Overdraft fees are one of the most common — and most misunderstood — charges in the U.S. banking system. For many Americans, a small timing mismatch between income and expenses can turn an ordinary purchase or bill payment into an unexpected $30–$35 fee. These fees don’t usually happen because of reckless spending, but because of how banks process transactions, apply rules, and prioritize payments behind the scenes.

In this guide, you’ll learn exactly what overdraft fees are, how and why they happen in real life, which transactions can legally trigger them, and how U.S. banking rules regulate these charges. More importantly, you’ll understand practical, proven ways to avoid overdraft fees — even if you live paycheck to paycheck or rely on automatic payments. Whether you’re new to managing a checking account or want a deeper understanding of how overdraft programs really work, this article gives you the complete picture.

Key Takeaways

- Overdraft fee happen when your bank or credit union approves a payment that exceeds your available balance.

- One small mistake can trigger multiple fees in a single day.

- Federal rules require your permission before banks can charge overdraft fees on debit card and ATM transactions.

- Many overdraft fees are avoidable with the right account settings and habits.

Why Overdraft Fees Matter in Everyday American Life

For many Americans, checking accounts handle rent, groceries, utilities, subscriptions, and daily spending. When money is tight or timing is off by even a few hours between deposits and payments, a simple purchase can turn into an expensive mistake.

A cup of coffee, a streaming subscription, or an automatic bill payment can suddenly cost $35 or more in fees — not because the item was expensive, but because the account balance dipped below zero.

What makes overdraft fees especially frustrating is that:

- They often happen during normal, everyday spending

- People may not realize the account is overdrawn until after fees are charged

- One overdraft can trigger multiple fees in a short period

Understanding how overdraft fees actually work — and when banks are allowed to charge them — gives you real control over your checking account and helps protect your monthly budget.

What Is an Overdraft Fee?

An overdraft fee is a charge your bank or credit union may apply when:

You spend or withdraw more money than your available checking account balance, and the bank chooses to approve the transaction anyway.

Instead of declining the payment, the bank temporarily covers the missing amount and expects you to repay it. For that service, the bank may charge an overdraft fee.

Typical U.S. overdraft fees at large banks are often around $30–$35 per transaction, though exact amounts vary by institution and account type.

How Overdrafts Actually Happen in Real Life

Most overdrafts are not caused by reckless spending. They usually happen because of timing issues and everyday banking habits, such as:

- A paycheck arriving later than expected

- Automatic bills posting earlier than usual

- Gas station or hotel charges posting after pending transactions clear

- Subscriptions renewing when you forgot they were active

- Misreading “available balance” versus “current balance” in your app

Here’s a simple example:

You have $40 in your checking account.

Your phone bill of $60 processes overnight.

The bank pays it, your balance becomes –$20, and the bank charges a $35 overdraft fee.

Now you owe $55 — even though you were only short by $20.

If more payments post before you add money, each one can trigger another fee.

What Types of Transactions Can Trigger Overdraft Fees?

Not all transactions are treated the same under U.S. banking rules.

Debit Card Purchases and ATM Withdrawals

These are covered by federal opt-in rules:

- Banks cannot charge overdraft fees on debit card and ATM transactions unless you explicitly agree (opt in).

- If you do not opt in, the transaction is usually declined instead of being approved with a fee.

This rule comes from the Federal Reserve’s Regulation E. Regulation E is a federal consumer protection rule that governs electronic payments in the U.S

Checks and Automatic Payments (ACH)

These work differently:

- Banks can charge overdraft fees for:

- Checks

- Online bill payments

- Automatic withdrawals (rent, utilities, subscriptions)

Even if you did not opt in for debit card overdrafts, these payments can still overdraw your account and trigger fees.

Many people assume opting out fully protects them — but it only applies to debit and ATM transactions, not bills and checks.

Overdraft Fees vs. NSF Fees: What’s the Difference?

