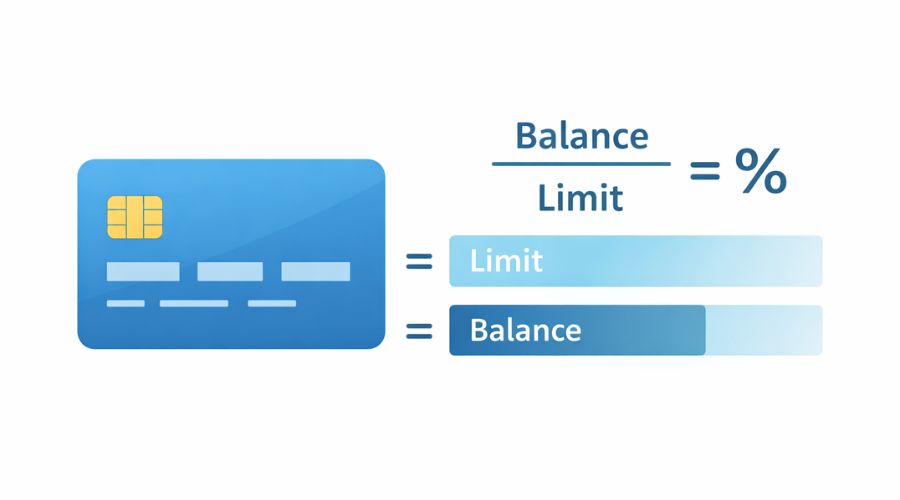

What Is Credit Utilization Ratio?

Your credit utilization ratio is:

How much credit you’re using ÷ how much credit you have available

It’s expressed as a percentage.

Simple Example

- Credit card limit: $5,000

- Current balance reported: $1,500

Calculation:

$1,500 ÷ $5,000 = 30% utilization

That means you’re using 30% of your available credit on that card.

Credit scoring models look at this number because it helps predict how likely someone is to struggle with debt. Higher usage suggests higher risk, even if payments are still on time.

How Credit Utilization Is Calculated in the U.S.

Credit utilization is calculated in two main ways:

1. Per-Card Utilization (Individual Card Level)

Each credit card is evaluated separately.

Example:

| Card | Limit | Balance | Utilization |

|---|---|---|---|

| Card A | $2,000 | $1,000 | 50% |

| Card B | $3,000 | $300 | 10% |

This is why spreading balances across cards — not just lowering total balances — can help protect your score.

Even though your total usage may look reasonable, a single maxed-out or heavily used card can still hurt your score.

2. Overall Utilization (Total Credit Across All Cards)

All card limits and balances are added together.

Using the same example:

- Total limits: $5,000

- Total balances: $1,300

- Overall utilization: 26%

Both per-card and overall utilization matter.

High utilization on one card can still cause a drop even if your total utilization looks fine.

What Counts Toward Credit Utilization (and What Does Not)

Counts Toward Utilization

- Credit card balances

- Store cards (retail credit cards)

- Lines of credit tied to cards

Usually Does NOT Count

- Installment loans (auto loans, personal loans, student loans)

- Mortgages

Installment loans affect your credit in other ways, but they are not part of utilization calculations.

When Is Your Balance Actually Measured?

This is one of the most misunderstood parts.

Most lenders report your balance to the credit bureaus once per month, usually:

- On your statement closing date, not your payment due date

That means:

- You can pay your bill in full every month

- But if your statement closes while a high balance is on the card, that high balance is what gets reported

This is why many people make a small payment before the statement date, even if they plan to pay the full balance later.

So even people who never pay interest can still show high utilization on their credit reports.

This is why utilization can change your score month to month, even when nothing else changes.

Why Credit Utilization Matters So Much for Your Credit Score

In both major scoring systems: According to consumer credit education from major U.S. credit bureaus, credit utilization is one of the most influential factors in credit scoring models.

- FICO Score: Utilization is part of the “Amounts Owed” category, which makes up about 30% of the score

- VantageScore: Utilization is also one of the most influential factors

That makes utilization second only to payment history in terms of impact. (If you want to understand how all credit score factors work together, you can also read our full guide on how credit scores are calculated in the U.S.)

High utilization can:

- Lower your score quickly

- Increase perceived risk to lenders

- Affect approvals and interest rates

The good news is that utilization is also one of the fastest things you can improve, because it updates as soon as new balances are reported.

How Much Credit Should You Actually Use?

There is no single official cutoff written into the law or scoring formulas, but long-term credit data from lenders and credit bureaus shows clear patterns.

General Utilization Ranges and Typical Effects

| Utilization Range | Typical Impact |

|---|---|

| 0% | Can be neutral or slightly negative if all cards report zero |

| 1% – 9% | Often best range for top scores |

| 10% – 29% | Generally safe for good credit |

| 30% – 49% | Score may start to drop |

| 50%+ | Often causes noticeable score declines |

| 80% – 100% | High risk category for scoring models |

Important: These are not official rules. They are observed scoring behaviors across millions of U.S. credit files.

Why 0% Utilization Is Not Always Ideal

It sounds logical that using no credit would look best — but scoring models also want to see active, responsible use.

If all cards report $0:

- Some models treat it as no recent activity

- That can slightly limit scoring potential

This is why many people with excellent credit still allow a small balance to report, then pay it off after the statement posts.

Real-Life U.S. Example: Same Spending, Different Scores

Two people both spend $1,000 each month on a credit card with a $5,000 limit.

Person A

- Lets statement close with $1,000 balance

- Utilization: 20%

Person B

- Pays $900 before statement closes

- Statement balance: $100

- Utilization: 2%

Both pay in full.

Neither pays interest.

But Person B is more likely to see higher and more stable credit scores because the reported balance stays low.

Who Should Pay Extra Attention to Utilization

Utilization matters for everyone, but it’s especially important if you:

- Are trying to qualify for a mortgage or auto loan soon

- Have short credit history

- Have lower credit limits

- Are rebuilding credit after past problems

If you are rebuilding, choosing the right type of card also matters. Secured cards and starter cards can behave differently when limits are low.

When limits are low, even small purchases can push utilization high very quickly.

Example:

- $500 limit

- $200 balance

- Utilization = 40%

That can hurt more than someone using $2,000 on a $10,000 limit.

Common Credit Utilization Mistakes That Hurt Scores

❌ “I pay on time, so balance doesn’t matter”

Payment history and utilization are separate.

You can pay perfectly and still hurt your score with high balances.

❌ “I can use up to my limit if I pay it off later”

Credit scores care about reported balances, not what you eventually pay.

❌ “Only total balance matters”

High usage on one card can hurt even if overall usage looks fine.

❌ “Utilization only matters if I carry debt”

Utilization affects scores even when no interest is charged.

At this point, you understand what credit utilization is, how it’s calculated, and why it matters so much.

Who Should Keep Credit Utilization Low — and When Higher Use May Be Okay

Not everyone needs to manage utilization with the same level of precision all the time. The right utilization strategy depends on your credit goals and whether you plan to apply for new credit soon. But in certain situations, even small increases can have outsized effects on approvals and interest rates.

People Who Should Aim for Very Low Utilization (Under 10%)

You should be extra careful if you are:

- Preparing to apply for a mortgage, auto loan, or refinance

- Working to move from fair to good credit

- Recovering from past late payments or collections

- Using secured or starter credit cards with low limits

Low-limit cards make it easier for balances to spike, even with normal spending.

When lenders review applications, they often look at the most recent reported balances, not just long-term averages. Keeping utilization very low before applying can improve how your credit profile looks at that exact moment.

When Higher Utilization Can Happen Without Long-Term Damage

Sometimes higher balances are realistic and unavoidable, such as:

- Emergency expenses before insurance reimburses you

- Large one-time purchases you plan to pay off quickly

- Temporary income disruptions

High utilization can still cause a short-term score drop, but if you reduce balances and the next statement reports lower usage, scores usually recover. Recovery often happens within one reporting cycle once lower balances are reported.

Credit utilization has no long-term memory in scoring models — only the most recently reported balances matter.

That makes utilization different from late payments, which can stay on reports for up to seven years.

Pros and Cons of Using More vs. Less of Your Available Credit

| Using Lower Utilization | Using Higher Utilization |

|---|---|

| Helps protect credit scores | Can reduce score quickly |

| Improves approval odds | May trigger lender risk flags |

| Supports lower interest rates | Can raise future borrowing costs |

| Shows controlled credit behavior | May limit future credit line increases |

| Keeps flexibility for emergencies | Leaves less room if emergencies happen |

Key warning: High utilization does not mean you are doing something wrong financially, but it does increase how risky your profile looks to lenders, even if your income and savings are strong.

How Credit Utilization Affects Real Financial Outcomes

Credit scores are not just numbers. Utilization can influence:

Loan Approvals

Higher utilization can:

- Trigger automated denials

- Lead to requests for additional documentation

- Push borderline applicants below approval thresholds

Interest Rates

Even small score differences can affect:

- Auto loan APRs

- Personal loan rates

- Credit card approvals with better terms

Over time, that can mean thousands of dollars in additional interest on major loans.

Credit Limit Increases

Banks regularly review accounts for:

- Risk management

- Credit line adjustments

High utilization can signal that someone may be:

- Overextended

- More likely to default

That can reduce the chance of limit increases, which then makes utilization harder to manage long-term.

Utilization vs. Debt: Why These Are Not the Same Thing

It’s important to separate:

- Actual financial health

- How credit models interpret your behavior

Someone can:

- Have high income

- Strong savings

- No missed payments

And still show high utilization because:

- They prefer to charge expenses for rewards

- They pay in full later

From a budgeting perspective, this behavior may be responsible, but scoring models only evaluate reported balances, not payment habits later in the month.

Credit scores do not measure wealth or budgeting skill.

They measure statistical risk patterns, and high balances correlate with future payment problems across large populations.

That’s why utilization matters even when it doesn’t reflect real financial stress.

Step-by-Step: How to Keep Utilization Low Without Changing Your Spending

You do not necessarily need to spend less to manage utilization better.

Step 1: Know Your Statement Closing Dates

Check each card’s:

- Statement closing date (not due date)

This is when balances are typically reported.

You can usually find this date on your statement or in your online account details.

Step 2: Pay Part of the Balance Before the Statement Closes

You can:

- Make an early payment

- Reduce the balance that gets reported

- Still pay the rest after the statement posts

Example:

- Balance during month: $1,200

- Pay $1,000 before statement

- Statement reports $200

Utilization stays low even though spending stayed the same.

Step 3: Spread Spending Across Cards (If You Have Multiple)

Instead of putting:

- All expenses on one card

You can:

- Distribute spending so no single card shows high usage

This helps with per-card utilization, not just overall utilization. Many scoring models penalize high usage on individual cards even if total usage is reasonable.

Step 4: Request Credit Limit Increases (When Appropriate)

Higher limits lower utilization without changing spending.

However:

- Some requests trigger hard credit checks

- Policies vary by bank

Some issuers allow limit increase requests without hard inquiries, while others do not.

This step makes the most sense when:

- Your income has increased

- You have several months of on-time payments

Step 5: Avoid Closing Old Cards Without a Plan

Closing a card:

- Reduces total available credit

- Can instantly raise utilization

This can cause sudden score drops even when spending stays the same.