These two fees are often confused, but they are not the same.

| Situation | What Happens | Possible Fee |

|---|---|---|

| Bank pays the transaction even though balance is too low | Account goes negative | Overdraft fee |

| Bank rejects the transaction due to low funds | Payment fails | NSF (Non-Sufficient Funds) fee |

Some banks charge either type, depending on how the transaction is handled.

Important:

If a payment is rejected and then retried by the merchant later, you could face multiple NSF fees from repeat attempts.

Why Banks Charge Overdraft Fees at All

From a bank’s perspective, overdraft coverage is considered a short-term loan — they advance money on your behalf and expect quick repayment.

Banks argue overdraft programs:

- Allow payments to go through

- Prevent declined transactions

- Provide convenience in emergencies

But consumer protection agencies have long pointed out that:

- Fees are very high compared to the amount overdrawn

- Low-balance customers are charged far more often

- Fees can create a cycle that’s hard to escape

Because of this, overdraft fees have been a major focus of U.S. banking regulation and consumer protection policy.

Who Is Most at Risk of Overdraft Fees?

Overdraft fees tend to affect people who:

- Live paycheck to paycheck

- Have unpredictable income

- Rely on automatic bill payments

- Keep low daily balances

- Are new to managing checking accounts

Students, gig workers, and households with tight monthly margins often face the highest risk — not due to poor decisions, but because small timing differences can have big consequences.

How Overdraft Programs Work Inside U.S. Banks

When your account balance drops below zero, your bank has two basic options:

- Decline the transaction (no overdraft, but the payment fails), or

- Approve the transaction and overdraw your account, then charge a fee

If your bank approves it, you are using what’s commonly called overdraft coverage (sometimes also called overdraft protection by banks, but not the same as linked-account protection, which we’ll explain later).

This decision happens automatically through the bank’s internal systems. The system does not look at how small or large the purchase is — it simply follows preset rules. There is no human reviewing each transaction in real time.

Once the transaction posts:

- Your account shows a negative balance

- The overdraft fee is added

- You are expected to deposit money quickly to bring the account back positive

Some banks also charge additional fees if the account stays negative for several days.

How Much Are Overdraft Fees in the U.S.?

There is no federal cap on overdraft fees for checking accounts, but most large U.S. banks historically charged around $30 to $38 per overdraft.

In recent years, some banks have reduced fees or eliminated them, but many accounts — especially older or basic checking accounts — still carry overdraft charges.

Common fee structures include:

| Fee Type | What It Means |

|---|---|

| Per-item overdraft fee | Charged each time a transaction overdraws the account |

| Daily maximum | Limit on how many overdraft fees can be charged per day |

| Extended overdraft fee | Extra fee if balance stays negative for several days |

Daily Fee Caps (Why Multiple Fees Add Up Fast)

Many banks set a daily limit, such as:

- Maximum 3–5 overdraft fees per day

That still means a person could be charged $90 to $175 in one day if several payments post while the balance is low.

This often happens when:

- Multiple subscriptions process overnight

- Rent and utilities post on the same day

- Debit card transactions from previous days finally finish processing

Even small purchases can stack up into large fee totals.

Extended Overdraft Fees (Sometimes Called Sustained Negative Balance Fees)

Some banks charge an additional fee if:

- Your account remains overdrawn for a certain number of days (often 5–7 days)

This is separate from the original overdraft fee. These are sometimes called “sustained negative balance fees” in bank disclosures.

For example:

- Day 1: Overdraft fee charged

- Day 5 or 7: Additional “extended overdraft” fee added

Not all banks charge this, but when they do, it can make it harder to recover financially if you’re already short on funds.

Overdraft Coverage vs. Overdraft Protection: Not the Same Thing

These terms sound similar but work very differently.

Overdraft Coverage (Fee-Based)

This is the standard overdraft program:

- Bank pays the transaction

- Account goes negative

- Overdraft fee is charged

This is what most people think of when they hear “overdraft fee.”