Common Myths About Credit Utilization (and the Facts)

Myth: You should always carry a balance to build credit

Fact:

Carrying a balance and paying interest does not improve scores.

What matters is reported usage and on-time payments, not interest paid.

Myth: Using your full limit proves you can handle credit

Fact:

Scoring models interpret maxed-out cards as higher risk, not responsible use.

Myth: Paying the full balance once a month is enough

Fact:

Timing matters. If balances are high when reported, scores can still drop.

Myth: Utilization matters less if you have perfect payment history

Fact:

Payment history and utilization are separate scoring factors.

Strong payment history does not cancel out high utilization.

How Utilization Fits Into Long-Term Credit Health

Utilization is a short-term signal with long-term consequences if it stays high consistently.

Consistently high utilization can:

- Keep scores lower than expected

- Reduce access to better financial products

- Limit future flexibility

But it is also one of the easiest factors to improve quickly once you understand how reporting works.

That makes it a powerful tool for managing your credit profile intentionally, especially before major financial decisions. This is why utilization management is often recommended in the months leading up to mortgage or auto loan applications.

Why Credit Utilization Affects Some People More Than Others

Two people can have the same utilization percentage and see very different credit score changes. That’s because utilization does not work in isolation. Scoring models evaluate it alongside the rest of your credit profile.

Several factors influence how strongly utilization affects you.

Total Available Credit Limits

People with higher total limits often experience smaller score swings from the same dollar amount of spending.

Example:

- Person A: $2,000 total limit, $800 balance → 40% utilization

- Person B: $20,000 total limit, $800 balance → 4% utilization

Even though spending is identical, the impact is very different.

Lower limits are common among:

- Students

- New credit users

- People rebuilding credit

This makes utilization harder to manage early on, even with modest expenses.

Length of Credit History

If your credit history is short:

- Scoring models have less data to evaluate

- Each factor carries more weight

High utilization on a thin credit file can trigger larger score drops than the same behavior on a long-established profile.

Recent Credit Behavior Patterns

Scoring models are sensitive to trends.

They can detect:

- Sudden spikes in balances

- Repeated cycles of high usage

- Rapid increases across multiple cards

Even if balances are paid later, frequent high reporting can signal rising risk, especially if it’s new behavior.

Mix of Credit Types

People with:

- Only credit cards

- No installment loans

May see utilization carry more influence than someone who also has:

- Auto loans

- Student loans

- Mortgages

A broader credit mix gives scoring models more data points to assess stability.

Utilization vs. Debt-to-Income Ratio: These Are Different Measurements

People often confuse these two concepts.

Credit Utilization

- Used by credit scoring models

- Based on credit limits and balances

- Appears on credit reports

Debt-to-Income Ratio (DTI)

- Used by lenders during applications

- Based on monthly debt payments vs. income

- Not included in credit scores

You can have:

- Low utilization but high DTI

or - High utilization but low DTI

Both matter for approvals, but they are measured separately and used at different stages of lending decisions.

What Happens If Utilization Stays High for a Long Time

Short-term high utilization is usually recoverable.

Long-term high utilization can create secondary problems.

Potential Long-Term Effects

- Fewer credit line increases

- Lower pre-approval offers

- Higher interest rates when approved

- Reduced negotiating power with lenders

This can also affect eligibility for balance transfer offers and promotional interest rates.

Some banks also use internal risk scoring models that:

- Review usage patterns over time

- Consider stability, not just current balances

So even though credit scores only reflect current utilization, lenders may still evaluate longer-term behavior internally.

Does Paying Multiple Times Per Month Help?

Yes, and for a specific reason.

Paying multiple times per month:

- Lowers the balance that appears on statements

- Reduces reported utilization

- Helps manage per-card usage

This does not improve your score directly, but it controls what gets reported, which then affects the score. In other words, it improves the data that scoring models see, not your actual payment history.

It can be especially helpful for:

- People with low credit limits

- Heavy card users who pay in full

- Anyone preparing for a loan application

Should You Open New Cards to Lower Utilization?

Opening new credit can:

- Increase total available limits

- Lower utilization percentage

But it also comes with trade-offs:

Benefits

- More available credit

- Lower utilization if spending stays the same

Risks

- Hard credit inquiry

- New account lowers average account age

- Too many new accounts can hurt approvals

This approach makes more sense when:

- You already have good credit

- You can manage additional accounts responsibly

- You are not applying for major loans soon

Opening new accounts shortly before a mortgage application can sometimes raise underwriting questions, even if scores remain strong.

For people actively preparing for mortgages, opening new credit is usually not recommended shortly before applying.

Store Cards and Buy Now, Pay Later: Hidden Utilization Effects

Store Credit Cards

Retail cards:

- Often have lower limits

- Are included in utilization calculations

A $400 balance on a $500 store card equals 80% utilization, which can significantly affect scores even if major cards look fine. This is why small store cards often cause disproportionate score drops.

Buy Now, Pay Later (BNPL) Services

As of recent years:

- Some BNPL providers have begun reporting certain loans to credit bureaus

- Reporting practices vary by company and product type

Short-term BNPL plans often:

- Do not affect utilization directly

- But missed payments may still be reported as delinquencies

Because reporting rules continue to evolve, BNPL should not be assumed to be invisible to credit profiles.

Utilization and Authorized User Accounts

Being added as an authorized user can affect your utilization.

If the primary cardholder:

- Keeps balances low → can help your credit

- Keeps balances high → can hurt your credit

Authorized user accounts include:

- The card’s full limit

- The reported balance

You may benefit from:

- High-limit cards with low balances

- Long positive payment history

But you also share utilization behavior, even if you never use the card yourself.