Overdraft Protection (Linked Account or Credit)

With overdraft protection, your bank links your checking account to:

- A savings account, or

- A credit card, or

- A line of credit

When your checking balance is too low:

- Money is transferred automatically to cover the payment

- Instead of an overdraft fee, you may pay:

- A small transfer fee, or

- Interest (if using credit)

This can reduce or eliminate overdraft fees, but it still has costs and rules.

Important differences to understand:

| Feature | Overdraft Coverage | Overdraft Protection |

|---|---|---|

| Transaction approved? | Yes | Yes |

| Account goes negative? | Yes | Usually no |

| Fee type | High overdraft fee | Transfer fee or interest |

| Requires setup | Often automatic | Must be enrolled |

Overdraft protection is not free money — it simply changes how the shortfall is funded.

When Banks Are Allowed to Reorder Transactions (Posting Order)

Another factor that affects overdraft fees is transaction posting order — the sequence in which banks process transactions.

Historically, some banks processed:

- Larger transactions first, then

- Smaller ones later

That could cause:

- One large charge to overdraw the account

- Then many small charges to trigger multiple overdraft fees

Due to lawsuits and regulatory pressure, many banks now post transactions:

- In chronological order, or

- By category (debits vs credits)

However, posting policies still vary by institution. You can usually find your bank’s posting order policy in its account agreement or fee schedule. and consumers usually have little control over the exact timing.

This is why checking “pending transactions” and “available balance” both matter when managing a low balance.

How Overdraft Fees Affect Your Long-Term Finances

Overdraft fees do more than reduce your current balance.

They can also:

- Make it harder to pay upcoming bills

- Increase reliance on credit cards or payday-style borrowing

- Lead to account closure if negative balances aren’t resolved

- Get reported to specialty banking databases that banks use when screening new account applications

While overdrafts themselves are not reported to credit bureaus, unpaid negative balances that go to collections can affect your credit.

So while overdraft fees start as a checking account issue, they can eventually create broader financial problems if they snowball.

Who Overdraft Programs Help — and Who Should Avoid Them

Overdraft programs are often presented as a safety net, but in practice, they do not benefit everyone equally. Whether they help or hurt depends on how often you face low balances and how quickly you can replace the missing money.

Situations Where Overdraft Coverage May Help

Overdraft coverage can be useful when:

- A critical payment (like rent or utilities) must go through

- You expect money to arrive within a day or two

- The fee is less harmful than the consequences of a declined payment (late fees, service shutoff, penalties)

In these cases, paying one overdraft fee may be the least damaging option available at that moment.

Situations Where Overdraft Coverage Often Causes More Harm

Overdraft programs tend to hurt people who:

- Frequently carry balances near zero

- Have irregular income schedules

- Rely on multiple automatic payments

- Do not receive real-time balance alerts

For these households, overdraft coverage often becomes:

- A repeated fee cycle

- A drain on already-limited cash

- A source of financial stress rather than protection

When overdrafts happen often, declined transactions can be safer than approved ones with high fees.

Pros and Cons of Using Overdraft Coverage

| Pros | Cons |

|---|---|

| Allows urgent payments to go through | Fees are high compared to the amount borrowed |

| Prevents declined card transactions | Multiple fees can happen in a single day |

| Can avoid late fees or service interruptions | Fees reduce money available for future bills |

| Helpful in short-term emergencies | Can create repeated negative balances |

This comparison shows why overdraft coverage works best as a backup plan, not as a regular spending tool.

Critical takeaway: Overdraft coverage should be treated as emergency backup, not routine cash flow support.

Common Myths About Overdraft Fees (and the Facts)

Many people misunderstand how overdraft programs actually work, which leads to costly surprises.

Myth 1: “If I don’t have money, the bank will just decline the charge.”