If the primary user starts carrying high balances, removing yourself as an authorized user may protect your score.

Early Warning Signs That Utilization Is Hurting You

You may want to review your balances if you notice:

- Score drops without missed payments

- Denials despite stable income

- Reduced pre-approval offers

- Sudden interest rate increases on new accounts

Utilization is often the easiest factor to check and adjust.

Managing Credit Utilization in Different Life Situations

Credit utilization does not exist in a vacuum. The “right” approach can change depending on where you are financially and what you’re preparing for.

Different life stages create different risks and priorities when it comes to credit reporting.

If You Are New to Credit

Common challenges:

- Low credit limits

- Few accounts

- Every purchase moves utilization quickly This makes even normal daily spending risky for utilization when limits are very low.

This makes even normal daily spending risky for utilization when limits are very low.

Best practices:

- Keep statement balances very low (often under 10% of the limit)

- Make small purchases and pay them down before statements close

- Avoid putting large expenses on starter cards

At this stage, utilization can matter more because scoring models have less history to rely on.

If You Are Rebuilding After Credit Problems

High utilization combined with past negatives can compound risk signals.

Best practices:

- Prioritize paying down balances first

- Focus on one card at a time if limits are tight

- Avoid adding new debt until balances stabilize

As utilization improves, scores often rise faster than with almost any other change. This is why utilization management is often the first step recommended in credit recovery plans.

If You Are Financially Stable but Use Cards Heavily

This includes people who:

- Use cards for rewards

- Put regular household expenses on cards

- Pay in full each month

Best practices:

- Track statement closing dates

- Make mid-cycle payments when needed

- Spread spending across multiple cards

This lets you keep earning rewards without showing high reported balances. However, this strategy only works if balances are paid consistently and do not grow month to month.

If You Are Preparing for a Major Loan

Timing matters more than long-term averages.

Best practices in the 1–3 months before applying:

- Keep utilization as low as realistically possible

- Avoid new charges close to statement dates

- Avoid opening or closing accounts

Even temporary reductions can improve how your profile looks during underwriting.

Many lenders rely heavily on automated systems, and small utilization changes can affect approval thresholds.

When Utilization Matters Less Than Other Factors

Utilization is powerful, but it is not always the primary driver of credit outcomes.

Other factors can outweigh utilization when they are present:

- Recent late payments

- Collections or charge-offs

- Very short credit history

- Too many new accounts in a short time

In these cases, lowering utilization still helps, but addressing negative marks and building consistent history becomes more important for long-term improvement.

Utilization and Long-Term Credit Strategy

It helps to think about utilization in two different time frames.

Short-Term Optimization

Used when:

- Applying for credit

- Recovering from recent score drops

Goal:

Keep reported balances very low for best possible score snapshots.

Long-Term Stability

Used when:

- Building sustainable habits

- Managing ongoing expenses

Goal:

Maintain balances that are consistently manageable without stress or missed payments. This approach supports both credit health and real financial stability.

Credit health works best when utilization management fits naturally into your budgeting system, not when it requires constant monitoring or extreme behavior.

Psychological Traps Around Credit Limits

Credit limits are not spending targets.

But many people subconsciously treat them that way, especially when:

- Limits increase

- Income rises

- Promotional offers appear

This can slowly push utilization higher over time, even without financial hardship. Over time, this can normalize higher balances and increase dependence on credit.

A higher limit is meant to provide:

- Flexibility

- Emergency capacity

Not a signal that higher spending is safe or sustainable.

Utilization vs. Emergency Spending

Emergencies are exactly what credit is designed to handle when savings are not immediately available.

If you must use credit for emergencies:

- Focus first on stability, not score optimization

- Then reduce balances as soon as income or insurance reimbursements allow. Prioritizing essential expenses is always more important than protecting short-term credit scores.

Short-term score drops are usually far less important than:

- Keeping utilities on

- Avoiding eviction

- Covering medical needs

Credit health should support financial stability, not replace it.

Common Questions About Paying Off Credit Card Balances

Should I leave a small balance every month?

Not required.

What matters is that a small balance is reported, not that interest is paid.

You can:

- Let a small balance appear on the statement

- Then pay it off before the due date

This shows activity without carrying debt.

Is it bad to pay off cards to zero?

No.

But if all cards report zero at the same time, some scoring models may treat your profile as inactive for that month, which can slightly limit score potential.

This effect is usually small and temporary.

Is rotating balances across cards a good strategy?

It can help with per-card utilization, but it does not reduce overall debt.

It should not be used to:

- Justify spending more

- Delay paying off balances

It is best used as a reporting strategy, not a debt strategy.

Signs Your Utilization Strategy Is Working

You are likely managing utilization well if:

- Your scores remain stable month to month

- You see gradual improvements over time

- You receive regular credit limit increases

- You qualify for better loan terms

Utilization does not need to be perfect. It just needs to be predictable and controlled.

How Credit Bureaus and Scoring Models Actually See Your Utilization

Understanding what gets reported — and how it’s interpreted — helps explain why utilization sometimes changes even when you think nothing has changed.

Many people assume scores track daily spending, but that is not how credit reporting works.

What Lenders Report to Credit Bureaus

Most U.S. credit card issuers report:

- Statement balance

- Credit limit

- Payment status

- Minimum payment due

They typically do not report:

- Daily balances

- How often you use the card

- Whether you paid interest

So when a scoring model calculates utilization, it is using a single monthly snapshot, not your full spending behavior. This is why timing matters more than how often you use your card.

Why Utilization Can Change Without New Spending

Utilization can increase even when you did not make new purchases, such as when:

- A credit limit is reduced by the issuer

- A promotional limit expires

- A card is closed

- A balance transfer offer ends

Any reduction in available credit raises utilization automatically if balances remain the same.