Fact:

Bills, checks, and automatic payments can still be approved and charged overdraft fees even if you opted out of debit card overdrafts.

Myth 2: “Overdraft fees are a form of loan with normal interest.”

Fact:

Overdraft fees are flat charges, not interest-based. Borrowing $5 and paying a $35 fee is effectively extremely expensive, even though it is not labeled as interest.

Myth 3: “Banks must warn me before charging overdraft fees.”

Fact:

Banks are required to provide disclosures when you open the account and to offer alerts if you enroll, but they are not required to stop a transaction or warn you in real time before a fee is charged.

Myth 4: “Opting out means I can never overdraft.”

Fact:

Opting out only blocks overdraft fees on debit card and ATM transactions. Other payments can still overdraft your account.

How to Avoid Overdraft Fee: Practical, Proven Strategies

Avoiding overdraft fees usually requires a mix of account settings and daily habits. No single step works for everyone, but together they significantly reduce risk.

These steps work best when used together, not just one at a time.

Turn Off Debit Card Overdraft Coverage (If It’s On)

If you prefer declined transactions over fees:

- Confirm that you are opted out of debit card and ATM overdraft coverage

- This prevents most everyday purchases from triggering fees

You can usually change this setting:

- Through online banking

- In the mobile app

- By calling customer service

Set Low-Balance Alerts

Most banks allow you to receive alerts when your balance falls below:

- A specific dollar amount you choose

These alerts help you:

- Transfer money

- Delay spending

- Prevent automatic payments from hitting unexpectedly

Alerts are especially helpful if your income or expenses vary from week to week.

Use Linked-Account Overdraft Protection Carefully

Linking a savings account can:

- Cover shortfalls automatically

- Avoid large overdraft fees

But keep in mind:

- Transfers may still carry small fees

- Draining savings repeatedly can undermine emergency funds

This option works best when:

- You already maintain a savings cushion

- Overdrafts are rare and accidental

Keep a Small Buffer in Checking

Many people intentionally leave:

- $50 to $200 as a “do not spend” buffer

This helps absorb:

- Posting delays

- Unexpected subscriptions

- Gas station or restaurant adjustments

This strategy requires discipline, but it is one of the most effective protections.

Watch Pending vs. Posted Transactions

Your bank app often shows:

- Current balance

- Available balance

Available balance usually reflects pending charges. Relying only on posted balances can give a false sense of how much you can safely spend.

When money is tight, available balance is the safer number to trust.

Review Subscriptions and Auto-Payments Regularly

Old subscriptions are one of the most common causes of surprise overdrafts.

At least once every few months:

- Review bank statements

- Cancel unused services

- Adjust billing dates when possible

This reduces the risk of multiple charges hitting on the same day.

Step-by-Step: What to Do If You’ve Already Been Charged an Overdraft Fee

If you notice an overdraft fee on your account, acting quickly can help limit the damage.

Step 1: Deposit or Transfer Money as Soon as Possible

This prevents:

- Additional overdrafts

- Extended negative balance fees

Step 2: Check Exactly What Triggered the Fee

Look for:

- The specific transaction

- Whether it was debit, bill pay, or automatic withdrawal

Understanding the cause helps prevent repeat fees.

Step 3: Contact Your Bank and Ask Politely About a Fee Reversal

Many banks may:

- Refund occasional overdraft fees

- Especially if you have not requested reversals often

There is no legal requirement that banks must refund it, but asking costs nothing and sometimes works.

Step 4: Adjust Account Settings Immediately

After an overdraft:

- Review opt-in status

- Set alerts

- Consider linking savings

Preventing the next one is just as important as dealing with the current fee.

U.S. Rules and Consumer Protections Around Overdraft Fees

Overdraft fees are legal in the United States, but they are regulated in specific ways to protect consumers from unfair or deceptive practices. Understanding these rules helps you know what banks must — and do not have to — do when it comes to charging overdraft fees.