For example, if your limit drops from $5,000 to $3,000 while your balance stays at $1,500, your utilization jumps from 30% to 50% without spending anything new.

Utilization and Balance Transfers

Balance transfers can temporarily increase utilization on:

- The receiving card

- Overall profile

Even if total debt stays the same, moving balances can cause:

- One card to spike

- Short-term score dips

Scores usually recover as balances are paid down, but timing matters if you plan to apply for new credit soon. It is usually better to complete balance transfers well before major loan applications.

Why Some Cards Report at Different Times

Not all lenders report on the statement closing date.

Some may report:

- On fixed calendar dates

- After payments post

- At different times for different accounts

This can cause:

- Short-term mismatches between actual balances and reported balances

- Temporary score changes. These changes often correct themselves once all lenders finish reporting for the month.

Because of this, checking your credit report or score immediately after making a payment may not reflect the change yet.

Monitoring Utilization the Right Way

Credit Card Statements

Your statement shows:

- Statement balance

- Credit limit

- Closing date

This is usually the best indicator of what will be reported.

Credit Reports

Your credit reports show:

- Last reported balance

- Credit limit per account

However:

- Reporting dates may differ by lender

- Updates can lag by several days or weeks

This is why checking your bank statement is often more reliable for tracking utilization than checking your credit score app.

Credit Scores

Scores can:

- Change as soon as new data is reported

- Fluctuate month to month even without mistakes

Small changes are normal and do not necessarily indicate problems.

Utilization and Credit Score Models: Not All Scores React the Same Way

Different scoring models weigh utilization slightly differently.

- Older FICO versions (still used by some lenders) may react more strongly to moderate utilization.

- Newer models can be more sensitive to recent spikes and trends.

- VantageScore may respond differently to zero balances than some FICO versions.

This is why you may see:

- Different scores across platforms

- Different changes from the same behavior

What matters most is that all major models penalize consistently high utilization. This is why utilization management is helpful regardless of which score version a lender uses.

Why Credit Karma and Similar Apps Can Be Misleading

Educational credit monitoring tools are useful, but they can:

- Emphasize short-term changes

- Use scoring models not used by lenders

- Trigger concern over minor fluctuations. This can lead people to make unnecessary changes based on very small score movements.

A small drop due to utilization usually corrects itself once balances report lower again.

What matters more is:

- Overall direction over time

- Whether major negative items are appearing. Major negative items matter far more than small utilization shifts.

When Utilization Is Not the Real Problem

Sometimes utilization gets blamed when other factors are responsible.

Score drops may also be caused by:

- New hard inquiries

- New accounts lowering average age

- Late payments

- Collections or disputes updating

Utilization is important, but it should be evaluated alongside the full credit picture.

How Long It Takes for Utilization Improvements to Affect Scores

Because utilization updates with new reports:

- Improvements can reflect within one reporting cycle

- Often within 30 to 45 days. This assumes balances are reduced before the next statement closes.

There is no long recovery period once balances are reduced, as long as no other negative events are present.

This is why utilization management is often used before:

- Mortgage applications

- Auto financing

- Credit limit requests

What Lenders May Look At Beyond the Score

Even when your score improves, lenders may also consider:

- Recent account behavior

- Payment consistency

- Internal usage patterns on their own cards

This means that while utilization drives the score, lender decisions may use additional internal data, especially for existing customers. This is why someone can have a strong score but still receive different terms from different banks.

Common Utilization Tactics: What Helps, What Doesn’t, and What Can Backfire

A lot of advice online focuses on “credit hacks.” Some are useful, some are neutral, and some can create new problems. It helps to separate practical strategies from myths.

Some tactics may improve how your credit looks short term, while others can quietly hurt you over time.

Tactic: Keeping a Small Balance on Purpose

What people think:

Leaving a small balance improves credit.

What actually matters:

A small balance must be reported, but it does not need to be carried past the due date.

You can:

- Let a small amount appear on the statement

- Then pay it in full before the due date

- Avoid interest entirely. Interest paid does not help your credit score in any way.

Carrying a balance and paying interest does not build credit faster.

Tactic: Paying Cards to Zero Immediately After Every Purchase

This keeps utilization extremely low, but:

- It is not necessary for good credit

- It can be inconvenient to manage

- It may reduce reported activity if balances always report as zero

For most people, paying before the statement closes — not after every purchase — is enough. This approach keeps utilization low without turning credit management into a daily task.

Tactic: Rotating Debt Between Cards

Moving balances around may:

- Lower per-card utilization

- Keep total utilization the same

This can help short-term reporting, but it does not solve:

- Overall debt levels

- Interest costs

It should not be used as a substitute for paying down balances. If balances keep rotating without decreasing, long-term interest costs and financial stress usually increase.

Tactic: Opening Cards Just for Higher Limits

More limits can reduce utilization, but:

- Hard inquiries may lower scores temporarily

- Too many new accounts can hurt credit profiles

- Some lenders view rapid credit expansion as risk

This approach works best when:

- You already manage balances well

- You are not about to apply for major loans

It is not ideal during active credit rebuilding or mortgage preparation. Mortgage lenders often prefer to see stable accounts rather than recently opened credit lines.

Tactic: Closing Cards to “Simplify” Finances

Closing cards can:

- Reduce available credit

- Increase utilization instantly

- Shorten credit history over time

If a card has:

- No annual fee

- No management problems

Keeping it open often helps long-term utilization and credit history, even if you rarely use it. Using the card once or twice a year can also help prevent automatic closures due to inactivity.

How Utilization Fits Into Debt Payoff Strategies

When paying off debt, people often choose between:

- Avalanche (highest interest first)

- Snowball (smallest balance first)

From a credit score perspective:

- Paying down high-utilization cards can produce faster score improvements

- Especially when those cards are near or over 50% utilization

That does not change which method saves more interest, but it explains why some people see score gains faster when they target heavily used cards first. This can be motivating early in a payoff plan, even if it is not always the cheapest approach.

Balancing Credit Scores vs. Financial Priorities

Credit optimization should never replace:

- Emergency savings

- Rent and utility payments

- Insurance coverage

If paying down credit cards means:

- Skipping medical care

- Missing rent

- Avoiding needed car repairs

Then score optimization is not the priority. Stability and safety always come before credit metrics.

Utilization management works best when it fits within a stable financial foundation, not when it creates new risks.

Utilization During Promotional APR Periods

0% introductory APR offers can:

- Reduce interest costs

- Allow strategic payoff plans

But they do not change how utilization is scored.

Even with 0% APR:

- High balances still count toward utilization

- Scores can still drop while balances are high

This is important if you plan to:

- Apply for other credit during the promo period

You may need to reduce balances before applying, even if interest is not accruing. Many people are surprised when scores drop during promotional periods despite making on-time payments.

Utilization and Joint Accounts

On joint credit card accounts:

- Both parties’ credit reports reflect the same balances and limits

- Utilization affects both profiles

If one person carries high balances, both may see score effects, even if only one person is spending.

Clear communication matters when credit is shared. If spending habits change, removing joint or authorized accounts may protect both parties.

When It’s Okay Not to Worry About Utilization

There are times when utilization should not be the main concern, such as when:

- You are focused on paying off high-interest debt

- You are stabilizing after financial setbacks

- You are not planning to apply for credit

In these cases, short-term score drops are usually less important than improving long-term financial health.

Utilization can be optimized later once balances are under control.

Practical Warning Signs of Risky Utilization Patterns

You may want to reassess spending or budgeting if:

- Balances never drop significantly month to month

- You rely on cards to cover basic expenses

- Limits increase but balances rise just as fast

- Minimum payments are getting harder to manage

These are financial stability issues first, not credit score issues.

Myths and Misunderstandings That Keep Hurting Credit Scores

Even people who are careful with money often follow outdated or incorrect advice about how credit works. These myths can quietly hold scores down for years.

Many of these beliefs are repeated online and passed between friends, even though they do not match how modern credit scoring models work.

Myth: Using More of Your Credit Helps Prove Responsibility

Reality:

Credit scoring models do not reward heavy usage. They reward low, controlled usage with consistent payments.

Maxing out cards — even temporarily — increases perceived risk, not trust. High balances are one of the strongest signals of potential future payment trouble in scoring models.

Myth: You Must Carry Debt to Build Credit

Reality:

Credit history builds from:

- On-time payments

- Active accounts

- Time

Interest paid does not improve scores. Carrying balances simply increases costs without improving credit outcomes. Many people pay unnecessary interest because of this misunderstanding.

Myth: Closing Cards Always Helps Financial Health

Reality:

Closing unused cards can:

- Increase utilization

- Shorten average credit age

- Reduce future flexibility

Financial simplicity matters, but it should be balanced against credit impact, especially before major applications. Closing accounts shortly before applying for a loan can also raise lender questions about recent changes in your profile.

Myth: All Utilization Is Viewed the Same

Reality:

Scoring models evaluate:

- Per-card utilization

- Overall utilization

- Sudden increases

- Persistent patterns

Where and how balances appear matters, not just total percentages. This is why moving the same balance between cards can change scores even if total debt does not change.

Myth: One High Month of Utilization Ruins Your Credit

Reality:

Utilization has no long-term memory in scoring models.

Once balances drop and new data is reported, scores typically recover unless other negatives are present. This is why temporary spending spikes rarely cause lasting damage by themselves.

What Actually Builds Strong Credit Profiles Over Time

Utilization is important, but it works best alongside other habits.

Strong credit profiles usually show:

- Long-term on-time payment history

- Stable credit limits

- Moderate, consistent usage

- Limited new credit applications

- Few or no negative marks

Utilization helps shape the month-to-month score, but payment history and time carry the most long-term weight. Utilization mainly affects short-term score movement, not long-term credit reputation.

Thinking About Utilization as Part of Overall Money Management

Utilization management should not feel like constant micromanagement.

Healthy long-term patterns include:

- Using credit as a payment tool, not as income

- Paying balances regularly

- Avoiding chronic reliance on minimum payments

When these habits are in place, utilization tends to stay within healthy ranges naturally. This is usually easier to maintain than trying to control utilization month by month.

How Utilization Interacts With Other Credit Score Factors

Here’s how utilization fits into the bigger scoring picture:

| Credit Factor | Long-Term Impact | Short-Term Impact |

|---|---|---|

| Payment history | Very high | Moderate |

| Credit utilization | Moderate | Very high |

| Credit age | High | Low |

| New credit | Moderate | Moderate |

| Credit mix | Low to moderate | Low |

This is why utilization changes can cause quick score swings, while other improvements take longer to show.

When People Over-Optimize and Create New Problems

Trying to chase perfect utilization can sometimes:

- Encourage opening too many accounts

- Lead to constant monitoring stress

- Distract from bigger financial goals

Credit scores are tools, not life scores. They should support your financial goals, not control every spending decision.

Good enough, consistent behavior usually produces excellent long-term results without extreme strategies.

What Credit Utilization Does NOT Tell Lenders

Utilization does not show:

- Your income

- Your savings

- Your job stability

- Your household expenses

It only reflects how much of your credit limits are in use at reporting time.

This is why credit profiles sometimes do not reflect real financial strength — and why lenders also use income and DTI during applications.