Federal Opt-In Rule for Debit Card and ATM Transactions

This requirement comes from the federal Regulation E opt-in rule, which governs how banks can charge overdraft fees on debit card and ATM transactions.

Under Regulation E (Federal Reserve rules for electronic payments):

- Banks cannot charge overdraft fees on:

- Debit card purchases

- ATM withdrawals

- Unless you explicitly opt in

This opt-in must be:

- Clear and voluntary

- Documented by the bank

If you never opted in, those transactions should be declined instead of approved with a fee. You can usually check or change your opt-in status in your bank’s mobile app or by calling customer service.

Important:

This rule does not apply to checks or automatic payments (ACH). Banks may still charge overdraft fees on those even if you opted out of debit overdrafts.

Disclosure Requirements

Banks must clearly disclose:

- When overdraft fees apply

- How much the fees are

- How overdraft programs work

These disclosures usually appear:

- When you open the account

- In account agreements

- In periodic updates to account terms

However, disclosures do not require banks to warn you before each fee is charged.

Consumers can also review general fee explanations in the FDIC overdraft and account fees guide, which explains how banks structure common checking account charges.

Limits on “Double Fees” for the Same Transaction

Regulators have pressured banks to stop charging:

- NSF fees multiple times for the same returned payment

Many banks now limit or eliminate repeat NSF charges when the same payment is retried multiple times, but policies still vary. This is one reason it’s important to read your account’s fee schedule.

Oversight by Consumer Protection Agencies

Several federal agencies oversee overdraft practices, including:

- Consumer Financial Protection Bureau (CFPB)

- Federal Reserve

- Office of the Comptroller of the Currency (OCC)

- Federal Deposit Insurance Corporation (FDIC)

These agencies monitor:

They also investigate patterns of consumer complaints and unfair fee practices.

- Disclosure practices

- Fee structures

- Consumer complaints

While enforcement actions have pushed many banks to reduce or change fees, overdraft charges remain allowed under current law.

Recent Industry Changes (and Why Policies Still Differ)

In recent years, some banks have:

- Lowered overdraft fees

- Increased daily fee caps

- Added grace periods

- Eliminated overdraft fees on small negative balances

However:

- There is no single national standard

- Credit unions and community banks may have very different policies

- Older checking accounts may still carry higher fees

This is why reviewing your account terms regularly is important, even if you have banked there for many years.

This means two people at different banks can have completely different experiences, even with similar spending habits.

Bottom line:

Always rely on your own account’s fee schedule, not general assumptions about “what banks usually do.”

How Overdrafts Interact With Other Banking Issues

Overdrafts don’t happen in isolation. They can affect several parts of your financial life.

Account Closures

If an account remains negative too long, the bank may:

- Close the account

- Send the balance to collections

This can make it harder to:

- Open a new checking account elsewhere

- Avoid relying on check-cashing services or prepaid cards

Banks often report closures to specialty consumer reporting agencies used by other banks when screening new applicants.

Impact on Credit Reports

Overdraft fees themselves:

- Do not appear on credit reports

But if unpaid balances go to collections:

- Collection accounts can appear on your credit file

- This can affect loan approvals and interest rates

So while overdrafts start as a banking issue, unresolved ones can turn into a credit problem.

Interaction With Direct Deposits and Benefits

If your account is negative:

- This means you may not receive the full amount of your paycheck or benefit deposit.

- This can leave you short for upcoming expenses

For people receiving:

- Paychecks

- Social Security

- Disability benefits

This timing can create repeated overdraft cycles if expenses hit before deposits clear.

Common Beginner Mistakes That Lead to Overdraft Fees

Even careful people make these mistakes, especially when they’re new to managing checking accounts.

Relying on “Current Balance” Instead of “Available Balance”

Pending charges may not show in the current balance yet. Spending based on that number can lead to accidental overdrafts when pending charges settle.