How to Use Utilization Strategically Without Overthinking It

A simple, sustainable approach for most people:

- Keep reported balances under 30% overall

- Try to stay under 30% on individual cards

- Use early payments when preparing for applications

- Do not carry balances just to “build credit”

This keeps utilization from becoming a problem without requiring constant tracking. Minor month-to-month fluctuations are normal and rarely worth stressing over.

Common Credit Utilization Questions Explained

These are practical situations many Americans run into, and the answers are often misunderstood. Clear answers can help you avoid unnecessary score drops and financial stress.

-

Does Utilization Reset Every Month?

Yes.

Utilization is recalculated each time new balances are reported.

Most cards report once per billing cycle.That means:

– High utilization last month does not permanently hurt your score

– Lower balances this month can improve your score quickly. This assumes lower balances are reported on the next statement.This is one of the most common reasons people see unexpected score drops.

This is very different from late payments or collections, which remain on reports for years.

-

If I Pay in Full Every Month, Why Did My Score Drop?

Most likely because:

– Your balance was high on the statement closing date

– That higher balance was reported to the credit bureausEven if you paid in full later, the score is based on what was reported, not what was eventually paid.

-

Should I Pay Before or After the Statement Closes?

For utilization control:

– Pay before the statement closes to lower the reported balance

For avoiding interest:

– Pay by the due date

You can do both by making:

– One payment before the statement closes (to manage utilization)

– One payment after the statement posts (to pay in full)This strategy lets you control utilization without ever paying interest.

-

Does Using Debit Instead of Credit Help Utilization?

Yes, indirectly.

Debit spending:

– Does not affect credit utilization

– Does not appear on credit reportsIf high utilization is becoming hard to manage, shifting some spending to debit can reduce reported balances — but it also means you are no longer building card activity on that spending. For people building credit, this trade-off should be considered carefully.

-

Do Authorized User Balances Count Toward My Utilization?

Yes.

Authorized user accounts typically appear on your credit report with:

– Full credit limit

– Full reported balanceIf the primary user keeps high balances, your utilization can increase even if you never use the card. If balances stay high, removing yourself as an authorized user can protect your score.

-

Can Credit Line Decreases Hurt My Score Even If I Do Nothing Wrong?

Yes.

– If a lender lowers your limit:

Your utilization increases automatically if balances stay the same

This can happen due to:– Inactivity

– Changes in lender risk policies

– Broader economic conditionsThis is why utilization can rise even without new spending. Once balances are reduced or limits are restored, scores usually recover.

-

Why Did My Score Drop After Paying Off a Loan?

This is usually not utilization-related.

Paying off installment loans can:

– Change your credit mix

– Reduce the number of active accountsUtilization applies mainly to revolving credit, not closed loans. Any score change after loan payoff usually comes from changes in credit mix or account activity.

-

Does Carrying a Balance Help With Credit Limit Increases?

Not necessarily.

Banks look at:

– Payment history

– Income (if updated)

– Risk patternsHigh balances may actually signal higher risk, which can reduce chances of increases.

-

Is It Bad to Use More Credit Right After Getting a New Card?

New cards usually have:

– Lower starting limits

– Short account ageUsing a large portion of that limit can:

– Spike utilization quickly

– Have stronger score impactIt’s usually better to use new cards lightly at first while history builds. This helps protect both utilization and account stability during the early months.

-

When Utilization Concerns Are Overblown

Small score movements caused by utilization are common and often temporary.

You usually do not need to worry if:

– Scores fluctuate by a few points

– You are not applying for credit soon

– You are paying balances down steadilyCredit scores are meant to track risk trends, not punish normal spending.

-

How to Think About Utilization Without Stress

A realistic mindset:

– Credit is a tool, not a test you can fail

– Perfect utilization is not required for excellent credit

– Consistency matters more than occasional spikesIf you:

– Pay on time

– Avoid long-term high balances

– Monitor major changesYour utilization will usually stay in healthy ranges naturally. You do not need perfect numbers every month to have excellent long-term credit.

A Simple, Sustainable Framework for Managing Credit Utilization

Rather than chasing exact percentages every month, it helps to follow a system that fits into normal financial routines.

Monthly Baseline Habits

For most people, these three habits are enough:

- Know your statement closing dates

This tells you when balances are likely to be reported. You can usually find this date on your statement or in your online account. - Avoid letting any single card exceed about 30% at statement time

This protects both per-card and overall utilization. It also reduces the chance of sudden score drops from a single high balance. - Pay balances in full by the due date whenever possible

This prevents interest and keeps debt from growing. Avoiding interest makes it easier to keep balances under control over time.

These steps handle most utilization issues without constant tracking.

When You Should Be More Aggressive

Increase focus on utilization when:

- You plan to apply for credit in the next 1–3 months

- Your score recently dropped without other obvious reasons

- Your balances have increased due to temporary expenses

In these periods:

- Aim for very low statement balances

- Delay large purchases if possible

- Avoid account changes

This creates the best short-term snapshot for lenders.

Small short-term adjustments can have a big impact during application reviews.

When You Can Relax About Utilization

You usually do not need to optimize utilization when:

- You are not seeking new credit

- Balances are steadily decreasing

- Your emergency savings and bills are stable

Long-term credit health benefits more from:

- Lower debt

- Strong cash flow

- Consistent payments

than from chasing perfect utilization percentages. Long-term consistency matters far more than short-term perfection.

Integrating Utilization Into Normal Budgeting

Utilization control works best when it supports — not replaces — basic money management.

Budgeting Comes First

Before worrying about utilization:

- Track monthly spending

- Ensure bills and savings are covered

- Build emergency funds when possible

When cash flow improves, utilization often improves naturally because balances become easier to manage. This is why improving income and spending control often helps credit scores indirectly.