Forgetting About Automatic Payments

Subscriptions and scheduled bills:

- Do not adjust themselves based on your balance

- Will still attempt to process even when funds are low

Assuming the Bank Will Decline First

Many people believe:

“If there’s no money, the bank won’t let it go through.”

For ACH payments and checks, that assumption is often wrong.

Waiting Too Long to Fix a Negative Balance

Delays can trigger:

- Additional overdrafts

- Extended overdraft fees

- Account closure risk

Fixing the balance quickly reduces total damage.

Overdraft Fees vs. Other Short-Term Cash Options (Simple Comparison)

When money runs short, overdraft fees are only one of several possible outcomes.

| Option | Typical Cost | Key Risk |

|---|---|---|

| Overdraft fee | High flat fee per transaction | Multiple fees quickly |

| Declined payment | No bank fee, but possible late fees | Service interruptions |

| Credit card | Interest if balance not paid | Adds to debt |

| Borrowing from savings | No fee, but reduces cushion | Less emergency protection |

This is not about choosing a “good” option — it’s about understanding trade-offs so you can avoid the most damaging outcomes when possible.

Real-Life Scenarios: How Overdraft Fees Actually Play Out

Seeing how overdraft fees happen in everyday situations makes the risks easier to recognize and avoid.

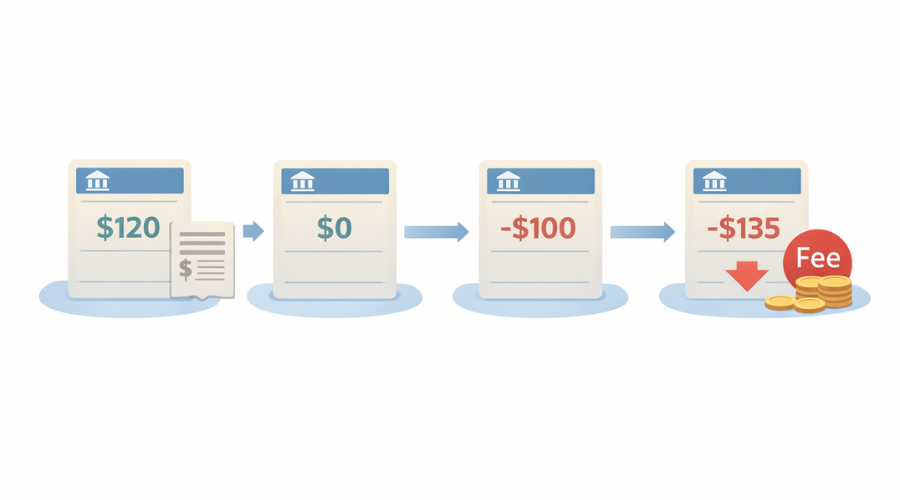

Scenario 1: Multiple Small Charges After One Large Bill

- Balance before bills: $120

- Electric bill posts: $140

- New balance: –$20 (overdraft fee added)

- Later that day:

- Coffee: $5

- Streaming service: $12

Each of those later transactions can trigger additional overdraft fees, even though the account was already negative.

What started as one mistake becomes several expensive charges. This is why daily fee caps matter, but they still do not prevent large total costs.

Scenario 2: Gas Station Holds and Delayed Posting

Some gas stations place:

- A temporary authorization hold higher than the final purchase amount

You may see:

- $150 pending charge

- Even if you only bought $40 of gas

If other transactions post while that hold is still pending, your available balance may drop much lower than expected, increasing overdraft risk.

Scenario 3: Paycheck Arrives the Same Day — But After Fees

- Rent auto-pay processes at 3:00 AM

- Paycheck posts at 9:00 AM

Even though both happen on the same day, the rent payment may still cause:

- Overdraft fee

- Negative balance until the deposit clears

Banks process transactions in batches, not based on when you “expect” money to arrive. This is why same-day deposits may not prevent early-morning overdrafts.