Using Credit Cards as Payment Tools, Not Financing Tools

Healthy utilization patterns usually come from:

- Treating cards like debit with delayed withdrawal

- Not relying on future income to cover current spending

When credit becomes a substitute for income, utilization tends to rise and stay high. This is one of the strongest warning signs of long-term financial strain.

How to Set Personal Utilization Targets

Instead of focusing on one universal rule, it helps to think in tiers:

| Situation | Suggested Focus |

|---|---|

| Everyday use, no applications planned | Keep under ~30% |

| Building or rebuilding credit | Try to stay under ~20% |

| Preparing for major loan | Aim for under ~10% |

| Emergency period | Focus on stability first, optimize later |

These are practical targets, not legal or scoring thresholds.

What Utilization Can and Cannot Do for Your Financial Life

What It Can Do

- Influence credit scores quickly

- Affect loan approvals and rates

- Shape how lenders assess short-term risk

What It Cannot Do

- Fix late payments

- Replace income growth

- Compensate for unstable finances

- Eliminate debt by itself

Utilization is one piece of a much larger financial picture. Strong financial health requires income stability, savings, and responsible spending alongside good credit habits.

Final Perspective Before the FAQs

Credit utilization matters because:

- It reflects how heavily you rely on borrowed money at a given moment

- Lenders and scoring systems associate high usage with higher risk

But it should not become:

- A source of anxiety

- A reason to avoid necessary expenses

- A distraction from building real financial security

When understood correctly, utilization becomes a management tool, not a constant worry. It should support your financial goals, not control your everyday decisions.

Frequently Asked Questions About Credit Utilization Ratio

-

What is the best credit utilization ratio for a good credit score?

For most people, keeping overall utilization below 30% helps protect their score.

Many people with excellent credit keep utilization below 10%, but that level is not required for good credit. What matters most is avoiding consistently high usage.Short-term spikes are usually less important than long-term patterns.

-

Is 30% a strict rule or just a guideline?

It is a guideline, not a legal or scoring cutoff.

Credit scores do not suddenly drop at exactly 30%, but risk tends to increase as utilization rises, and many people begin seeing score declines once they cross that range.

The higher utilization goes, the stronger the risk signal becomes to scoring models. -

Does utilization matter if I pay my credit card in full every month?

Yes.

Utilization is based on the balance that is reported, not whether you eventually pay interest.

If your statement closes with a high balance, that balance affects your utilization even if you pay in full later.

This surprises many people who assume full payment automatically protects their score. -

How can I keep utilization low if I use my card for most expenses?

You can manage reporting without changing spending by:

– Making a payment before the statement closes

– Spreading purchases across multiple cards

– Avoiding large charges close to the closing dateKnowing your closing dates makes this much easier to manage.

This lowers the balance that gets reported while allowing normal card use.

-

Does utilization include pending transactions?

No.

Utilization is calculated using posted balances, not pending charges.

However, once transactions post, they will be included in the reported balance. -

Does utilization affect mortgage approval?

Indirectly, yes.

Utilization affects your credit score, and your score affects:

– Mortgage eligibility

– Interest rates

– Required down payments in some programsLenders also review debt-to-income separately, but utilization can still influence how strong your profile looks. Even small score differences can affect interest rates on large loans.

-

Should I close unused credit cards to improve utilization?

Usually no.

Closing cards:

– Reduces available credit

– Can raise utilization instantly

– May shorten average account age over timeIf a card has no annual fee and is not causing problems, keeping it open often helps utilization. Using the card occasionally can also prevent automatic closures due to inactivity.

-

Why did my score drop after I paid off my card?

This is uncommon but can happen when:

– All cards report zero balances at once

– Credit mix changes

– Other account updates occurred at the same timeMost of the time, utilization decreases improve scores, but short-term variations can occur depending on what else updated that month. In most cases, these changes correct themselves over time.

-

Do business credit cards affect personal utilization?

Some business cards:

– Do not report balances to personal credit reports

– But may report late paymentsOthers do report like personal cards.

It depends on the issuer and the specific product, so business card utilization is not automatically invisible to personal credit. Always check the issuer’s reporting policy before assuming business balances will not affect your personal credit. -

How long does it take for utilization improvements to raise my score?

Often within one reporting cycle, usually 30 to 45 days, once lower balances are reported to the credit bureaus. This usually happens after your next statement closes.

There is no long recovery period after utilization drops, as long as no other negative factors are present.

-

Can using too little credit hurt my score?

If all cards consistently report zero balances, some scoring models may treat your profile as inactive for that month, which can slightly limit score potential.

Allowing a small balance to report occasionally can help show ongoing activity, but this effect is usually minor. It should not be a reason to carry debt or pay interest.

-

Does utilization affect insurance rates or job background checks?

Credit-based insurance scores in some states may consider similar factors as credit scores, including utilization.

Employment background checks generally do not use credit scores, but some employers may review credit reports for certain financial positions, where high debt may raise concerns.Rules vary by state and employer policies.

-

Should I worry about utilization if I am focused on paying off debt?

Your top priority should be:

– Reducing high-interest balances

– Stabilizing cash flowUtilization usually improves naturally as debt decreases.

Short-term score changes matter less than long-term financial recovery. Lower debt and stronger cash flow usually improve credit over time as well.

Disclaimer

This article is for educational and informational purposes only and should not be considered legal, tax, or financial advice. Credit rules, lender policies, and scoring outcomes may vary depending on individual financial circumstances and institutional practices.

Readers should consult a qualified financial professional, tax advisor, or attorney before making major financial decisions.

1 thought on “Credit Utilization Ratio: How Much Credit Should You Use for a Good Score?”