Scenario 4: Opted Out of Debit Overdrafts — Still Got a Fee

A person opts out and believes overdrafts are impossible.

But:

- Phone bill auto-pay posts

- Account balance is low

- Overdraft fee still applies

Opt-out does not cover ACH and bill payments.

Myths vs. Facts About Avoiding Overdraft Fees

Clearing up these common misunderstandings can help prevent repeated fees.

Myth: “Keeping track of my balance manually is enough.”

Fact:

Pending charges, holds, and posting delays make manual tracking unreliable when balances are tight. Alerts and buffers provide much stronger protection.

Myth: “Linking savings completely solves overdrafts.”

Fact:

It reduces fees, but repeated transfers can drain emergency funds and still leave you short later in the month.

Myth: “If my bank charges fees, switching banks is the only solution.”

Fact:

Changing banks may help, but many overdraft problems are caused by timing and habits that can still create negative balances anywhere.

Account management strategies matter regardless of bank.

How Overdraft Fees Can Affect Budgeting and Financial Stability

Overdraft fees often:

- Reduce the money available for necessities

- Push later bills in the month into risk

- Increase reliance on credit or borrowing

Because fees are unpredictable, they are:

- Hard to plan for

- Often excluded from budgets

- Emotionally frustrating

Preventing them is not just about saving fee money — it helps stabilize monthly cash flow and reduce stress around basic expenses.

Frequently Asked Questions About Overdraft Fees in the U.S.

-

Can a bank charge multiple overdraft fees in one day?

Yes. Many banks charge a fee for each transaction that overdraws your account, up to a daily maximum. That means several fees can occur in the same day if multiple payments post while your balance is too low.

-

Are overdraft fees legal in all states?

Yes. Overdraft fees are allowed nationwide under federal banking law. However, banks must follow federal disclosure and opt-in rules, and some states have additional consumer protection rules affecting certain practices.

-

Do credit unions charge overdraft fees too?

Many do, though fee amounts and policies often differ from large banks. Some credit unions offer lower fees or alternative programs, but overdraft charges are not limited to banks.

-

Can I be charged overdraft fees if my balance is only a few dollars negative?

Yes. Even being $1 or $2 overdrawn can trigger a full overdraft fee, depending on your bank’s policies. Some banks have small-dollar grace thresholds, but not all do.

-

Do overdraft fees affect my credit score?

The fees themselves do not appear on credit reports. However, if a negative balance goes unpaid and is sent to collections, that collection account can harm your credit.

-

Can banks change overdraft fee policies without my permission?

Banks can change account terms, but they must provide notice. You usually have the option to close the account if you disagree, though that may not be practical in the short term.

-

Should I always opt out of overdraft coverage?

Not necessarily. Opting out avoids fees on debit and ATM transactions, but it also means those transactions will be declined. Some people prefer approval in emergencies. The right choice depends on your cash flow stability and tolerance for declined payments.

-

Is overdraft protection the same as using credit?

When protection is linked to a credit line or credit card, it is a form of borrowing and may involve interest. When linked to savings, it is a transfer of your own money.

-

Why do some people get overdraft fees often while others never do?

The biggest factors are:

– Timing of income and bills

– Size of balance buffer

– Use of automatic payments

– Whether alerts and protections are set upIt is more about cash flow patterns than spending habits.

Final Thoughts on Overdraft Fees

Overdraft fees are not rare mistakes — they are a predictable result of tight cash flow and banking system timing. While banks control fee policies, consumers can reduce risk by understanding how transactions post, using alerts, and keeping small buffers when possible.

Avoiding overdraft fees is not about being perfect with money. It is about building systems that protect you when timing does not go as planned.

Disclaimer

This content is provided for educational and informational purposes only and does not constitute legal, tax, or financial advice. Banking rules, account terms, and personal financial situations vary. You should consult a qualified financial professional or your financial institution for guidance specific to your circumstances before making financial decisions.